データセンター改修市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Data Center Renovation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716494

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

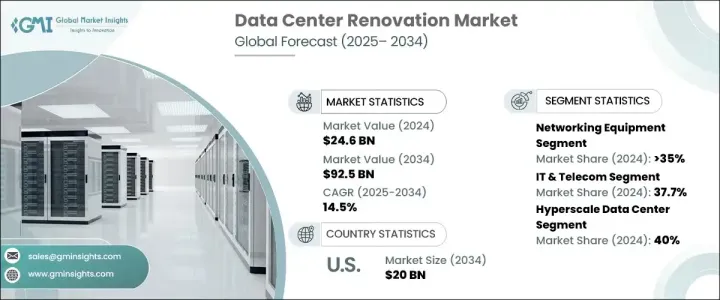

世界のデータセンター改修市場の2024年の市場規模は246億米ドルで、2025年から2034年にかけて14.5%のCAGRを記録すると予測されています。

クラウド・コンピューティング、ストリーミング・プラットフォーム、ソーシャルメディア、eコマースの急激な台頭により、世界のデータ・トラフィックが急増し、企業は増大する需要に対応するためデータセンターの近代化を迫られています。企業がリモートワーク、オンライン・コラボレーション、デジタル・トランザクションを採用し続ける中、高性能で低遅延のデータ処理が不可欠となっています。

人工知能(AI)、ビッグデータ分析、5G対応アプリケーションの導入が進む中、シームレスなデータフロー、セキュリティ強化、運用効率を確保するためのインフラ・アップグレードの必要性がさらに高まっています。データセンター事業者は、電力管理、冷却効率、ネットワーク性能を改善するための先進的なソリューションに投資しています。さらに、環境の持続可能性が重視されるようになったことで、再生可能エネルギー源、液体冷却システム、AIを活用したエネルギー管理ソリューションが採用され、運用コストの最小化とカーボンフットプリントの削減が推進されています。組織がハイパースケールデータセンターやエッジデータセンターの拡張に注力し、高速接続と低遅延通信をサポートするにつれて、アップグレードされたインフラに対する需要は急増し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 246億米ドル |

| 予測金額 | 925億米ドル |

| CAGR | 14.5% |

市場は製品別に、冷却、電源、ITラックとエンクロージャー、ネットワーク機器、LV/MV配電、データセンターインフラ管理(DCIM)に区分されます。ネットワーク機器は、高速接続とシームレスなデータフローの必要性により、2024年のデータセンター改修市場で35%のシェアを占めました。業界全体でデジタルトランスフォーメーションが加速するなか、データセンターはクラウドコンピューティング、AI、5G技術によるワークロードの増加をサポートするため、ルーター、スイッチ、光ファイバーインフラ、ロードバランサーのアップグレードを進めています。ソフトウェア定義ネットワーキング(SDN)とネットワーク機能仮想化(NFV)の採用により、運用の柔軟性が強化され、遅延が減少しており、市場の重要なセグメントとなっています。

最終用途別に見ると、市場はBFSI、ヘルスケア、IT・通信、政府、その他に分けられます。IT・通信分野は、クラウドサービス、AIアプリケーション、5Gネットワークの拡大に対応するため、高度なデジタルインフラへのニーズが高まっており、2024年のシェアは37.7%で市場をリードしました。データ量の急増に伴い、通信事業者やクラウドサービスプロバイダーは、データ処理の高速化、ネットワーク効率の向上、遅延の低減を確実にするため、ハイパースケールデータセンターやエッジデータセンターに投資しています。この動向は、データセンターの近代化と改修の需要を世界的に大きく押し上げる結果となっています。

北米のデータセンター改修市場は2024年に35%のシェアを占め、米国がこの地域を支配しています。クラウドコンピューティングの急成長、AIの採用拡大、規制要件の進化により、ハイパースケールデータセンターやエンタープライズデータセンターは近代化取り組みに多額の投資を行うようになりました。こうした投資は、冷却効率の向上、電力使用の最適化、サイバーセキュリティ・プロトコルの強化に重点が置かれています。持続可能性への取り組みは、こうした改修戦略の形成において重要な役割を担っており、各社は再生可能エネルギーソリューション、液体冷却技術、AIを活用したエネルギー管理システムを統合することで、効率の向上とカーボンフットプリントの削減に取り組んでいます。米国のデータセンター事業者が引き続き技術革新とコンプライアンスを優先していることから、市場は今後数年間にわたって持続的な成長を遂げる構えです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- メーカー

- システムインテグレーター

- 設置・保守プロバイダー

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース

- ケーススタディ

- 規制状況

- 影響要因

- 促進要因

- 世界中でオンラインサービスの利用が増加

- データセンターの近代化需要の高まり

- データセンターのエネルギー消費削減に対する政府の取り組み

- IT・通信セクターの拡大

- 業界の潜在的リスク&課題

- 施設の日常的な運営活動の中断

- 原材料と熟練労働者のコスト上昇

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 冷却

- 電源

- ITラック&エンクロージャー

- ネットワーク機器

- LV/MV配電

- DCIM

第6章 市場推計・予測:データセンター別、2021年~2034年

- 主要動向

- ハイパースケール

- コロケーション

- エンタープライズ

- エッジ

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- BFSI

- 政府機関

- ヘルスケア

- IT・通信

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- ABB

- Acer

- Ascenty

- Cisco

- Dell

- Equinix

- Fujitsu

- Gensler

- Hewlett Packard Enterprise(HPE)

- Hitachi

- HostDime

- Huawei

- IBM

- Inspur

- IPXON Networks

- KIO Networks

- Lenovo

- Oracle

- Schneider Electric

- Vertiv

目次

The Global Data Center Renovation Market was valued at USD 24.6 billion in 2024 and is projected to register a CAGR of 14.5% between 2025 and 2034. The exponential rise of cloud computing, streaming platforms, social media, and e-commerce has triggered a massive increase in global data traffic, prompting organizations to modernize their data centers to meet growing demands. As businesses continue to embrace remote work, online collaboration, and digital transactions, the need for high-performance, low-latency data processing has become essential.

The increasing adoption of artificial intelligence (AI), big data analytics, and 5G-enabled applications is further fueling the need for infrastructure upgrades to ensure seamless data flow, enhanced security, and operational efficiency. Data center operators are investing in advanced solutions to improve power management, cooling efficiency, and network performance. Additionally, the growing emphasis on environmental sustainability is driving the adoption of renewable energy sources, liquid cooling systems, and AI-powered energy management solutions to minimize operational costs and reduce carbon footprints. As organizations focus on scaling hyperscale and edge data centers to support high-speed connectivity and low-latency communication, the demand for upgraded infrastructure continues to surge.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.6 Billion |

| Forecast Value | $92.5 Billion |

| CAGR | 14.5% |

The market is segmented based on product into cooling, power, IT racks and enclosures, networking equipment, LV/MV distribution, and data center infrastructure management (DCIM). Networking equipment dominated the data center renovation market with a 35% share in 2024, driven by the need for high-speed connectivity and seamless data flow. As digital transformation accelerates across industries, data centers are upgrading their routers, switches, fiber-optic infrastructure, and load balancers to support increasing workloads from cloud computing, AI, and 5G technologies. The adoption of software-defined networking (SDN) and network function virtualization (NFV) is enhancing operational flexibility and reducing latency, making it a critical segment of the market.

On the basis of end use, the market is divided into BFSI, healthcare, IT and telecom, government, and others. The IT and telecom sector led the market with a 37.7% share in 2024 due to the growing need for advanced digital infrastructure to accommodate the expanding footprint of cloud services, AI applications, and 5G networks. As data volumes soar, telecom operators and cloud service providers are investing in hyperscale and edge data centers to ensure faster data processing, improved network efficiency, and reduced latency. This trend has resulted in a significant boost to the demand for data center modernization and renovation initiatives globally.

North America data center renovation market accounted for a 35% share in 2024, with the United States dominating the region. The rapid growth of cloud computing, increased adoption of AI, and evolving regulatory requirements have prompted hyperscale and enterprise data centers to invest heavily in modernization efforts. These investments are focused on enhancing cooling efficiency, optimizing power usage, and strengthening cybersecurity protocols. Sustainability initiatives play a critical role in shaping these renovation strategies, with companies integrating renewable energy solutions, liquid cooling technologies, and AI-driven energy management systems to improve efficiency and reduce their carbon footprints. As data center operators in the U.S. continue to prioritize innovation and compliance, the market is poised for sustained growth over the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Manufacturers

- 3.1.2 System integrators

- 3.1.3 Installation and maintenance providers

- 3.1.4 End Use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Case studies

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing use of online services across the globe

- 3.9.1.2 Growing demand for data center modernization

- 3.9.1.3 Government initiatives to reduce the energy consumption of data centers

- 3.9.1.4 Expansion of the IT & telecom sector

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Disruptions in the daily operational activities of facilities

- 3.9.2.2 Rising cost of raw materials and skilled labor

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Cooling

- 5.3 Power

- 5.4 IT Racks & enclosures

- 5.5 Networking equipment

- 5.6 LV/MV distribution

- 5.7 DCIM

Chapter 6 Market Estimates & Forecast, By Data Center, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Hyperscale

- 6.3 Colocation

- 6.4 Enterprise

- 6.5 Edge

Chapter 7 Market Estimates & Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Government

- 7.4 Healthcare

- 7.5 IT & telecom

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Acer

- 9.3 Ascenty

- 9.4 Cisco

- 9.5 Dell

- 9.6 Equinix

- 9.7 Fujitsu

- 9.8 Gensler

- 9.9 Hewlett Packard Enterprise (HPE)

- 9.10 Hitachi

- 9.11 HostDime

- 9.12 Huawei

- 9.13 IBM

- 9.14 Inspur

- 9.15 IPXON Networks

- 9.16 KIO Networks

- 9.17 Lenovo

- 9.18 Oracle

- 9.19 Schneider Electric

- 9.20 Vertiv

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日