|

市場調査レポート

商品コード

1716468

ポリマー電気ブッシング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Polymeric Electrical Bushing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ポリマー電気ブッシング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月12日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

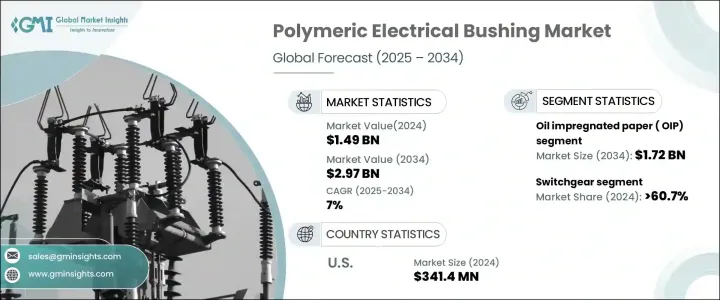

ポリマー電気ブッシングの世界市場は2024年に14億9,000万米ドルと評価され、2025年から2034年にかけてCAGR 7%で成長すると予測されています。

太陽光発電、風力発電、水力発電のような、よりクリーンで持続可能なエネルギー源へと世界の関心がシフトする中、高度な電気部品の必要性はこれまで以上に重要になっています。高分子電気ブッシングは、その優れた耐久性、高い機械的強度、過酷な気象条件への優れた耐性により、再生可能エネルギーシステムに不可欠な存在として、強い勢いを増しています。さらに、各国が老朽化した送電網の近代化を重視し、スマートグリッド技術を採用するにつれて、信頼性が高くメンテナンスフリーの電気部品への需要が高まっています。

送配電(T&D)ネットワークの複雑化に加え、エネルギー損失の削減と効率改善の必要性が高まっていることが、ポリマーブッシュの市場見通しを引き続き強めています。特に電力需要が急増している新興国では、送電線の拡張に向けた投資が進んでおり、業界参加者にとっては有利な機会となっています。さらに、電気インフラにおける環境に優しく高性能な材料の使用を促進する厳しい規制が、さまざまな用途でのポリメリックブッシングの採用をさらに加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億9,000万米ドル |

| 予測金額 | 29億7,000万米ドル |

| CAGR | 7% |

含油紙(OIP)分野は、急速な都市化、工業化の進展、エネルギー分野における継続的な技術進歩に牽引され、2034年までに17億2,000万米ドルを生み出すと予測されています。このセグメントの成長は、世界のT&Dセクターの継続的な拡大と密接に結びついており、電力需要の増加により、シームレスな運用を確保するための高度で効率的な部品が求められています。OIPブッシングは、その優れた絶縁耐力と優れた電気絶縁特性により、変圧器用途に選ばれる材料であり続けています。高電圧条件下で信頼性の高い性能を発揮するOIPブッシングは、産業、商業、住宅の各分野で増大する電力需要を支えるために不可欠です。

2024年に60.7%の市場シェアを占めたスイッチギアアプリケーション分野は、ポリメリックブッシングの需要増加の大部分を反映しています。多くの新興経済諸国が時代遅れの変圧器や配電システムのアップグレードに注力する中、ポリメリックブッシュは近代的なインフラに適したソリューションとして際立っています。その高度な絶縁性能と長寿命により、送電網の信頼性と効率を向上させることができます。

米国のポリマー電気ブッシング市場は2024年に3億4,140万米ドルに達し、スマートグリッド技術とインフラ近代化への投資が増加していることがその要因となっています。優れた性能、長寿命、厳しい環境ストレスに耐える能力を持つことから、全米の公益事業者は従来の磁器や石油ベースのブッシングからポリマー製の代替品への置き換えを積極的に進めています。これらの要因から、ポリマーブッシュは弾力性があり効率的な米国の送電網を構築する上で重要な部品となっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:ブッシングタイプ別、2021年~2034年

- 主要動向

- 含油紙(OIP)

- 鉱物ベース

- シリコンベース

- その他

- 樹脂含浸紙(RIP)

- その他

第6章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 中電圧

- 高電圧

- 超高電圧

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 変圧器

- 開閉装置

- その他

第8章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 産業

- ユーティリティ

- その他

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- ABB

- Barberi Rubinetterie Industriali

- CG Power and Industrial Solutions

- Eaton

- Elliot Industries

- General Electric

- Gipro

- Hitachi Energy

- Hubbell

- Jiangxi Johnson Electric

- Liyond

- Maschinenfabrik Reinhausen

- Meister International

- Nexans

- Pfisterer Holding

- Polycast

- Poinsa

- Siemens Energy

The Global Polymeric Electrical Bushing Market, valued at USD 1.49 billion in 2024, is projected to grow at a CAGR of 7% between 2025 and 2034, reflecting a robust demand trajectory driven by evolving power infrastructure needs worldwide. As the global focus shifts toward cleaner and more sustainable energy sources like solar, wind, and hydropower, the need for advanced electrical components has become more crucial than ever. Polymeric electrical bushings are gaining strong momentum due to their superior durability, high mechanical strength, and excellent resistance to harsh weather conditions, making them indispensable in renewable energy systems. Additionally, as countries emphasize the modernization of aging grids and adopt smart grid technologies, the demand for reliable and maintenance-free electrical components is on the rise.

The increasing complexity of power transmission and distribution (T&D) networks, coupled with a growing need to reduce energy losses and improve efficiency, continues to bolster the market outlook for polymeric bushings. The ongoing investments in expanding transmission lines, especially in emerging economies where electricity demand is surging, are also creating lucrative opportunities for industry participants. Moreover, stringent regulatory mandates promoting the use of eco-friendly and high-performance materials in electrical infrastructure are further accelerating the adoption of polymeric bushings across various applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.49 Billion |

| Forecast Value | $2.97 Billion |

| CAGR | 7% |

The oil-impregnated paper (OIP) segment is anticipated to generate USD 1.72 billion by 2034, driven by rapid urbanization, rising industrialization, and continuous technological advancements in the energy sector. The segment's growth is closely tied to the ongoing expansion of the global T&D sector, where the rising demand for electricity calls for advanced and efficient components to ensure seamless operations. OIP bushings continue to be the material of choice for transformer applications, owing to their superior dielectric strength and excellent electrical insulation properties. Their ability to offer reliable performance under high-voltage conditions makes them essential for supporting the increasing electricity demand across industrial, commercial, and residential sectors.

The switchgear application segment, which accounted for a 60.7% market share in 2024, reflects a significant portion of the growing polymeric bushing demand. As many developed economies focus on upgrading outdated transformer and distribution systems, polymeric bushings stand out as the preferred solution for modern infrastructure. Their advanced insulation capabilities and long service life help improve grid reliability and efficiency, which is critical as global electricity consumption continues to escalate.

The U.S. Polymeric Electrical Bushing Market reached USD 341.4 million in 2024, fueled by the nation's increasing investments in smart grid technologies and infrastructure modernization. Utility providers across the country are actively replacing traditional porcelain and oil-based bushings with polymeric alternatives, given their superior performance, longer lifespan, and ability to withstand severe environmental stresses. These factors make polymeric bushings a key component in building a resilient and efficient U.S. power grid.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Bushing Type, 2021 - 2034, ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Oil impregnated paper (OIP)

- 5.2.1 Mineral-based

- 5.2.2 Silicon-based

- 5.2.3 Others

- 5.3 Resin impregnated paper (RIP)

- 5.4 Others

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034, ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Medium voltage

- 6.3 High voltage

- 6.4 Extra high voltage

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034, ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 Transformer

- 7.3 Switchgear

- 7.4 Others

Chapter 8 Market Size and Forecast, By End Use, 2021 - 2034, ('000 Units & USD Million)

- 8.1 Key trends

- 8.2 Industries

- 8.3 Utility

- 8.4 Others

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034, (‘000 Units & USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 Russia

- 9.3.4 UK

- 9.3.5 Italy

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Barberi Rubinetterie Industriali

- 10.3 CG Power and Industrial Solutions

- 10.4 Eaton

- 10.5 Elliot Industries

- 10.6 General Electric

- 10.7 Gipro

- 10.8 Hitachi Energy

- 10.9 Hubbell

- 10.10 Jiangxi Johnson Electric

- 10.11 Liyond

- 10.12 Maschinenfabrik Reinhausen

- 10.13 Meister International

- 10.14 Nexans

- 10.15 Pfisterer Holding

- 10.16 Polycast

- 10.17 Poinsa

- 10.18 Siemens Energy