中電圧サージアレスタ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Medium Voltage Surge Arrester Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 127 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716450

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

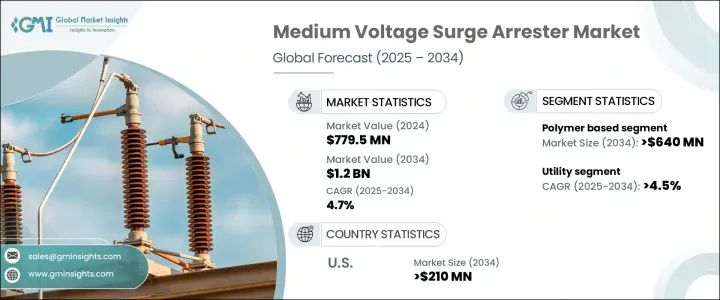

中電圧サージアレスタの世界市場は、2024年には7億7,950万米ドルとなり、2025年から2034年にかけてCAGR 4.7%で成長すると予測されています。

この成長は主に、急速な都市化と産業成長の加速に後押しされた、信頼性の高い送配電システムに対する需要の増加によってもたらされます。経済が拡大しインフラが近代化するにつれて、電気システムの安全性と信頼性を確保するための高度なサージ保護の必要性がさらに高まっています。サージアレスタは、機器の故障を防ぎ、ダウンタイムを最小限に抑える上で極めて重要な役割を果たすため、さまざまな産業で不可欠となっています。さらに、スマートグリッドと再生可能エネルギー源の採用が増加していることも、サージ保護ソリューションのニーズの増加に寄与しています。送電網が複雑化するにつれ、過酷な環境条件に耐え、送電網の安定性を確保できる高度な高圧避雷器の需要が大幅に増加すると予想されます。

市場は材料タイプ別にポリマーとポーセレンに区分されます。ここ数年、ポリマーベースの避雷器は、その優れた性能特性により大きな支持を得ています。これらのアレスタは、軽量で耐食性に優れ、過酷な環境条件下でも優れた耐久性を発揮するため、高く評価されています。電圧サージに対する堅牢な保護を必要とする産業では、重要なインフラを保護するためにポリマーベースのソリューションの採用が増加しています。2034年までに、ポリマーベース分野は6億4,000万米ドルを生み出すと予想されており、これは材料と生産技術の継続的な進歩が原動力となっています。一方、磁器ベースのサージアレスタは、特定の用途では依然として関連性が高いもの、ポリマーベースのものと比べて採用率は比較的緩やかです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億7,950万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 4.7% |

中電圧サージアレスタの用途は、公益事業、産業、住宅および商業地域など複数の分野にまたがっています。現在、公益事業分野が最大の市場シェアを占めており、2024年には48%を占める。この優位性は、電気サージからの保護強化を必要とする送電網の拡張と近代化構想への継続的な投資が後押ししています。製造施設、石油・ガス施設、データセンターなどの重要なインフラストラクチャは、運用の中断を防ぎ、機密機器を保護するために避雷器に大きく依存しています。再生可能エネルギー源の統合が進み、現代の送電網が複雑化するにつれ、公益事業部門におけるサージ保護ソリューションの需要は、今後10年間でさらに急増する見込みです。

米国の高圧サージアレスタ市場は、2024年に1億3,320万米ドルを生み出し、2034年には2億1,000万米ドルに達すると予測されています。この成長の要因には、老朽化したインフラの更新やスマートグリッドの継続的な拡大があり、高度なサージ保護ソリューションの採用が必要となっています。米国では引き続き送電網の近代化を優先し、先進技術を取り入れているため、送電網の安定性を確保し、運用上のリスクを最小限に抑えるサージアレスタの需要は堅調に伸びると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:材料別、2021年~2034年

- 主要動向

- ポリマー

- ポーセレン

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅・商業用

- 工業用

- ユーティリティ

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- CG Power &Industrial Solutions

- CHINT Group

- DEHN SE

- Eaton

- Ensto Elpro

- General Electric

- Hitachi Energy

- Hubbell

- Izoelektro

- Schneider Electric

- Siemens Energy

- Surgetek

- TDK Electronics

目次

The Global Medium Voltage Surge Arrester Market was valued at USD 779.5 million in 2024 and is projected to grow at a CAGR of 4.7% between 2025 and 2034. This growth is primarily driven by the increasing demand for reliable power transmission and distribution systems, fueled by rapid urbanization and accelerating industrial growth. As economies expand and infrastructure modernizes, the need for advanced surge protection becomes even more critical to ensure the safety and reliability of electrical systems. Surge arresters play a pivotal role in preventing equipment failure and minimizing downtime, making them indispensable in various industries. Additionally, the rising adoption of smart grids and renewable energy sources is contributing to the increased need for surge protection solutions. As power grids become more complex, the demand for advanced medium voltage surge arresters capable of withstanding harsh environmental conditions and ensuring grid stability is expected to rise significantly.

The market is segmented by material type into polymer and porcelain. Over the past few years, polymer-based surge arresters have gained significant traction due to their superior performance characteristics. These arresters are highly valued for their lightweight, corrosion-resistant properties, and exceptional durability in extreme environmental conditions. Industries that require robust protection against voltage surges are increasingly adopting polymer-based solutions to safeguard critical infrastructure. By 2034, the polymer-based segment is expected to generate USD 640 million, driven by continuous advancements in materials and production technologies. On the other hand, while porcelain-based surge arresters remain relevant in specific applications, their adoption rate has been relatively slower compared to their polymer counterparts.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $779.5 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 4.7% |

The application of medium voltage surge arresters spans multiple sectors, including utilities, industries, and residential and commercial areas. The utility sector currently holds the largest market share, accounting for 48% in 2024. This dominance is fueled by ongoing investments in power grid expansion and modernization initiatives that require enhanced protection from electrical surges. Critical infrastructure, such as manufacturing facilities, oil and gas installations, and data centers, heavily depends on surge arresters to prevent operational disruptions and safeguard sensitive equipment. With the increasing integration of renewable energy sources and the growing complexity of modern power grids, the demand for surge protection solutions within the utility sector is poised to surge further over the next decade.

The United States medium voltage surge arrester market generated USD 133.2 million in 2024 and is projected to reach USD 210 million by 2034. Factors contributing to this growth include the replacement of aging infrastructure and the ongoing expansion of smart grids, which necessitate the adoption of advanced surge protection solutions. As the U.S. continues to prioritize grid modernization and incorporate advanced technologies, the demand for surge arresters that ensure grid stability and minimize operational risks is expected to grow steadily.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Material, 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Polymer

- 5.3 Porcelain

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Residential & commercial

- 6.3 Industrial

- 6.4 Utility

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 CG Power & Industrial Solutions

- 8.3 CHINT Group

- 8.4 DEHN SE

- 8.5 Eaton

- 8.6 Ensto Elpro

- 8.7 General Electric

- 8.8 Hitachi Energy

- 8.9 Hubbell

- 8.10 Izoelektro

- 8.11 Schneider Electric

- 8.12 Siemens Energy

- 8.13 Surgetek

- 8.14 TDK Electronics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 127 Pages

- 納期

- 2~3営業日