産業用油絶縁開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Industrial Oil Insulated Switchgear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716448

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

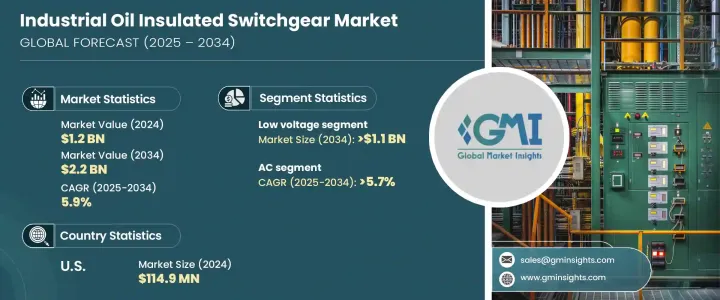

産業用油絶縁開閉装置の世界市場は、2024年に12億米ドルを生み出し、2025年から2034年にかけてCAGR 5.9%で成長すると予測されています。

この成長は、世界の急速な工業化、製造施設の拡大、継続的なインフラ開発により、信頼性の高い配電ソリューションに対する需要が高まっていることを反映しています。シームレスなワークフローを維持し、コストのかかるダウンタイムを回避するために、産業オペレーションはますます中断のない安定した電力に依存しています。停電やシステム障害は、操業の大幅な中断、機器の損傷、収益の損失につながります。石油化学、鉱業、自動車、製造業などの業界が事業を拡大するにつれて、高度で信頼性の高い開閉装置システムの必要性はますます高まっています。

油絶縁開閉装置は、産業用電気ネットワークの安定性と安全性を確保する耐障害性の強化、堅牢な絶縁、優れた冷却機能を提供することで、こうした需要に対応する上で重要な役割を果たしています。エネルギー効率を高め、老朽化した電気インフラを改善することへの関心が高まるにつれ、さまざまな産業で油絶縁開閉装置が採用されるようになっています。さらに、再生可能エネルギーとスマートグリッドシステムの統合が進む中、産業界は変動する電力負荷に対応し、さまざまな条件下で安定した性能を確保できる開閉装置ソリューションを求めています。油絶縁開閉装置は、他の選択肢では長期的な信頼性が得られないような過酷で厳しい環境でも、システムの完全性を維持する能力が認められているため、この動向は市場の成長を大きく後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 12億米ドル |

| 予測金額 | 22億米ドル |

| CAGR | 5.9% |

電圧別では、低電圧分野が顕著な成長を遂げ、2034年までに約11億米ドルの売上が見込まれています。安定した効率的な配電システムに対する需要の高まりとともに、産業オートメーションの急増がこの拡大の主な原動力となっています。特に新興国の中小企業は、最新の生産プロセスと自動化システムをサポートするため、低電圧油絶縁開閉装置を急速に採用しています。これらのスイッチギア・ソリューションは、世界中の産業が持続可能な発電方式に移行し続ける中、既存の送電網へのクリーンエネルギーや再生可能エネルギーの統合をサポートするために不可欠です。分散型エネルギーネットワーク内で効率的に動作し、複雑な負荷を処理できることから、最新の産業インフラにとってますます不可欠なものとなっています。

電流に関しては、送電と配電の主な方法として交流への依存が続いていることが主な要因となって、交流セグメントは2034年までに5.7%の成長を遂げると予測されています。交流は、長距離送電の効率性と大規模送電網システムとの互換性から、産業用アプリケーションに好まれる電流タイプです。石油化学、鉱業、製造業、重工業などの業界では、中電圧から高電圧の電力を管理し、業務の継続性と安全性を確保するために、常に交流油絶縁開閉装置に依存しています。

米国の産業用油絶縁開閉装置市場は、産業用電気インフラの近代化が進んでいることから、2024年には1億1,490万米ドルを占める。産業界が操業リスクの最小化と稼働時間の最大化に注力する中、油絶縁開閉装置はその優れた耐久性、耐障害性、高度な絶縁機能により、信頼されるソリューションとなっています。鉄鋼、自動車、航空宇宙、製薬などの分野では、無停電電源の確保、メンテナンスの必要性の低減、生産効率の最適化を目的として、この技術の採用が進んでいます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 低電圧

- 中電圧

- 高電圧

第6章 市場規模・予測:電流別、2021年~2034年

- 主要動向

- 交流

- 直流

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- オマーン

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- ペルー

- アルゼンチン

第8章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- CHINT Group

- Eaton

- Fuji Electric

- General Electric

- HD Hyundai Electric

- Hitachi

- Hyosung Heavy Industries

- Lucy Group

- Mitsubishi Electric

- Ormazabal

- Schneider Electric

- Siemens

- Skema

- Toshiba

目次

The Global Industrial Oil Insulated Switchgear Market generated USD 1.2 billion in 2024 and is projected to grow at a CAGR of 5.9% between 2025 and 2034. This growth reflects the rising demand for reliable power distribution solutions fueled by rapid industrialization, expansion of manufacturing facilities, and ongoing infrastructure development worldwide. Industrial operations are increasingly dependent on uninterrupted and stable electricity to maintain seamless workflows and avoid costly downtimes. Power outages or system failures can lead to significant operational disruptions, equipment damage, and revenue losses. As industries like petrochemicals, mining, automotive, and manufacturing scale up their operations, the need for advanced and reliable switchgear systems continues to intensify.

Oil-insulated switchgear plays a critical role in addressing these demands by offering enhanced fault tolerance, robust insulation, and superior cooling capabilities that ensure the stability and security of industrial electrical networks. The growing focus on enhancing energy efficiency and upgrading aging electrical infrastructure further propels the adoption of oil-insulated switchgear across diverse industries. Moreover, with the increasing integration of renewable energy and smart grid systems, industries seek switchgear solutions that can handle fluctuating power loads and ensure consistent performance under varying conditions. This trend significantly drives market growth as oil-insulated switchgear is recognized for its ability to maintain system integrity in harsh and demanding environments, where other alternatives might fail to deliver long-term reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.9% |

In terms of voltage, the low voltage segment is poised for notable growth and is expected to generate around USD 1.1 billion by 2034. The surge in industrial automation, alongside rising demand for stable and efficient power distribution systems, is a key driver behind this expansion. Small- and medium-sized enterprises, particularly in emerging economies, are rapidly adopting low voltage oil-insulated switchgear to support modern production processes and automation systems. These switchgear solutions are essential for supporting clean and renewable energy integration into existing grids as industries worldwide continue to shift towards sustainable power generation practices. Their ability to operate efficiently within decentralized energy networks and handle complex loads makes them increasingly indispensable for modern industrial infrastructure.

Regarding current, the AC segment is projected to witness growth of 5.7% by 2034, largely driven by the ongoing reliance on alternating current as the primary method for electricity transmission and distribution. AC is the preferred current type for industrial applications due to its efficiency in transporting power over long distances and its compatibility with large-scale grid systems. Industries such as petrochemicals, mining, manufacturing, and heavy engineering consistently depend on AC oil-insulated switchgear to manage medium to high-voltage electricity, ensuring operational continuity and safety.

The U.S. Industrial Oil Insulated Switchgear Market accounted for USD 114.9 million in 2024, propelled by the ongoing modernization of industrial electrical infrastructure. With industries focusing on minimizing operational risks and maximizing uptime, oil-insulated switchgear has become a trusted solution due to its superior durability, fault resistance, and advanced insulation features. Sectors including steel, automotive, aerospace, and pharmaceuticals are increasingly adopting this technology to secure uninterrupted power supply, reduce maintenance needs, and optimize production efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Current 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 AC

- 6.3 DC

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Oman

- 7.5.5 South Africa

- 7.5.6 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Bharat Heavy Electricals

- 8.3 CG Power and Industrial Solutions

- 8.4 CHINT Group

- 8.5 Eaton

- 8.6 Fuji Electric

- 8.7 General Electric

- 8.8 HD Hyundai Electric

- 8.9 Hitachi

- 8.10 Hyosung Heavy Industries

- 8.11 Lucy Group

- 8.12 Mitsubishi Electric

- 8.13 Ormazabal

- 8.14 Schneider Electric

- 8.15 Siemens

- 8.16 Skema

- 8.17 Toshiba

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日