プラスチックパレットの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測

Plastic Pallets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708211

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

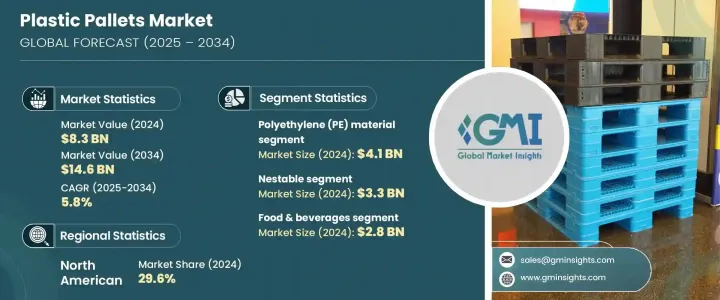

世界のプラスチックパレット市場は2024年に83億米ドルと評価され、2025年から2034年にかけてCAGR5.8%で成長すると予測されています。

効率的で持続可能、かつ耐久性のある包装ソリューションに対する需要の高まりが、特にeコマース、小売、医薬品、冷蔵倉庫などの分野でこの成長を後押ししています。プラスチックパレットは、従来の木製パレットよりも耐久性に優れ、汚染リスクの低減、衛生基準の遵守など、優れた利点を備えています。世界貿易が拡大し、サプライチェーンが複雑化するにつれ、物流効率を高め、コストを最小限に抑えるためにプラスチックパレットを選択する産業が増えています。カーボンフットプリントを削減し、輸送中の製品の安全性を確保することが重視されるようになり、さまざまな産業でプラスチックパレットの採用がさらに加速しています。

さらに、倉庫での自動化を促進する機能を含むプラスチックパレット設計の革新により、プラスチックパレットは現代のサプライチェーン管理に不可欠なものとなっています。プラスチックパレットに関連する長期的なコストメリットに関する意識の高まりは、害虫発生の懸念から木製パレットの使用を抑制することを目的とした政府の規制とともに、市場の成長をさらに後押ししています。循環型経済の実践と持続可能なサプライチェーンソリューションに向けた世界の後押しが、企業に再利用可能でリサイクル可能なプラスチックパレットへの投資を促し、多様な産業でその魅力を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 83億米ドル |

| 予測金額 | 146億米ドル |

| CAGR | 5.8% |

プラスチックパレット市場は材料別に区分され、ポリエチレン(PE)、ポリプロピレン(PP)、その他の材料が主要カテゴリーを形成しています。PEセグメントは2024年に41億米ドルと評価されました。この材料は、手頃な価格、軽量特性、顕著な柔軟性により、依然として製造業者の間で好まれています。ポリエチレンパレットは、構造的な完全性を維持しながら厳しい取り扱いに耐えることができるため、小売やeコマースの分野で特に人気があります。また、衝撃吸収性と耐衝撃性が製品の安全性にとって重要な要素である、飲料や動きの速い消費財(FMCG)の輸送にも広く使用されています。

プラスチックパレットはタイプ別にも分類され、市場は入れ子式、積み重ね式、ラック式、その他のタイプに分けられます。入れ子式プラスチックパレット分野は、省スペースで費用対効果の高い物流ソリューションに対する需要の高まりにより、2024年に33億米ドルを創出しました。入れ子式パレットは、倉庫スペースの削減と返送コストの最小化を実現する実用的なソリューションであり、大量出荷を必要とする業界に最適です。運用効率と二酸化炭素排出量の削減を優先する企業は、保管スペースを最適化し、全体的な輸送コストを削減できる入れ子式パレットにますます注目しています。

北米は2024年にプラスチックパレット市場で29.6%のシェアを占めましたが、これはサプライチェーンの合理化、倉庫の自動化、持続可能な代替包装への関心の高まりを反映しています。害虫駆除や衛生上の懸念から、木製パレットの使用に関する政府の規制が厳しくなっており、この地域ではプラスチックパレットへの移行がさらに加速しています。これらのパレットは、業界の要件と規制基準の両方を満たす、より耐久性があり、長持ちし、費用対効果の高いソリューションを提供します。産業界が自動化を採用し、サプライチェーンの最適化に投資し続ける中、プラスチックパレットは、様々なセクターで効率性と持続可能性の強化に極めて重要な役割を果たす態勢を整えています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 産業エコシステム分析

- 業界への影響要因

- 成長促進要因

- eコマースと小売業界の成長

- 食品・飲料業界における導入の増加

- 世界貿易とサプライチェーンの最適化の増加

- プラスチックリサイクル技術の進歩

- 冷蔵・化学産業の拡大

- 業界の潜在的リスク・課題

- 限られた修理可能性

- プラスチック廃棄物に対する環境問題

- 成長促進要因

- 成長の可能性分析

- 規制状況

- 技術動向

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ポリエチレン(PE)

- 高密度ポリエチレン(HDPE)

- LDPE

- ポリプロピレン(PP)

- その他

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 入れ子式

- ラック式

- スタッカブル

- その他

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品・飲料

- 化学品

- 医薬品

- 自動車

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Bekuplast

- Benoplast

- Cabka

- CHEP

- Craemer

- Loscam International

- Millwood

- Monoflo International

- Naeco Packaging

- Nilkamal Material Handling

- ORBIS Corporation

- Polymer Solutions International

- Premier Handling Solutions

- Rehrig Pacific

- Schoeller Allibert

- Smart-Flow

- TMF Corporation

- Werit Kunststoffwerke

目次

The Global Plastic Pallets Market was valued at USD 8.3 billion in 2024 and is projected to grow at a CAGR of 5.8% between 2025 and 2034. The rising demand for efficient, sustainable, and durable packaging solutions is driving this growth, particularly in sectors such as e-commerce, retail, pharmaceuticals, and cold storage. Plastic pallets offer superior advantages over traditional wooden pallets, including better durability, reduced risk of contamination, and compliance with hygiene standards. As global trade continues to expand and supply chains become more complex, industries are increasingly opting for plastic pallets to enhance logistical efficiency and minimize costs. The growing emphasis on reducing carbon footprints and ensuring product safety during transit has further accelerated the adoption of plastic pallets in various industries.

Additionally, innovations in plastic pallet design, including features that facilitate automation in warehouses, are making these pallets an essential part of modern supply chain management. Rising awareness about the long-term cost benefits associated with plastic pallets, along with government regulations aimed at curbing the use of wooden pallets due to concerns about pest infestations, is further boosting market growth. The global push toward circular economy practices and sustainable supply chain solutions is encouraging companies to invest in reusable and recyclable plastic pallets, enhancing their appeal across diverse industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 5.8% |

The plastic pallets market is segmented based on material, with polyethylene (PE), polypropylene (PP), and other materials forming the key categories. The PE segment was valued at USD 4.1 billion in 2024. This material remains a preferred choice among manufacturers due to its affordability, lightweight properties, and remarkable flexibility. Polyethylene pallets are particularly popular in the retail and e-commerce sectors due to their ability to withstand rigorous handling while maintaining their structural integrity. They are also widely used in the transportation of beverages and fast-moving consumer goods (FMCG), where shock absorption and impact resistance are critical factors for product safety.

Plastic pallets are also categorized by type, with the market divided into nestable, stackable, rackable, and other types. The nestable plastic pallet segment generated USD 3.3 billion in 2024, driven by the increasing demand for space-saving and cost-effective logistics solutions. Nestable pallets offer a practical solution for reducing warehouse space requirements and minimizing return shipping costs, making them ideal for industries with high-volume shipping needs. Businesses that prioritize operational efficiency and lower carbon emissions are increasingly turning to nestable pallets for their ability to optimize storage space and reduce overall transportation costs.

North America held a 29.6% share of the plastic pallets market in 2024, reflecting a growing preference for streamlined supply chains, automation in warehouses, and a focus on sustainable packaging alternatives. Stricter government regulations concerning the use of wooden pallets, driven by pest control and hygiene concerns, have further accelerated the shift towards plastic pallets in this region. These pallets offer a more durable, long-lasting, and cost-effective solution that meets both industry requirements and regulatory standards. As industries continue to adopt automation and invest in supply chain optimization, plastic pallets are poised to play a pivotal role in enhancing efficiency and sustainability across various sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce & retail industry

- 3.2.1.2 Rising adoption in the food & beverage industry

- 3.2.1.3 Rise in global trade & supply chain optimization

- 3.2.1.4 Advancements in plastic recycling technology

- 3.2.1.5 Expansion of cold storage & chemical industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited repairability

- 3.2.2.2 Environmental concerns over plastic waste

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.2.1 HDPE

- 5.2.2 LDPE

- 5.3 Polypropylene (PP)

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Nestable

- 6.3 Rackable

- 6.4 Stackable

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Chemicals

- 7.4 Pharmaceuticals

- 7.5 Automotive

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bekuplast

- 9.2 Benoplast

- 9.3 Cabka

- 9.4 CHEP

- 9.5 Craemer

- 9.6 Loscam International

- 9.7 Millwood

- 9.8 Monoflo International

- 9.9 Naeco Packaging

- 9.10 Nilkamal Material Handling

- 9.11 ORBIS Corporation

- 9.12 Polymer Solutions International

- 9.13 Premier Handling Solutions

- 9.14 Rehrig Pacific

- 9.15 Schoeller Allibert

- 9.16 Smart-Flow

- 9.17 TMF Corporation

- 9.18 Werit Kunststoffwerke

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日