|

市場調査レポート

商品コード

1708177

板紙包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Boxboard Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 板紙包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月12日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

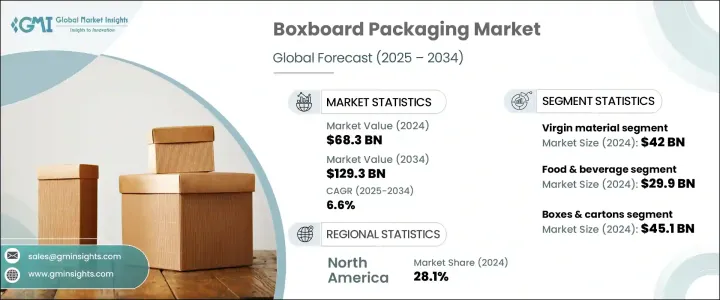

板紙包装の世界市場は2024年に683億米ドルを生み出し、2025年から2034年にかけてCAGR 6.6%で成長すると予測されています。

同市場は、持続可能で耐久性に優れ、多用途なパッケージング・ソリューションに対する需要の高まりに後押しされ、多業種にわたって着実な成長を続けています。消費者の嗜好が環境に優しく軽量なパッケージングにシフトする中、適応性とリサイクル性の高さから板紙包装が脚光を浴びています。都市化の進展とライフスタイルの変化によって、特に飲食品分野ではコンパクトで便利な、すぐに使えるパッケージへのニーズがさらに高まっています。

さらに、eコマースのブームと、魅力的で保護性の高いパッケージに対する需要の高まりが相まって、板紙包装メーカーに新たなビジネスチャンスをもたらしています。企業は現在、環境規制と消費者の期待の両方に沿った革新的なデザインと素材に多額の投資を行っています。世界各国の政府が使い捨てプラスチックに関する規制を強化し、循環型経済の重要性を強調する中、板紙包装市場は今後も世界の包装事情において重要な位置を占めると予想されます。高級化粧品から医薬品、動きの速い消費財に至るまで、ボックスボードパッケージングは、形状、機能、持続可能性を組み合わせる能力で際立っています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 683億米ドル |

| 予測金額 | 1,293億米ドル |

| CAGR | 6.6% |

市場は主に材料別にバージン材とリサイクル材に区分され、バージン材セグメントは2024年に420億米ドルを生み出します。バージン板紙は、優れた強度、滑らかな表面、卓越した印刷品質で高く評価されており、高級感のあるプレゼンテーションと堅牢な保護が重要な産業にとって理想的な選択肢となっています。高級仕上げと詳細なグラフィックをサポートする能力により、高級品、化粧品、医薬品パッケージングに好ましい選択肢となっています。製品を保護するだけでなく、店頭でのビジュアルアピールを高めるパッケージングを求めるブランドが増えているため、バージン素材の需要は堅調に推移すると予想されます。

最終用途産業別に分類すると、2024年には飲食品セクターが299億米ドルを占め、板紙包装市場で最大のシェアを占めています。調理済み食品、テイクアウト食品、コンビニエンス食品の消費の増加は、軽量で耐久性のある包装ソリューションの需要に直接影響を与えています。消費者が製品の品質を落とすことなく利便性を優先し続ける中、保護と保存期間延長の両方を提供する包装が不可欠になっています。さらに、オンライン食料品配達やeコマース・プラットフォームの急速な拡大により、製品の安全な輸送と保管を確保するための頑丈でカスタマイズ可能な包装の必要性が高まっています。

地域別では、北米が2024年の世界板紙包装市場で28.1%のシェアを占めています。この優位性は、高品質で持続可能な包装オプションを必要とする飲食品、医薬品、消費財などの業界からの旺盛な需要によるところが大きいです。環境に優しい包装を奨励し、使い捨てプラスチックを段階的に廃止する厳しい政府規制が、コーティングされた再生板や固形晒硫酸塩のようなリサイクル可能な材料の採用を促進しています。北米全域の企業は、進化する消費者の要求と規制基準に対応するため、パッケージング・ポートフォリオの強化に注力しており、この地域の市場成長をさらに後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 飲食品産業の成長

- 持続可能で環境に優しい包装に対する需要の高まり

- 印刷技術の進歩

- eコマース産業の急拡大

- 消費財産業の成長

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 原材料価格の変動

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- バージン

- リサイクル

第6章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 箱・カートン

- インサート・仕切り

- トレー

- その他

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 医薬品

- 工業製品

- エレクトロニクス

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Cellmark

- CMPC Biopackaging

- Crusader Packaging

- Custom Boxes Zone

- DS Smith

- Folbb

- Graphic Packaging International

- Huhtamaki

- ITC

- James Cropper

- Metsa Group

- Mondi

- Netpak

- Nippon Paper Industries

- Sappi

- Smurfit Kappa

- Spento Papers

- Stora Enso

The Global Boxboard Packaging Market generated USD 68.3 billion in 2024 and is expected to grow at a CAGR of 6.6% from 2025 to 2034. The market continues to witness steady growth, fueled by the rising demand for sustainable, durable, and versatile packaging solutions across multiple industries. As consumer preferences shift toward eco-friendly and lightweight packaging, boxboard packaging is gaining prominence for its adaptability and recyclability. Increasing urbanization and changing lifestyles have further heightened the need for compact, convenient, and ready-to-use packaging, particularly within the food and beverage sector.

Additionally, the boom in e-commerce, coupled with the growing demand for attractive and protective packaging, is shaping new opportunities for boxboard packaging manufacturers. Companies are now investing heavily in innovative designs and materials that align with both environmental mandates and consumer expectations. With governments worldwide tightening regulations around single-use plastics and emphasizing the importance of circular economies, the boxboard packaging market is expected to remain a vital part of the global packaging landscape. From premium cosmetics to pharmaceutical products and fast-moving consumer goods, boxboard packaging stands out for its ability to combine form, function, and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $68.3 Billion |

| Forecast Value | $129.3 Billion |

| CAGR | 6.6% |

The market is primarily segmented by material into virgin and recycled categories, with the virgin material segment generating USD 42 billion in 2024. Virgin boxboard materials are highly valued for their superior strength, smooth surface, and exceptional print quality, making them an ideal choice for industries where high-end presentation and robust protection are crucial. Their ability to support premium finishes and detailed graphics makes them a preferred option for luxury goods, cosmetics, and pharmaceutical packaging. The demand for virgin materials is expected to hold strong as brands increasingly seek packaging that not only protects the product but also enhances its visual appeal on store shelves.

When segmented by end-use industries, the food and beverage sector accounted for USD 29.9 billion in 2024, representing one of the largest shares in the boxboard packaging market. The rising consumption of ready-to-eat meals, takeout, and convenience foods is directly impacting the demand for lightweight and durable packaging solutions. As consumers continue to prioritize convenience without compromising product quality, packaging that offers both protection and extended shelf life is becoming essential. Moreover, the rapid expansion of online grocery delivery and e-commerce platforms has intensified the need for sturdy and customizable packaging to ensure safe product transport and storage.

Regionally, North America held a 28.1% share of the global boxboard packaging market in 2024. This dominance is largely driven by robust demand from industries such as food and beverage, pharmaceuticals, and consumer goods, all of which require high-quality and sustainable packaging options. Stringent government regulations encouraging eco-friendly packaging and phasing out single-use plastics are driving the adoption of recyclable materials like coated recycled boards and solid bleached sulfate. Companies across North America are focusing on enhancing their packaging portfolios to meet evolving consumer demands and regulatory standards, further boosting the regional market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of food & beverage industry

- 3.2.1.2 Rise in demand for sustainable and Eco-friendly packaging

- 3.2.1.3 Advancement in printing technology

- 3.2.1.4 Rapid expansion of E-commerce industry

- 3.2.1.5 Rise in consumer goods industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruption

- 3.2.2.2 Fluctuation in raw materials price

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Virgin

- 5.3 Recycled

Chapter 6 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Boxes & cartons

- 6.3 Inserts & dividers

- 6.4 Trays

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Pharmaceuticals

- 7.4 Industrial goods

- 7.5 Electronics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cellmark

- 9.2 CMPC Biopackaging

- 9.3 Crusader Packaging

- 9.4 Custom Boxes Zone

- 9.5 DS Smith

- 9.6 Folbb

- 9.7 Graphic Packaging International

- 9.8 Huhtamaki

- 9.9 ITC

- 9.10 James Cropper

- 9.11 Metsa Group

- 9.12 Mondi

- 9.13 Netpak

- 9.14 Nippon Paper Industries

- 9.15 Sappi

- 9.16 Smurfit Kappa

- 9.17 Spento Papers

- 9.18 Stora Enso