農業機器ファイナンス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Agricultural Equipment Finance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708173

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

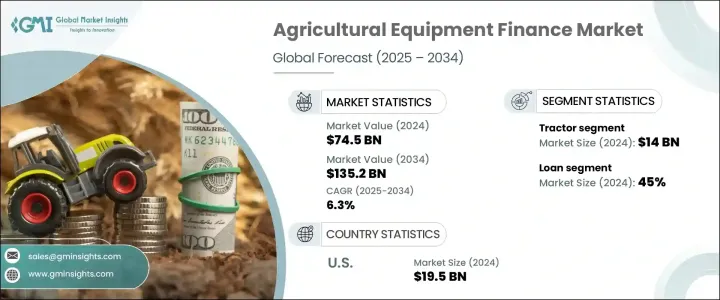

世界の農業機器ファイナンス市場は、2024年に745億米ドルを生み出し、2025年から2034年にかけてCAGR 6.3%で拡大すると予測されています。

この目覚ましい成長は、主に世界人口の継続的な増加が原動力となっており、これは食糧生産に対する需要の増大に直結しています。食糧需要が増大するにつれて、世界中の農家は農業生産高を増大させる必要に迫られ、トラクター、収穫機、灌漑システム、精密農業技術などの先進機械に大きく依存しています。しかし、最新の農業機械に関連する技術の進化やコストの上昇により、多くの農家はこれらの機械を購入することができないです。そこで、農家が初期費用を負担することなくハイテク機械を利用できるようにする融資ソリューションが重要になります。

農業機器ファイナンス市場は、農法の近代化を促進する上で極めて重要な役割を担っており、特に新興国の政府が食糧安全保障を確保するために機械化を奨励しています。加えて、収量を向上させ資源の浪費を最小限に抑えることを目的とした精密農業へのシフトが進行しているため、高度な農具とその調達に必要な金融支援に対する需要がさらに高まっています。機械化農業の利点に関する農家の意識の高まりは、農業機器に対する補助金や税制優遇措置といった政府の支援策と相まって、この市場の成長に大きな勢いを与えています。気候変動と労働力不足が世界的に農業セクターに影響を与え続ける中、柔軟な資金調達オプションに裏打ちされた効率的で高能力の機械の必要性は、これまで以上に重要になっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 745億米ドル |

| 予測金額 | 1,352億米ドル |

| CAGR | 6.3% |

農業機器市場は、トラクター、収穫機、灌漑システム、精密農業技術など、さまざまなカテゴリーに区分されます。なかでもトラクターは、2024年に140億米ドルを生み出す主要セグメントであり続けています。トラクターは、耕作、植え付け、収穫などの多様な農作業に不可欠であり、最も人気のある機械の1つとなっています。GPS対応システム、自律走行機能、燃費向上など、トラクター技術の絶え間ない進歩により、トラクターの価格は上昇し続けています。その結果、農家はこれらの必要不可欠な道具を購入するための資金調達オプションにますます依存するようになり、農業機器ファイナンス・ソリューションに対する安定した需要を牽引しています。

融資オプションに関して言えば、農業機器ファイナンス市場はローン、リース、レンタル購入、その他の選択肢に大別されます。このうち、ローン分野は2024年の市場シェアの45%を占めています。通常、商業銀行や農業専門の金融機関が提供する農業機械向けローンは、開発途上地域の農家に特に人気があります。これらのローンは柔軟な返済期間と長期所有のメリットを提供し、持続可能で効率的な経営を目指す農家にとって理想的な選択肢となっています。このようなオーダーメイドのローン商品を利用できるため、農家は生産性と収益性を高めるために最先端の機械に投資することができます。

地域別では、北米の農業機器ファイナンス市場が2024年の世界シェアの35%を占めています。堅調な農業部門を擁する米国は、世界最大の農産物生産・輸出国の一つとして際立っています。国内および国際的な食糧需要に対応するため、米国の農家は近代的で大容量の機器に大きく依存しており、これが資金調達ソリューションの必要性を大きく後押ししています。米国農業は世界市場で競争力を維持するため、技術的なアップグレードと生産効率の向上を優先しており、この需要はさらに拡大すると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 農業機械メーカー

- 金融機関および金融業者

- 販売業者および流通業者

- 最終用途

- 利益率分析

- 技術革新の状況

- 特許分析

- 使用事例

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 農業活動に対する政府の支援と補助金

- 人口増加による食糧需要の増大

- 大規模商業農業への移行

- 農機具の技術的進歩

- 業界の潜在的リスク&課題

- 不安定な農業市場

- 金融技術の導入の遅れ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:機器別、2021年~2034年

- 主要動向

- トラクター

- 収穫機

- 畜産機械

- 灌漑システム

- 定植・播種装置

- 施肥・散布装置

- 精密農業技術

- その他

第6章 市場推計・予測:資金調達別、2021年~2034年

- 主要動向

- ローン

- リース

- 分割払い購入

- その他

第7章 市場推計・予測:借り手別、2021年~2034年

- 主要動向

- 個人農家

- 大規模農業法人

- 協同組合・農業グループ

第8章 市場推計・予測:金融機関別、2021年~2034年

- 主要動向

- 商業銀行

- 政府系機関

- 設備メーカー

- 農業専門金融機関

- その他

第9章 市場推計・予測:融資期間別、2021年~2034年

- 主要動向

- 短期(3年まで)

- 中期(3~5年)

- 長期(5年以上)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- AGCO Finance

- Agricultural Bank of China

- American AgCredit

- Banco Santander

- Bayer

- BMO Harris Equipment Finance

- BNP Paribas Leasing Solutions

- CNH Industrial Capital

- CoBank

- DLL Group

- Farm Credit Canada

- FNB Agriculture

- John Deere Capital

- Kubota Credit

- Mahindra Finance

- Northland Capital Equipment Finance

- Rabo AgriFinance

- Regions Bank

- TD Equipment Finance

- Wells Fargo

目次

The Global Agricultural Equipment Finance Market generated USD 74.5 billion in 2024 and is projected to expand at a CAGR of 6.3% between 2025 and 2034. This remarkable growth is primarily driven by the continuously rising global population, which directly fuels an ever-growing demand for food production. As food demand escalates, farmers worldwide are compelled to boost their agricultural output, relying heavily on advanced machinery such as tractors, harvesters, irrigation systems, and precision farming technologies. However, with evolving technologies and higher costs associated with modern agricultural equipment, many farmers are unable to afford these machines outright. This is where financing solutions become critical, enabling farmers to access high-tech machinery without bearing the burden of full upfront costs.

The agricultural equipment finance market plays a crucial role in facilitating the modernization of farming practices, particularly as governments in emerging economies encourage mechanization to ensure food security. In addition, the ongoing shift toward precision agriculture, aimed at improving yields and minimizing resource wastage, further heightens the demand for sophisticated farming tools and the financial support necessary to procure them. Rising awareness among farmers regarding the benefits of mechanized farming, coupled with supportive government initiatives such as subsidies and tax benefits for agricultural equipment, adds significant momentum to the growth of this market. As climate change and labor shortages continue to impact the agriculture sector globally, the need for efficient, high-capacity machinery backed by flexible financing options becomes more critical than ever.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $74.5 Billion |

| Forecast Value | $135.2 Billion |

| CAGR | 6.3% |

The market for agricultural equipment is segmented into various categories, including tractors, harvesters, irrigation systems, and precision agriculture technologies. Among these, tractors remain a dominant segment, generating USD 14 billion in 2024. Tractors are indispensable for diverse farm operations like plowing, planting, and harvesting, making them one of the most sought-after machines. With constant advancements in tractor technology-such as GPS-enabled systems, autonomous functionality, and enhanced fuel efficiency-the price of tractors continues to rise. As a result, farmers increasingly depend on financing options to afford these essential tools, driving steady demand for agricultural equipment finance solutions.

When it comes to financing options, the agricultural equipment finance market is largely divided into loans, leasing, hire purchase, and other alternatives. Among these, the loan segment accounted for 45% of the market share in 2024. Loans for agricultural equipment, usually offered by commercial banks and specialized farm lenders, are especially popular among farmers in developing regions. These loans provide flexible repayment terms and the advantage of long-term ownership, making them an ideal choice for farmers aiming to build sustainable and efficient operations. The availability of such tailored loan products ensures that farmers can invest in cutting-edge machinery to boost productivity and profitability.

Regionally, North America Agricultural Equipment Finance Market held 35% of the global share in 2024. The United States, with its robust agricultural sector, stands out as one of the largest producers and exporters of agricultural goods worldwide. To keep pace with both domestic and international food demands, American farmers rely heavily on modern, high-capacity equipment, significantly driving the need for financing solutions. This demand is expected to grow further as U.S. agriculture continues to prioritize technological upgrades and enhanced production efficiency to remain competitive in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Agricultural equipment manufacturers

- 3.2.2 Financial institutions and lenders

- 3.2.3 Dealers and distributors

- 3.2.4 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Government support and subsidies for agricultural activities

- 3.9.1.2 Growing food demand due to rising population

- 3.9.1.3 Shift towards large-scale commercial farming

- 3.9.1.4 Technological advancements in farm equipment

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Volatile agricultural markets

- 3.9.2.2 Slow adoption of financial technology

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Equipment, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Tractor

- 5.3 Harvester

- 5.4 Livestock equipment

- 5.5 Irrigation systems

- 5.6 Planting and seeding equipment

- 5.7 Fertilizing and spraying equipment

- 5.8 Precision Agriculture Technology

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Financing, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Loan

- 6.3 Leasing

- 6.4 Hire purchase

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Borrower, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Individual farmers

- 7.3 Large agricultural corporations

- 7.4 Cooperatives and farming groups

Chapter 8 Market Estimates & Forecast, By Finance Provider, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Commercial banks

- 8.3 Government agencies

- 8.4 Equipment manufacturers

- 8.5 Specialized farm lenders

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Financing Term, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Short term (up to 3 years)

- 9.3 Medium term (3-5 years)

- 9.4 Long term (more than 5 years)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AGCO Finance

- 11.2 Agricultural Bank of China

- 11.3 American AgCredit

- 11.4 Banco Santander

- 11.5 Bayer

- 11.6 BMO Harris Equipment Finance

- 11.7 BNP Paribas Leasing Solutions

- 11.8 CNH Industrial Capital

- 11.9 CoBank

- 11.10 DLL Group

- 11.11 Farm Credit Canada

- 11.12 FNB Agriculture

- 11.13 John Deere Capital

- 11.14 Kubota Credit

- 11.15 Mahindra Finance

- 11.16 Northland Capital Equipment Finance

- 11.17 Rabo AgriFinance

- 11.18 Regions Bank

- 11.19 TD Equipment Finance

- 11.20 Wells Fargo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日