|

市場調査レポート

商品コード

1708170

紙製パレット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Paper Pallets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 紙製パレット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月11日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

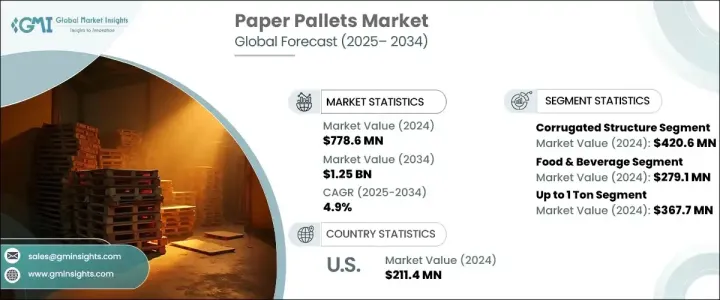

紙製パレットの世界市場は、2024年に7億7,860万米ドルと評価され、2025年から2034年にかけてCAGR 4.9%で成長すると予測されています。

この成長の主な要因は、eコマース分野の急拡大と、持続可能でコスト効率の高いソリューションによるサプライチェーンの合理化に注目が集まっていることです。世界の産業界が環境に配慮したビジネス慣行を取り入れる中、紙製パレットは従来の木製パレットやプラスチックパレットに代わる実用的で環境に優しい代替品として台頭してきました。これらのパレットは、その軽量構造、リサイクル性、コスト効率の高さにより、著しい支持を集めています。各業界の企業は、輸送コストの削減、厳しい環境規制への対応、持続可能な包装に対する消費者の需要の高まりに対応するため、紙製パレットを選択する傾向が強まっています。

さらに、ロジスティクスの最適化、カーボンフットプリントの最小化、プラスチック削減義務の遵守が重視されるようになり、世界中で紙製パレットの需要が高まっています。紙製パレットへのシフトは、倉庫効率の改善、運営経費の削減、環境に優しいパッケージング・ソリューションを支援する政府のイニシアティブに沿うという企業の戦略的努力によっても推進されています。国境を越えた貿易や世界の物流網の増加、衛生的で使い捨て可能な、輸出に準拠したパッケージングへのニーズの高まりも、紙製パレットの市場アピールの拡大に拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億7,860万米ドル |

| 予測金額 | 12億5,000万米ドル |

| CAGR | 4.9% |

コスト効率が高いだけでなく、環境基準や循環型経済目標に準拠したパッケージング・ソリューションを業界が求める中、紙製パレットの需要は急増を続けています。企業は環境への影響を最小限に抑えながら業務効率を向上させるために紙製パレットに注目しており、この動向はeコマース、飲食品、医薬品、消費財などの分野で急速に勢いを増しています。紙製パレットは、規制上の要求と、より環境に優しい製品や包装材を求める消費者の嗜好の両方の進化に応えようと努力する企業にとって、魅力的な選択肢です。世界サプライチェーンが複雑化するにつれ、汎用性が高く軽量でリサイクル可能なパレットソリューションへのニーズが、市場の堅調な見通しを後押ししています。

紙製パレット市場は、構造と最終用途産業によって区分できます。段ボール紙製パレットが市場をリードし、2024年には4億2,060万米ドルを生み出します。これらのパレットは軽量で耐久性があり、再生可能でリサイクル可能な材料から作られているため、持続可能な物流を重視する企業にとって理想的です。特に、効率的なラスト・マイル・デリバリーが重要な要件であるeコマースのような業界では、プラスチック廃棄物削減のための規制努力によって、その採用はさらに後押しされています。

用途別では、持続可能で衛生的なパッケージング・ソリューションに対する需要の高まりによって、飲食品セグメントが2024年に2億7,910万米ドルを占めました。包装食品の消費の増加とオンライン食品宅配サービスの増加がこの動向の主な要因です。紙製パレットは、安全で費用対効果が高く、環境に優しいパッケージングオプションを提供し、業界の持続可能性向上への後押しと一致します。

北米が世界的に優位を占め、2024年の紙製パレット市場で32.4%のシェアを獲得しました。同地域の成長の原動力は、リサイクル可能で軽量なロジスティクス・ソリューションに対する旺盛な需要に加え、環境に優しい素材の使用や使い捨てプラスチックの禁止を奨励する政府の政策です。これらの要因に加え、eコマースや食品宅配などの業界で持続可能な包装に対する消費者の嗜好が高まっていることが、北米全域で紙製パレットの採用を加速させています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- プラスチック使用に対する厳しい規制

- 軽量化とコスト効率

- サプライチェーン最適化への注目の高まり

- eコマース産業の急拡大

- 飲食品業界の成長

- 業界の潜在的リスク&課題

- 高い初期投資コスト

- 湿度感受性と耐久性の問題

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:構造別、2021年~2034年

- 主要動向

- 段ボールパレット

- ハニカムパレット

- ハイブリッド

第6章 市場推計・予測:耐荷重別、2021~2034年

- 主要動向

- 1トン未満

- 1~2トン

- 2トン以上

第7章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 2ウェイ

- 4ウェイ

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 医薬品

- 小売・eコマース

- 化学

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- DS Smith

- Elsons International

- EXA PACK

- FICUS PAX

- GL Packaging

- International Paper

- INTERPAK INDUSTRIES PTE LTD

- Karton Palet

- Kraftpal

- Litco International, Inc.

- Mondi

- Napco Nationa

- Pallite Group

- ProtoPack, LLC.

- Shenzhen Topwon Group Co.,Ltd

- Signode Industrial Group LLC

- Smurfit Kappa

- Tri-Wall

- WestRock Company

- Custom Packaging Products

The Global Paper Pallets Market was valued at USD 778.6 million in 2024 and is expected to grow at a CAGR of 4.9% between 2025 and 2034. This growth is primarily fueled by the rapid expansion of the e-commerce sector and the growing focus on streamlining supply chains with sustainable and cost-effective solutions. As global industries embrace environmentally responsible business practices, paper pallets have emerged as a practical and eco-friendly alternative to traditional wooden and plastic pallets. These pallets are gaining remarkable traction due to their lightweight structure, recyclability, and cost-efficiency. Companies across industries are increasingly opting for paper pallets to reduce shipping costs, comply with stringent environmental regulations, and meet growing consumer demand for sustainable packaging.

Furthermore, the rising emphasis on optimizing logistics, minimizing carbon footprints, and adhering to plastic reduction mandates is propelling the demand for paper pallets worldwide. The shift toward paper pallets is also driven by companies' strategic efforts to improve warehouse efficiency, cut operational expenses, and align with government initiatives that support eco-friendly packaging solutions. The rise of cross-border trade and global logistics networks, along with the increasing need for hygienic, disposable, and export-compliant packaging, adds to the growing market appeal of paper pallets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $778.6 Million |

| Forecast Value | $1.25 Billion |

| CAGR | 4.9% |

The demand for paper pallets continues to surge as industries seek packaging solutions that are not only cost-effective but also comply with environmental standards and circular economy goals. Businesses are turning to paper pallets to enhance operational efficiencies while minimizing their environmental impact, and this trend is rapidly gaining momentum across sectors like e-commerce, food and beverage, pharmaceuticals, and consumer goods. Paper pallets are an attractive choice for companies striving to meet both regulatory demands and evolving consumer preferences for greener products and packaging materials. As global supply chains become more complex, the need for versatile, lightweight, and recyclable pallet solutions is driving a robust market outlook.

The paper pallets market can be segmented by structure and end-use industries. Corrugated paper pallets led the market, generating USD 420.6 million in 2024. These pallets are lightweight, durable, and made from renewable and recyclable materials, making them an ideal fit for businesses focused on sustainable logistics. Their adoption is further boosted by regulatory efforts to reduce plastic waste, especially in industries like e-commerce, where efficient last-mile delivery is a critical requirement.

In terms of application, the food and beverage segment accounted for USD 279.1 million in 2024, driven by increasing demand for sustainable and hygienic packaging solutions. The growing consumption of packaged food and the rise in online food delivery services are key contributors to this trend. Paper pallets offer a safe, cost-effective, and eco-friendly packaging option that aligns with the industry's push toward greater sustainability.

North America dominated the global landscape, capturing a 32.4% share of the paper pallets market in 2024. The region's growth is powered by strong demand for recyclable and lightweight logistics solutions, coupled with government policies encouraging the use of eco-friendly materials and bans on single-use plastics. These factors, along with rising consumer preference for sustainable packaging in industries such as e-commerce and food delivery, are accelerating paper pallet adoption across North America.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent Regulations on Plastic Usage

- 3.2.1.2 Lightweight and Cost Efficiency

- 3.2.1.3 Increased Focus on Supply Chain Optimization

- 3.2.1.4 Rapid Expansion of the E-Commerce Industry

- 3.2.1.5 Growth in the Food & Beverage Industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment Cost

- 3.2.2.2 Moisture Sensitivity and Durability Issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Structure, 2021 – 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Corrugated pallets

- 5.3 Honeycomb pallets

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Load Capacity, 2021 – 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 1 Ton

- 6.3 1-2 Tons

- 6.4 Above 2 Tons

Chapter 7 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 2-way

- 7.3 4-way

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Pharmaceuticals

- 8.4 Retail & E-Commerce

- 8.5 Chemical

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 DS Smith

- 10.2 Elsons International

- 10.3 EXA PACK

- 10.4 FICUS PAX

- 10.5 GL Packaging

- 10.6 International Paper

- 10.7 INTERPAK INDUSTRIES PTE LTD

- 10.8 Karton Palet

- 10.9 Kraftpal

- 10.10 Litco International, Inc.

- 10.11 Mondi

- 10.12 Napco Nationa

- 10.13 Pallite Group

- 10.14 ProtoPack, LLC.

- 10.15 Shenzhen Topwon Group Co.,Ltd

- 10.16 Signode Industrial Group LLC

- 10.17 Smurfit Kappa

- 10.18 Tri-Wall

- 10.19 WestRock Company

- 10.20 Custom Packaging Products