|

市場調査レポート

商品コード

1708158

自動車用燃料供給ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Fuel Feed Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用燃料供給ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月07日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

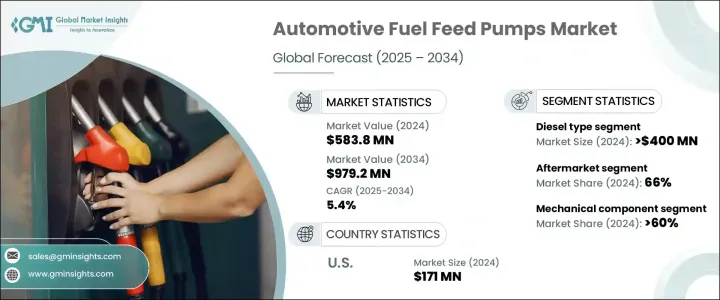

自動車用燃料供給ポンプの世界市場は、2024年には5億8,380万米ドルとなり、2025年から2034年にかけてCAGR 5.4%で成長すると予測されています。

この市場は、先進国と新興経済諸国における自動車生産と販売の急増に牽引され、着実に拡大しています。中国、インド、ブラジルなどの急成長市場で都市化が加速し、可処分所得が増加するにつれて、乗用車と商用車の需要も急上昇しています。より多くの車両が走行する中、効率的な燃料供給ポンプ・システムの必要性が高まっています。これらの部品は、シームレスな燃料供給とエンジン性能の維持に重要な役割を果たしているからです。

さらに、燃費の向上や排出ガス規制の強化など、自動車工学の技術的進歩も、高度な燃料供給ポンプの採用に拍車をかけています。また、自動車メーカーがエンジンの耐久性と燃料使用量の最適化を優先しているため、世界の自動車セクターがハイブリッドエンジンや高度な内燃機関にシフトしていることも、高性能燃料供給ポンプシステムの需要を刺激しています。さらに、自動車保有台数の老朽化による交換部品のニーズの高まりと、自動車の排出ガスと性能に関する政府規制の強化が、市場のダイナミクスに影響を与え、世界中のOEMおよびアフターマーケットサプライヤーの双方に一貫した成長機会を生み出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5億8,380万米ドル |

| 予測金額 | 9億7,920万米ドル |

| CAGR | 5.4% |

自動車用燃料供給ポンプ市場は、エンジンの種類によってガソリンとディーゼルに区分されます。このうち、ディーゼルエンジン用燃料供給ポンプの2024年の売上高は4億米ドルです。ディーゼルエンジンは、トラック、バス、建設機械などの商用車や産業車両に広く使用されており、いずれも高効率で耐久性の高い燃料供給システムを必要とします。ディーゼル燃料供給ポンプは、エンジン出力を最適化し、燃料効率を向上させ、エンジンの長期信頼性を確保する高圧燃料噴射システムのサポートに不可欠です。特に建設、ロジスティクス、公共輸送の各分野で大型車の世界の需要が高まるにつれて、堅牢なディーゼル燃料供給ポンプに対するニーズが高まっています。これらのポンプは、過酷な運転条件への対応能力で支持され、さまざまな業界の高性能車両に不可欠な部品となっています。

自動車用燃料供給ポンプの販売は、OEM(相手先ブランド製造)チャネルとアフターマーケットチャネルに分類されます。アフターマーケットセグメントは2024年に66%のシェアを占め、その主な理由は自動車の老朽化に伴いポンプの交換ニーズが高まっているためです。燃料供給ポンプは時間の経過とともに摩耗し、車両の性能と安全性を維持するために交換が必要になります。消費者も車両運行業者も同様に、すぐに入手でき、さまざまな車種に適合する、費用対効果が高く信頼性の高いアフターマーケット・ソリューションを求めています。アフターマーケットの幅広い製品の入手可能性と手頃な価格は、多様な顧客層を引き付け続けており、市場情勢の重要な部分を占めています。

米国の自動車用燃料供給ポンプ市場は、2024年に1億7,100万米ドルを生み出し、2025年から2034年にかけてCAGR 5.5%で成長する見込みです。この成長の主な原動力は、同国の自動車保有台数の多さと強力な自動車製造エコシステムです。米国では自動車の平均車齢が上昇しているため、アフターマーケットの燃料供給ポンプに対する需要が高まっています。米国の堅調な交換市場は、性能と寿命に対する消費者の期待に応える高品質で耐久性のある燃料供給ポンプの必要性を浮き彫りにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料メーカー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- コスト内訳分析

- 主要ニュース&イニシアティブ

- 影響要因

- 促進要因

- 自動車生産・販売の増加

- 厳しい排ガス規制

- 低燃費車への需要の高まり

- 自動車技術の進歩

- 業界の潜在的リスク&課題

- 技術革新のための高い研究開発費

- 自動車の安全・性能基準の厳格化

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:エンジン別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- メカニカル

- 電動

- ターボポンプ

第7章 市場推計・予測:自動車別、2021年~2034年

- 主要動向

- 乗用車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

- 二輪車

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 直接噴射システム

- マルチポイント噴射システム

- 燃料噴射システム

- キャブレターエンジン

- 高性能車

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aisin Seiki

- AST Otomotiv

- Carter Fuel

- Continental

- Daimler

- Delphi Automotive

- DENSO

- DEUTZ

- Devendra

- HELLA

- Hitachi Astemo

- Johnson Electric

- Perkins Engines

- Rheinmetall

- Robert Bosch

- Scania

- Schaeffler

- SHW

- Valeo

- ZF Friedrichshafen

The Global Automotive Fuel Feed Pumps Market was valued at USD 583.8 million in 2024 and is projected to grow at a CAGR of 5.4% between 2025 and 2034. The market is witnessing steady expansion driven by surging vehicle production and sales across both developed and emerging economies. As urbanization accelerates and disposable incomes rise in fast-growing markets like China, India, and Brazil, the demand for passenger and commercial vehicles is also rising sharply. With more vehicles on the road, the need for efficient fuel feed pump systems is growing, as these components play a crucial role in ensuring seamless fuel delivery and maintaining engine performance.

Additionally, technological advancements in automotive engineering, including the push toward better fuel efficiency and emission control, are fueling the adoption of advanced fuel feed pumps. The global automotive sector's shift toward hybrid and advanced internal combustion engines is also stimulating the demand for high-performance fuel feed pump systems as automakers prioritize engine durability and optimized fuel usage. Furthermore, the increasing need for replacement parts due to aging vehicle fleets, combined with stricter government regulations for vehicle emissions and performance, is influencing market dynamics and creating consistent growth opportunities for both OEM and aftermarket suppliers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $583.8 Million |

| Forecast Value | $979.2 Million |

| CAGR | 5.4% |

The automotive fuel feed pump market is segmented based on engine type into gasoline and diesel categories. Among these, diesel engine fuel feed pumps accounted for USD 400 million in revenue in 2024. Diesel-powered engines are widely used in commercial and industrial vehicles, including trucks, buses, and construction machinery, all of which require highly efficient and durable fuel delivery systems. Diesel fuel feed pumps are essential in supporting high-pressure fuel injection systems that optimize engine power, improve fuel efficiency, and ensure long-term engine reliability. As global demand for heavy-duty vehicles grows, particularly in the construction, logistics, and public transportation sectors, the need for robust diesel fuel feed pumps is rising. These pumps are favored for their ability to handle extreme operating conditions, making them indispensable components in high-performance vehicles across a range of industries.

Sales of automotive fuel feed pumps are classified into OEM (original equipment manufacturer) and aftermarket channels. The aftermarket segment dominated with a 66% share in 2024, largely due to the rising need for replacement pumps as vehicles age. Over time, fuel feed pumps experience wear and require replacement to maintain vehicle performance and safety. Consumers and fleet operators alike seek cost-effective and reliable aftermarket solutions that are readily available and compatible with a variety of vehicle models. The aftermarket's broad product availability and affordability continue to attract a diverse customer base, making it a critical part of the market landscape.

The U.S. automotive fuel feed pumps market generated USD 171 million in 2024, with expectations to grow at a CAGR of 5.5% from 2025 to 2034. This growth is primarily driven by the country's substantial vehicle fleet and a strong automotive manufacturing ecosystem. The rising average age of vehicles in the U.S. amplifies the demand for aftermarket fuel feed pumps as replacements become essential to keep vehicles operational and efficient. The robust replacement market in the U.S. highlights the need for high-quality, durable fuel feed pumps that align with consumer expectations for performance and longevity.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing vehicle production & sales

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing demand for fuel-efficient vehicles

- 3.7.1.4 Advancements in automotive technology

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High R&D costs for innovation

- 3.7.2.2 Stricter vehicle safety & performance standards

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Diesel

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Mechanical

- 6.3 Electric

- 6.4 Turbopump

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

- 7.4 Two wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Direct injection system

- 8.3 Multipoint injection system

- 8.4 Fuel injection system

- 8.5 Carbureted engines

- 8.6 High-performance vehicles

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 AST Otomotiv

- 11.3 Carter Fuel

- 11.4 Continental

- 11.5 Daimler

- 11.6 Delphi Automotive

- 11.7 DENSO

- 11.8 DEUTZ

- 11.9 Devendra

- 11.10 HELLA

- 11.11 Hitachi Astemo

- 11.12 Johnson Electric

- 11.13 Perkins Engines

- 11.14 Rheinmetall

- 11.15 Robert Bosch

- 11.16 Scania

- 11.17 Schaeffler

- 11.18 SHW

- 11.19 Valeo

- 11.20 ZF Friedrichshafen