|

市場調査レポート

商品コード

1708150

頭蓋インプラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cranial Implant Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 頭蓋インプラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月06日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

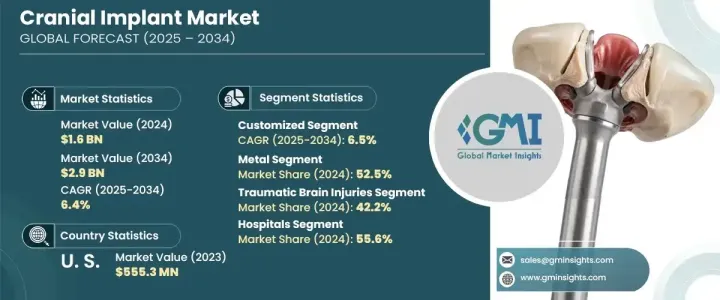

頭蓋インプラントの世界市場は、2024年に16億米ドルと評価され、2025年から2034年にかけてCAGR 6.4%で成長すると予測されています。

同市場は、神経疾患や外傷性脳損傷の有病率の上昇、高度な手術技術の採用増加などを背景に、着実な成長を遂げています。脳卒中、てんかん、アルツハイマー病、先天性頭蓋骨奇形などの疾患により、頭蓋再建を必要とする患者が世界中で増加しています。世界人口の高齢化と事故による頭部外傷の増加により、高品質の頭蓋インプラントに対する需要は急増すると予想されます。3Dプリンティングと生体材料の絶え間ない進歩が業界に革命をもたらし、インプラントの精密性、耐久性、生体適合性を高めています。さらに、新興国市場の有利な規制政策により製品承認が加速しており、企業は革新的なソリューションをより効率的に導入できるようになっています。新興国におけるヘルスケア投資の増加や、神経・外傷治療へのアクセスの改善も、市場拡大に寄与しています。

市場はカスタマイズ製品と非カスタマイズ製品に分けられます。2024年には、カスタマイズされた頭蓋インプラントは10億米ドルを生み出し、今後10年間のCAGRは6.5%と予測され、顕著な成長が見込まれています。これらのインプラントは、正確な適合を提供する能力によって人気を集めており、再建の結果と機能的性能の両方を高めています。CTスキャンやMRIのような高度な画像診断技術を使用することで、医療専門家は個人の頭蓋骨構造にシームレスに適合する患者専用のインプラントを作成することができます。この個別化されたアプローチは、術後の回復と審美的な結果を大幅に改善し、ヘルスケア部門全体でカスタマイズされたソリューションの需要に拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 29億米ドル |

| CAGR | 6.4% |

頭蓋インプラントは、主に金属、ポリマー、セラミック材料で作られています。2024年の市場規模は金属製が52.5%を占め、8億3,090万米ドルの売上を計上しました。チタンとその合金は、その卓越した強度、生体適合性、長期耐久性により、依然として好ましい選択です。金属製インプラントは脳への保護に優れているため、外傷や複雑な頭蓋骨手術から回復した患者に理想的です。ポリマーベースのインプラントと比較して、金属製インプラントは寿命が長く、故障率が低いため、医療処置に広く採用されています。

北米の頭蓋インプラント市場は、2024年に6億4,060万米ドルを生み出し、2034年には12億米ドルに達すると予測されています。この成長の主な要因は、外傷性脳損傷(TBI)の発生率の増加と、この地域の先進ヘルスケアインフラです。特に米国は、最先端の医療技術の開発と商業化を奨励する支援的な規制環境の恩恵を受けています。AI支援イメージング、3Dプリンティング、生体工学的材料の採用は、頭蓋インプラントの情勢を再構築し、より効率的でカスタマイズされた治療オプションを可能にしています。こうした技術的進歩は、旺盛なヘルスケア支出や神経外科ソリューションに対する高い認識と相まって、北米を世界市場成長の主要な貢献国として位置づけています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 外傷性脳損傷(TBI)の増加

- 神経疾患と頭蓋骨変形の有病率の増加

- 3Dプリンティングとカスタムインプラント技術の進歩

- 生体適合性およびスマート材料の採用増加

- 業界の潜在的リスク&課題

- 頭蓋インプラントと外科手術の高コスト

- 厳しい規制承認とコンプライアンス要件

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- カスタマイズ

- ノンカスタマイズ

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 金属

- ポリマー

- ポリエーテルエーテルケトン(PEEK)

- ポリメチルメタクリレート(PMMA)

- その他のポリマー

- セラミック

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 外傷性脳損傷

- 腫瘍切除症例

- 脳神経外科再建術

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 脳神経外科センター

- 学術・研究機関

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 3D Systems

- Acumed LLC

- Anatomics Pty Ltd

- B. Braun SE

- Brainlab

- evonos GmbH &Co. KG

- Integra LifeSciences

- Johnson &Johnson

- Kelyniam Global Inc.

- KLS Martin

- Medartis AG

- Medtronic

- Matrix Surgical USA

- Renishaw plc.

- Stryker Corporation

- Zimmer Biomet

The Global Cranial Implant Market was valued at USD 1.6 billion in 2024 and is projected to grow at a CAGR of 6.4% between 2025 and 2034. The market is experiencing steady growth, driven by the rising prevalence of neurological disorders, traumatic brain injuries, and the increasing adoption of advanced surgical techniques. A growing number of patients worldwide require cranial reconstruction due to conditions such as strokes, epilepsy, Alzheimer's disease, and congenital skull deformities. With an aging global population and an uptick in accident-related head injuries, demand for high-quality cranial implants is expected to surge. Continuous advancements in 3D printing and biomaterials are revolutionizing the industry, making implants more precise, durable, and biocompatible. Furthermore, favorable regulatory policies in developed markets are accelerating product approvals, allowing companies to introduce innovative solutions more efficiently. Increasing healthcare investments and improved accessibility to neuro and trauma care in emerging economies also contribute to market expansion.

The market is divided into customized and non-customized products. In 2024, customized cranial implants generated USD 1 billion and are set for notable growth, with a projected CAGR of 6.5% over the next decade. These implants are gaining popularity due to their ability to provide a precise fit, enhancing both reconstructive outcomes and functional performance. Using advanced imaging techniques such as CT scans and MRIs, medical professionals can create patient-specific implants that align seamlessly with an individual's skull structure. This personalized approach significantly improves post-surgical recovery and aesthetic results, fueling the demand for customized solutions across the healthcare sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.4% |

Cranial implants are primarily made from metal, polymer, or ceramic materials. The metal segment dominated the market in 2024, holding a 52.5% share and generating USD 830.9 million in revenue. Titanium and its alloys remain the preferred choice due to their exceptional strength, biocompatibility, and long-term durability. Metal implants offer superior protection to the brain, making them ideal for patients recovering from traumatic injuries or complex skull surgeries. Compared to polymer-based implants, metal options provide enhanced longevity and lower failure rates, driving their widespread adoption in medical procedures.

North America Cranial Implant Market generated USD 640.6 million in 2024 and is projected to reach USD 1.2 billion by 2034. This growth is largely driven by the increasing incidence of traumatic brain injuries (TBI) and the region's advanced healthcare infrastructure. The United States, in particular, benefits from a supportive regulatory environment that encourages the development and commercialization of cutting-edge medical technologies. The adoption of AI-assisted imaging, 3D printing, and bioengineered materials is reshaping the landscape of cranial implants, enabling more efficient and customized treatment options. These technological advancements, combined with strong healthcare spending and high awareness of neurosurgical solutions, position North America as a key contributor to global market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing cases of traumatic brain injuries (TBI)

- 3.2.1.2 Growing prevalence of neurological disorders and skull deformities

- 3.2.1.3 Advancements in 3D printing and custom implant technologies

- 3.2.1.4 Increasing adoption of biocompatible and smart materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of cranial implants and surgical procedures

- 3.2.2.2 Stringent regulatory approvals and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Customized

- 5.3 Non-customized

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Polymer

- 6.3.1 Polyetheretherketone (PEEK)

- 6.3.2 Polymethylmethacrylate (PMMA)

- 6.3.3 Other polymers

- 6.4 Ceramic

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Traumatic brain injuries

- 7.3 Tumor resection cases

- 7.4 Neurosurgical reconstructive procedures

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Neurosurgery centers

- 8.4 Academic and research institute

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3D Systems

- 10.2 Acumed LLC

- 10.3 Anatomics Pty Ltd

- 10.4 B. Braun SE

- 10.5 Brainlab

- 10.6 evonos GmbH & Co. KG

- 10.7 Integra LifeSciences

- 10.8 Johnson & Johnson

- 10.9 Kelyniam Global Inc.

- 10.10 KLS Martin

- 10.11 Medartis AG

- 10.12 Medtronic

- 10.13 Matrix Surgical USA

- 10.14 Renishaw plc.

- 10.15 Stryker Corporation

- 10.16 Zimmer Biomet