|

市場調査レポート

商品コード

1708143

自動車用ベルトテンショナープーリー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Belt Tensioner Pulleys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ベルトテンショナープーリー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月05日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

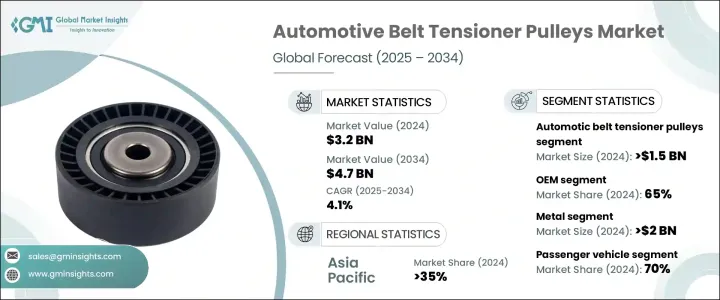

自動車用ベルトテンショナープーリーの世界市場は、2024年には32億米ドルとなり、2025年から2034年にかけてCAGR 4.1%で成長すると予測されています。

この市場は、乗用車や商用車の世界の生産の増加に牽引され、着実な成長を目の当たりにしています。自動車ベルトテンショナープーリーは、適切なベルト張力を維持し、摩耗や損傷を低減し、エンジン効率を最適化する上で重要な役割を果たしています。自動車メーカーは、高性能、低燃費、耐久性のあるエンジンに焦点を当てているように、これらのコンポーネントの需要が増加し続けています。

新興国を中心とした自動車産業の急速な拡大が、市場の成長をさらに後押ししています。排出ガスの削減と燃費の向上を目指した厳しい規制基準が、自動車メーカーに高度なテンショニング・ソリューションの統合を促しています。軽量かつ高耐久性材料を含むベルト駆動システムの技術革新は、ベルトテンショナプーリーの性能を強化しています。さらに、電気自動車やハイブリッド車の採用が増加しているため、市場力学が再構築され、高度なパワートレイン・システムに合わせた特殊なテンショニング・ソリューションの機会が生まれています。持続可能なモビリティとモジュラーエンジン設計へのシフトに伴い、メーカーは様々な動作条件下で一貫した性能を確保するベルトテンショナプーリーの開発に注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 32億米ドル |

| 予測金額 | 47億米ドル |

| CAGR | 4.1% |

市場は、自動ベルトテンショナープーリーと手動ベルトテンショナープーリーという2つの主要製品カテゴリーに区分されます。自動ベルトテンショナープーリーセグメントは、2024年に15億米ドルの評価額を獲得し、大きな市場シェアを占めています。これらの自動調整プーリーは、手動で介入することなく最適なベルト張力を維持し、エンジンの寿命と効率を向上させるため、車両のモデル全体で好まれています。現代の自動車では、低メンテナンス、高精度のコンポーネントの需要の増加が、このセグメントの拡大に拍車をかけています。

自動車ベルトテンショナープーリー市場はまた、相手先商標製品メーカー(OEM)とアフターマーケット販売を含む最終用途によって分類されます。2024年には、OEMセグメントが市場シェアの65%を占め、安定した成長が見込まれています。自動車メーカーは、エンジン性能を向上させ、燃費規制を満たし、耐久性を向上させるために、カスタム設計のベルトテンショナープーリーを統合しています。電気自動車やハイブリッド車の次世代エンジン設計とモジュラーベルト駆動システムのためのプッシュは、OEM分野における高度なテンショナプーリの採用を加速しています。

中国の自動車用ベルトテンショナープーリー市場は2024年に3億3,250万米ドルを生成し、主要な地域のプレーヤーとしての地位を固めました。同国は世界最大の自動車メーカーの一つであり、自動車の生産台数の増加と燃費の良い自動車に対する消費者の需要の増加は、高度なベルトテンショナープーリーシステムの必要性を後押ししています。ロジスティクスの成長とフリート管理プログラムによって駆動される商用車のフリートの拡大は、これらのコンポーネントの需要をさらに推進しています。自動車産業が進化し続けているように、ベルトテンショナプーリーは、様々な車両カテゴリ全体でシームレスなエンジン性能を確保するために不可欠なままです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- メーカー

- 部品サプライヤー

- サービスプロバイダー

- 流通業者

- 最終用途

- 利益率分析

- 技術革新の状況

- 主要ニュースと取り組み

- コスト分析

- 価格動向

- 材料性能の比較分析

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- 自動車生産台数とアフターマーケット需要の増加

- ベルトドライブシステムの進歩

- 電気自動車とハイブリッド車の需要増加

- 厳しい排ガス・燃費規制

- 業界の潜在的リスク&課題

- 耐久性と性能の限界

- 原材料価格の変動

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 自動ベルトテンショナープーリー

- 手動ベルトテンショナープーリー

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 金属

- プラスチック

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- エンジンタイミングシステム

- オルタネーターシステム

- パワーステアリングシステム

- エアコンシステム

- ウォーターポンプシステム

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ACDelco

- Bando Chemical Industries

- BorgWarner

- Cloyes Gear &Products

- Continental

- Dayco Products

- Fenner

- Gates

- Goodyear Belts

- Hutchinson

- INA Tensioner

- JTEKT

- Litens Automotive

- Mitsuboshi Belting

- NSK Automation

- NTN

- Pricol Limited

- Schaeffler

- SKF Group

- Tsubakimoto Chain

The Global Automotive Belt Tensioner Pulleys Market was valued at USD 3.2 billion in 2024 and is projected to grow at a CAGR of 4.1% between 2025 and 2034. This market is witnessing steady growth, driven by the increasing production of passenger and commercial vehicles worldwide. Automotive belt tensioner pulleys play a critical role in maintaining proper belt tension, reducing wear and tear, and optimizing engine efficiency. As vehicle manufacturers focus on high-performing, fuel-efficient, and durable engines, the demand for these components continues to rise.

The rapid expansion of the automotive industry, particularly in emerging economies, is further propelling market growth. Stringent regulatory standards aimed at reducing emissions and improving fuel efficiency have prompted automakers to integrate advanced tensioning solutions. Innovations in belt drive systems, including lightweight and high-durability materials, are enhancing the performance of belt tensioner pulleys. Additionally, the rising adoption of electric and hybrid vehicles is reshaping market dynamics, creating opportunities for specialized tensioning solutions tailored for advanced powertrain systems. With a shift towards sustainable mobility and modular engine designs, manufacturers are focusing on developing belt tensioner pulleys that ensure consistent performance under varying operating conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 4.1% |

The market is segmented into two primary product categories: automatic and manual belt tensioner pulleys. The automatic belt tensioner pulleys segment garnered a valuation of USD 1.5 billion in 2024, holding a significant market share. These self-adjusting pulleys are preferred across vehicle models as they maintain optimal belt tension without manual intervention, enhancing engine longevity and efficiency. The increasing demand for low-maintenance, high-precision components in modern vehicles is fueling the expansion of this segment.

The automotive belt tensioner pulleys market is also categorized by end-use applications, including original equipment manufacturers (OEM) and aftermarket sales. In 2024, the OEM segment accounted for 65% of the market share and is expected to grow steadily. Automakers are integrating custom-engineered belt tensioner pulleys to improve engine performance, meet fuel efficiency regulations, and enhance durability. The push for next-generation engine designs and modular belt drive systems in electric and hybrid vehicles is accelerating the adoption of advanced tensioner pulleys in the OEM sector.

China automotive belt tensioner pulleys market generated USD 332.5 million in 2024, cementing its position as a key regional player. With the country being one of the largest automotive manufacturers globally, rising vehicle production and increasing consumer demand for fuel-efficient automobiles are boosting the need for advanced belt tensioner pulley systems. The expansion of commercial vehicle fleets, driven by logistics growth and fleet management programs, is further driving demand for these components. As the automotive industry continues evolving, belt tensioner pulleys remain indispensable in ensuring seamless engine performance across various vehicle categories.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Component suppliers

- 3.2.3 Service providers

- 3.2.4 Distributors

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Cost analysis

- 3.7 Price trend

- 3.8 Comparative analysis of material performance

- 3.9 Patent analysis

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increasing vehicle production and aftermarket demand

- 3.11.1.2 Advancements in belt drive systems

- 3.11.1.3 Growing demand for electric and hybrid vehicles

- 3.11.1.4 Stringent emission and fuel efficiency regulations

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Durability and performance limitations

- 3.11.2.2 Fluctuations in raw material prices

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Automatic belt tensioner pulleys

- 5.3 Manual belt tensioner pulleys

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicle

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicle

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Metal

- 7.3 Plastic

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Engine timing system

- 8.3 Alternator system

- 8.4 Power steering system

- 8.5 Air conditioning system

- 8.6 Water pump system

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ACDelco

- 11.2 Bando Chemical Industries

- 11.3 BorgWarner

- 11.4 Cloyes Gear & Products

- 11.5 Continental

- 11.6 Dayco Products

- 11.7 Fenner

- 11.8 Gates

- 11.9 Goodyear Belts

- 11.10 Hutchinson

- 11.11 INA Tensioner

- 11.12 JTEKT

- 11.13 Litens Automotive

- 11.14 Mitsuboshi Belting

- 11.15 NSK Automation

- 11.16 NTN

- 11.17 Pricol Limited

- 11.18 Schaeffler

- 11.19 SKF Group

- 11.20 Tsubakimoto Chain