|

市場調査レポート

商品コード

1708139

ヘビーデューティ自律走行車市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Heavy-Duty Autonomous Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ヘビーデューティ自律走行車市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月05日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

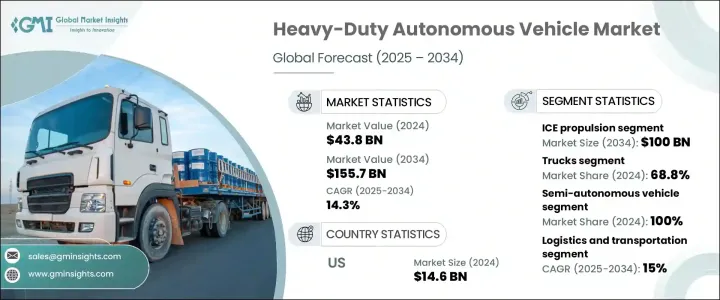

世界のヘビーデューティ自律走行車市場は2024年に438億米ドルに達し、2025年から2034年にかけてCAGR14.3%で拡大すると予測されています。

強化された安全機能に対する需要の高まりが、自動運転技術の採用の増加と相まって、この分野の大幅な成長を牽引しています。自律走行大型車は、最先端のセンサー、人工知能、リアルタイムのデータ分析を統合して道路を効率的にナビゲートすることで、輸送に革命をもたらしています。これらの高度なシステムにより、車両は周囲の状況を把握し、即座に判断を下し、ダイナミックな交通状況に適応して事故リスクを大幅に低減することができます。この自動化へのシフトは、交通安全を高めるだけでなく、ヒューマンエラーを最小限に抑え、死傷者の減少、ヘルスケアや物的損害の大幅なコスト削減につながります。

持続可能性と業務効率を重視する傾向が強まっているため、業界全体でヘビーデューティ自律走行車の導入がさらに加速しています。企業は労働力不足に対処し、長期的な経費を削減し、車両管理を最適化するために自動化を活用しています。AI主導の意思決定とリアルタイム・コネクティビティの進歩により、自律走行トラック・バスは物流、鉱業、建設、公共交通に不可欠な存在になりつつあります。世界各国の政府は、自律走行車の試験と商業展開を促進する規制と政策を導入しており、既存の輸送ネットワークへの安全でシームレスな統合を保証しています。さらに、5G接続、クラウドベースのモニタリング、機械学習アルゴリズムの急速な開発が業界を前進させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 438億米ドル |

| 予測金額 | 1,557億米ドル |

| CAGR | 14.3% |

同市場は、内燃機関車(ICE)、電気自動車、ハイブリッド車など、推進力の種類によって区分されます。2024年の市場シェアはICEが60%を占め、2034年には1,000億米ドルに達すると予想されます。ICEエンジン搭載の自律走行車は、その手頃な価格と確立された燃料補給インフラにより、初期段階の研究開発には依然として好ましい選択肢です。電気自動車に比べて航続距離が長いため、長距離運転や困難な地形に適しており、多様な環境での幅広い試験と採用が容易になっています。

車両タイプ別では、ヘビーデューティ自律走行車市場はトラックとバスに分類されます。トラックは2024年に68.8%と圧倒的なシェアを占めており、物流、鉱業、製造業などの産業で広く使用されていることがその要因となっています。自律走行トラックは休憩なしで連続運転が可能で、燃料消費を最適化し、配送を迅速化します。企業が効率とコスト削減を優先する中、自動運転トラックへのシフトはサプライチェーン進化の重要な要素になりつつあります。企業は輸送を合理化し、生産性を高め、労働力不足を緩和するため、自律走行トラック・ソリューションへの投資を増やしています。

北米のヘビーデューティ自律走行車市場は2024年に146億米ドルを生み出しました。政府の主導により、自律走行車のテストと大規模展開を支援するための規制枠組みが積極的に形成されています。交通安全と渋滞緩和への注目の高まりが、この地域の自動運転大型車需要を促進しています。自律走行技術が進化を続けるなか、北米は重要な市場として浮上しており、業界のリーダーたちは輸送とロジスティクスを再定義する次世代イノベーションに投資しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料メーカー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- コスト内訳分析

- 価格動向

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 鉱業と建設における自動化需要の高まり

- AIとセンサー技術の進歩

- より安全で持続可能な輸送のための規制強化

- インフラ整備への政府投資の拡大

- 業界の潜在的リスク&課題

- 高い初期投資コスト

- 規制と安全性への懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- トラック

- クラス7

- クラス8

- バス

第6章 市場推計・予測:自動運転レベル別、2021年~2034年

- 主要動向

- 半自律走行車

- レベル1

- レベル2

- レベル3

- 自律走行車

- レベル4

第7章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- ハイブリッド車

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 物流・輸送

- 鉱業

- 農業

- 建設

- 石油・ガス

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- 2getthere

- Aurora

- Baidu

- Caterpillar

- Daimler Truck

- Embark Trucks

- FAW

- General Motors

- Kodiak Robotics

- Navya ARMA

- New Flyer

- Oxa Autonomy

- PACCAR

- Schaeffler AG

- Torc Robotics

- TRATON

- TuSimple

- Volvo

- ZF Friedrichshafen

- Zoox

The Global Heavy-duty Autonomous Vehicle Market reached USD 43.8 billion in 2024 and is projected to expand at a CAGR of 14.3% between 2025 and 2034. The rising demand for enhanced safety features, coupled with the increasing adoption of self-driving technology, is driving substantial growth in this sector. Autonomous heavy-duty vehicles are revolutionizing transportation by integrating cutting-edge sensors, artificial intelligence, and real-time data analysis to navigate roads efficiently. These advanced systems allow vehicles to assess their surroundings, make instant decisions, and adapt to dynamic traffic conditions, significantly reducing accident risks. This shift toward automation not only enhances road safety but also minimizes human error, leading to fewer fatalities and injuries and substantial cost savings on healthcare and property damage.

The growing emphasis on sustainability and operational efficiency is further accelerating the adoption of heavy-duty autonomous vehicles across industries. Companies are leveraging automation to address labor shortages, reduce long-term expenses, and optimize fleet management. With advancements in AI-driven decision-making and real-time connectivity, autonomous trucks and buses are becoming integral to logistics, mining, construction, and public transportation. Governments worldwide are introducing regulations and policies to facilitate autonomous vehicle testing and commercial deployment, ensuring safe and seamless integration into existing transportation networks. Additionally, rapid developments in 5G connectivity, cloud-based monitoring, and machine learning algorithms are propelling the industry forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.8 Billion |

| Forecast Value | $155.7 Billion |

| CAGR | 14.3% |

The market is segmented based on propulsion types, including internal combustion engine (ICE), electric, and hybrid vehicles. In 2024, the ICE segment dominated with a 60% market share and is expected to generate USD 100 billion by 2034. ICE-powered autonomous vehicles remain the preferred choice for early-stage research and development due to their affordability and well-established refueling infrastructure. Their extended range compared to electric alternatives makes them more suitable for long-distance operations and challenging terrains, facilitating broader testing and adoption across diverse environments.

By vehicle type, the heavy-duty autonomous vehicle market is categorized into trucks and buses. Trucks held a dominant share of 68.8% in 2024, driven by their widespread use in industries such as logistics, mining, and manufacturing. Autonomous trucks offer continuous operation without breaks, optimizing fuel consumption and expediting deliveries. As businesses prioritize efficiency and cost reduction, the shift toward self-driving trucks is becoming a critical component of supply chain evolution. Companies are increasingly investing in autonomous trucking solutions to streamline transportation, enhance productivity, and mitigate workforce shortages.

North America heavy-duty autonomous vehicle market generated USD 14.6 billion in 2024. Government initiatives are actively shaping regulatory frameworks to support autonomous vehicle testing and large-scale deployment. The growing focus on road safety and congestion reduction is propelling demand for self-driving heavy-duty vehicles in this region. As autonomous technology continues to evolve, North America is emerging as a key market, with industry leaders investing in next-generation innovations to redefine transportation and logistics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End Use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Price trend

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for automation in mining and construction

- 3.8.1.2 Advancements in ai and sensor technologies

- 3.8.1.3 Regulatory push for safer and sustainable transport

- 3.8.1.4 Growing government investment in infrastructure development

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial investment costs

- 3.8.2.2 Regulatory and safety concerns

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Trucks

- 5.2.1 Class 7

- 5.2.2 Class 8

- 5.3 Buses

Chapter 6 Market Estimates & Forecast, By Level of Autonomy, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Semi-autonomous vehicle

- 6.2.1 Level 1

- 6.2.2 Level 2

- 6.2.3 Level 3

- 6.3 Autonomous vehicle

- 6.3.1 Level 4

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicle

- 7.4 Hybrid vehicle

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Logistics and transportation

- 8.3 Mining

- 8.4 Agriculture

- 8.5 Construction

- 8.6 Oil & gas

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 U.K.

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 2getthere

- 10.2 Aurora

- 10.3 Baidu

- 10.4 Caterpillar

- 10.5 Daimler Truck

- 10.6 Embark Trucks

- 10.7 FAW

- 10.8 General Motors

- 10.9 Kodiak Robotics

- 10.10 Navya ARMA

- 10.11 New Flyer

- 10.12 Oxa Autonomy

- 10.13 PACCAR

- 10.14 Schaeffler AG

- 10.15 Torc Robotics

- 10.16 TRATON

- 10.17 TuSimple

- 10.18 Volvo

- 10.19 ZF Friedrichshafen

- 10.20 Zoox