インシュアテック市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Insurtech Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708132

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

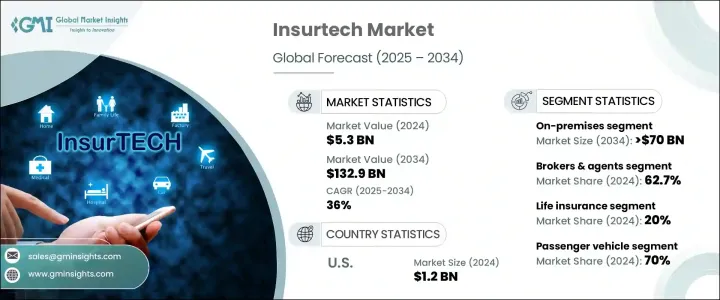

世界のインシュアテック市場は2024年に53億米ドルと評価され、2025年から2034年にかけてCAGR36%で成長すると予測されています。

この目覚ましい拡大には、人工知能(AI)や機械学習(ML)といった最先端技術の急速な導入が拍車をかけており、これらは保険の展望を再定義しつつあります。デジタルトランスフォーメーションが加速する中、インシュアテック企業はAI主導の自動化を活用して効率性を高め、保険金請求を合理化し、顧客とのやり取りを改善しています。このような進歩は、運用コストを大幅に削減し、不正行為の検出を改善することで、保険サービスをより迅速に、より安全に、より顧客本位にします。モバイル・アプリケーション、チャットボット、高度な分析プラットフォームの浸透は、保険契約者にシームレスなデジタル体験を提供し、この分野の開発にさらに貢献しています。

規制当局の支援と消費者の嗜好の進化も、インシュアテック市場の軌跡を形作っています。世界中の政府や金融規制当局がデジタル保険ソリューションを支持し、コンプライアンス要件を緩和し、伝統的な保険会社と新興企業間の競争を促しています。消費者は、リアルタイムの保険金請求追跡、パーソナライズされた保険契約の提案、迅速な紛争解決などを提供するテクノロジー主導の保険モデルにますます惹かれています。利用ベースの保険(UBI)、パラメトリック保険、組み込み型保険ソリューションの需要が急増し、この分野のイノベーションを促進しています。さらに、インシュアテック企業と既存の保険プロバイダーとのパートナーシップがハイブリッド・ソリューションの開発を促進し、デジタルの利便性と伝統的なリスク評価のバランスを確保しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億米ドル |

| 予測金額 | 1,329億米ドル |

| CAGR | 36% |

市場は展開モデルによって分類され、オンプレミスとクラウドベースのソリューションがセグメントをリードしています。オンプレミスの市場シェアは60%で、2034年には700億米ドルに達すると予測されています。この優位性は、オンプレミス・インフラストラクチャが提供するセキュリティ強化によるところが大きく、機密性の高い顧客データやビジネス・データを扱う業界にとっては依然として重要です。金融機関、ヘルスケアプロバイダー、保険会社は、GDPR、HIPAA、PCI-DSSなどの規制枠組みへのコンプライアンスを確保するため、オンプレミスのソリューションを優先しています。これらの規制では厳格なデータ保護対策が必要となるため、データ管理とサイバーセキュリティを優先する企業にとって、オンプレミスの導入は魅力的な選択肢となっています。

インシュアテック市場は、ブローカー・代理店、D2C(Direct-to-Consumer)、その他の販売チャネルによっても区分されます。ブローカー・代理店セグメントは2024年の市場シェアで62.7%を占め、保険取引における人間の専門知識が引き続き重要であることを裏付けています。ブローカーと代理店は、複雑な保険契約体系を持つ顧客を支援し、個々の顧客に合ったアドバイスを提供し、リスク評価をナビゲートする上で重要な役割を果たしています。カスタマイズされた補償ソリューションを交渉する彼らの能力は、特に高額保険カテゴリーにおいて、デジタル専用モデルに対する競争優位性を提供します。自動化された保険プラットフォームが台頭しているとはいえ、多くの消費者は包括的な補償と経済的な安全性を確保するために、個別の相談を好みます。

北米のインシュアテック市場は2024年に12億米ドルを創出し、米国がこの分野で圧倒的な力を持つようになりました。同国の確立された保険業界は、高度な技術インフラと相まって、世界のインシュアテックイノベーションの最前線に位置しています。米国の規制環境は、デジタル保険の導入を促進し、新興企業が革新的なソリューションを開発するインセンティブを与える競合エコシステムを育んでいます。AIを活用したアンダーライティング、ブロックチェーンを活用したスマートコントラクト、IoTを活用したリスク評価などを重視する米国は、インシュアテックの未来を形成し続けています。これらの要因は、ベンチャーキャピタルや金融機関からの投資の増加と相まって、デジタル保険革命における北米のリーダーシップを確固たるものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- テクノロジープロバイダー

- 保険プロバイダー

- 流通業者

- エンドユース

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- 使用事例

- 規制状況

- 影響要因

- 促進要因

- AI、ブロックチェーン、IoT、クラウドコンピューティングを活用したデジタルトランスフォーメーション

- パーソナライズされた柔軟な保険ソリューションへの需要の高まり

- イノベーションを促進する投資とパートナーシップの増加

- デジタル・イノベーションを支援する規制イニシアチブ

- 業界の潜在的リスク&課題

- データ・セキュリティとプライバシーに関する懸念

- レガシーシステムとの統合と複雑な規制要件への対応

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 医療保険

- 生命保険

- 損害保険

- 自動車保険

- 特殊保険

- 再保険

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 人工知能(AI)と機械学習(ML)

- ビッグデータ&アナリティクス

- ブロックチェーン

- モノのインターネット(IoT)

- テレマティクス

- クラウド・コンピューティング

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- ダイレクト・ツー・コンシューマー(D2C)

- ブローカーおよびエージェント

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alan

- BIMA

- Bolttech

- Bright Health Group

- Clover Health

- Coalition

- Cover Genius

- Duck Creek Technologies

- GoHealth

- Hippo Insurance

- Lemonade

- Metromile

- Next Insurance

- Oscar Health

- PolicyBazaar

- Root Insurance

- Shift Technology

- Trov

- Wefox

- ZhongAn Insurance

目次

The Global Insurtech Market was valued at USD 5.3 billion in 2024 and is projected to grow at a CAGR of 36% between 2025 and 2034. This impressive expansion is fueled by the rapid adoption of cutting-edge technologies like artificial intelligence (AI) and machine learning (ML), which are redefining the insurance landscape. As digital transformation accelerates, Insurtech firms are leveraging AI-driven automation to enhance efficiency, streamline claim processing, and improve customer interactions. These advancements significantly reduce operational costs and improve fraud detection, making insurance services faster, more secure, and more customer-centric. The growing penetration of mobile applications, chatbots, and advanced analytics platforms further contributes to the sector's development, offering policyholders seamless digital experiences.

Regulatory support and evolving consumer preferences also shape the Insurtech market's trajectory. Governments and financial regulators worldwide endorse digital insurance solutions, easing compliance requirements, and encouraging competition among traditional insurers and startups. Consumers are increasingly drawn to tech-driven insurance models that provide real-time claim tracking, personalized policy recommendations, and swift dispute resolutions. The demand for usage-based insurance (UBI), parametric insurance, and embedded insurance solutions is surging, driving innovation in the sector. Additionally, partnerships between Insurtech firms and established insurance providers are fostering the development of hybrid solutions, ensuring a balance between digital convenience and traditional risk assessment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $132.9 Billion |

| CAGR | 36% |

The market is categorized based on deployment models, with on-premises and cloud-based solutions leading the segment. The on-premises segment held a 60% market share and is forecasted to generate USD 70 billion by 2034. This dominance is largely due to the enhanced security offered by on-premises infrastructure, which remains critical for industries handling sensitive customer and business data. Financial institutions, healthcare providers, and insurance companies prioritize on-premises solutions to ensure compliance with regulatory frameworks like GDPR, HIPAA, and PCI-DSS. These regulations necessitate stringent data protection measures, making on-premises deployment an attractive choice for enterprises prioritizing data control and cybersecurity.

The Insurtech market is also segmented by distribution channels, which include brokers & agents, Direct-to-Consumer (D2C), and other methods. The brokers & agents segment held a 62.7% market share in 2024, underscoring the continued relevance of human expertise in insurance transactions. Brokers and agents play a vital role in assisting clients with complex policy structures, providing tailored advice, and helping customers navigate risk assessments. Their ability to negotiate customized coverage solutions offers a competitive edge over digital-only models, particularly in high-value insurance categories. Despite the rise of automated insurance platforms, many consumers still prefer personalized consultation to ensure comprehensive coverage and financial security.

North America Insurtech market generated USD 1.2 billion in 2024, with the United States emerging as a dominant force in the sector. The country's well-established insurance industry, coupled with its advanced technological infrastructure, positions it at the forefront of global Insurtech innovation. The U.S. regulatory environment fosters a competitive ecosystem that encourages digital insurance adoption and incentivizes startups to develop innovative solutions. With a strong emphasis on AI-driven underwriting, blockchain-based smart contracts, and IoT-powered risk assessments, the U.S. continues to shape the future of Insurtech. These factors, combined with increasing investments from venture capitalists and financial institutions, solidify North America's leadership in the digital insurance revolution.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology providers

- 3.1.1.2 Insurance providers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Use cases

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Digital transformation using AI, blockchain, IoT, and cloud computing

- 3.6.1.2 Growing demand for personalized and flexible insurance solutions

- 3.6.1.3 Increased investments and partnerships fuelling innovation

- 3.6.1.4 Regulatory initiatives supporting digital innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Data security and privacy concerns

- 3.6.2.2 Integration with legacy systems and navigating complex regulatory requirements

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Health insurance

- 5.3 Life insurance

- 5.4 Property & casualty (P&C) insurance

- 5.5 Auto insurance

- 5.6 Specialty insurance

- 5.7 Reinsurance

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Artificial intelligence (AI) & machine learning (ML)

- 6.3 Big data & analytics

- 6.4 Blockchain

- 6.5 Internet of things (IoT)

- 6.6 Telematics

- 6.7 Cloud computing

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-Premises

- 7.3 Cloud-Based

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Direct-to-Consumer (D2C)

- 8.3 Brokers & agents

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alan

- 10.2 BIMA

- 10.3 Bolttech

- 10.4 Bright Health Group

- 10.5 Clover Health

- 10.6 Coalition

- 10.7 Cover Genius

- 10.8 Duck Creek Technologies

- 10.9 GoHealth

- 10.10 Hippo Insurance

- 10.11 Lemonade

- 10.12 Metromile

- 10.13 Next Insurance

- 10.14 Oscar Health

- 10.15 PolicyBazaar

- 10.16 Root Insurance

- 10.17 Shift Technology

- 10.18 Trov

- 10.19 Wefox

- 10.20 ZhongAn Insurance

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日