デジタルヘルスの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測

Digital Health Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699400

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

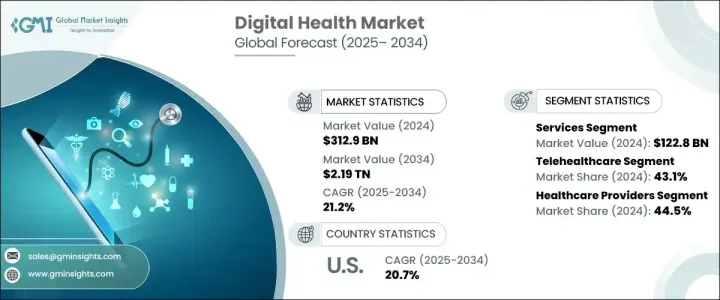

世界のデジタルヘルス市場は2024年に3,129億米ドルとなり、2025年から2034年にかけてCAGR21.2%で拡大する見通しです。

この著しい成長は、ヘルスケアにおける最先端のデジタル技術の統合が進んでいることに起因しています。人工知能(AI)、ビッグデータ分析、クラウドコンピューティング、モノのインターネット(IoT)は業界を変革し、効率化を促進し、患者ケアを強化しています。アクセス性の向上、費用対効果の高い治療、リアルタイムの患者モニタリングの必要性に後押しされ、デジタルヘルスソリューションの需要は急増し続けています。デジタルヘルスケアソリューションの急速な進化は、業務効率の改善だけでなく、患者エンゲージメントを再定義し、より個別化されたデータ主導の医療アプローチへの道を開いています。

世界中の政府や民間投資家がデジタルヘルス構想に多額の資金を提供しており、市場の拡大をさらに加速させています。テレヘルスの導入、AI主導の診断、デジタル治療法を支援する強力な政策枠組みは、ヘルスケア提供の再形成において極めて重要な役割を果たしています。コネクテッドデバイスとモバイルヘルス(mヘルス)アプリケーションの台頭は、患者の行動に大きな影響を与え、予防医療と遠隔医療モデルへのシフトを促しています。さらに、慢性疾患の増加と高齢化により、デジタルヘルスプラットフォームの需要が高まっており、現代のヘルスケアエコシステムには欠かせない要素となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 3,129億米ドル |

| 予測金額 | 2兆1,900億米ドル |

| CAGR | 21.2% |

デジタルヘルス市場は、ハードウェア、ソフトウェア、サービスの3つの中核要素に分類されます。サービス分野は、2024年に1,228億米ドルと評価され、2034年までCAGR21.3%で成長すると予測されます。この拡大は、遠隔患者モニタリング、遠隔医療、ヘルスケア分析に対する需要の急増が原動力となっています。AIやIoTなどの先進技術の統合により、デジタル医療サービスは業務を合理化し、ケア提供を強化し、患者と医療者のシームレスな交流を促進しています。ヘルスケア組織がワークフローを最適化し、患者の転帰を改善しようとする中、デジタルサービスは効率的かつ積極的な医療介入を可能にする重要な存在になりつつあります。

遠隔医療、モバイルヘルス(mヘルス)、健康分析、デジタルヘルスシステムは、依然として業界の進歩の最前線にあります。遠隔医療分野は2024年に市場シェアの43.1%を占め、これは仮想診察、遠隔診断、遠隔医療プラットフォームへの依存の高まりに後押しされています。COVID-19の流行は、これらの技術の採用を加速させ、アクセス可能でスケーラブルなヘルスケアソリューションの必要性を浮き彫りにしました。その結果、ヘルスケアプロバイダーは世界的に遠隔医療サービスを統合し、リーチを拡大し、患者がタイムリーで費用対効果の高い医療を受けられるよう、ケアへのアクセシビリティを高め続けています。

米国のデジタルヘルス市場は、2024年に1,236億米ドルを生み出し、2025年から2034年のCAGRは20.7%と予測されています。同国は、強力な規制の枠組み、高い投資水準、高度なデジタルインフラに支えられ、デジタルヘルスケアの導入における世界的リーダーであり続けています。AIを活用した診断ツール、遠隔患者モニタリングソリューション、データ駆動型ヘルスケアモデルの広範な導入により、米国市場の優位性は確固たるものとなっています。次世代技術の統合が進み、価値観に基づく医療が強力に推進される中、米国のデジタル医療分野は持続的な成長を遂げ、世界市場の牽引役としての地位を強化するものと思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 遠隔患者モニタリングサービスに対する需要の高まり

- スマートフォンの普及とインターネット接続の増加

- デジタルヘルスにおける政府の積極的な取り組みと資金提供

- ベンチャーキャピタルからの投資の増加

- 業界の潜在的リスク・課題

- データのプライバシーとセキュリティに関する懸念

- 高い導入コスト

- 成長促進要因

- 成長可能性分析

- 市場参入の情勢

- 規制状況

- 米国

- 欧州

- 投資分析:地域別

- 米国

- 欧州

- アジア太平洋

- 合併・買収の状況

- 償還シナリオ

- デジタルヘルスプロジェクト/イニシアティブ

- テクノロジー情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場マトリックス分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- クラウドベース

- オンプレミス

- サービス

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- テレヘルスケア

- 遠隔介護

- 活動モニタリング

- 遠隔服薬管理

- 遠隔医療

- LTCモニタリング

- ビデオ相談

- 遠隔介護

- mヘルス

- ウェアラブルと接続された医療機器

- 血圧モニター

- 心拍数モニター

- 血糖値モニター

- パルスオキシメーター

- 睡眠トラッカー

- 神経モニター

- その他のウェアラブルと接続された医療機器

- mヘルスアプリ

- 医療アプリ

- 女性の健康アプリ

- 慢性疾患管理アプリ

- 個人健康記録アプリ

- 投薬管理アプリ

- 遠隔モニタリングアプリ

- その他の医療アプリ

- フィットネスアプリ

- 医療アプリ

- ウェアラブルと接続された医療機器

- 健康分析

- 予測分析

- 処方的分析

- 記述的分析

- デジタルヘルスシステム

- 電子カルテ(EHR)

- 電子処方システム

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- ヘルスケアプロバイダー

- 患者

- 支払者

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Accenture

- AMD Global Telemedicine

- American Well(Amwell)

- Athenahealth

- Capsa Healthcare

- Eagle Telemedicine

- Firstbeat Technologies

- GE Healthcare

- Health Catalyst

- Honeywell International

- IBM

- iHealth Lab

- Koninklijke Philips N.V.

- McKesson Corporation

- Oracle(Cerner Corporation)

- Qualcomm Technologies

- Teladoc Health

- Veradigm LLC(Allscripts Healthcare Solutions)

目次

The Global Digital Health Market was valued at USD 312.9 billion in 2024 and is poised to expand at a CAGR of 21.2% between 2025 and 2034. This remarkable growth stems from the increasing integration of cutting-edge digital technologies in healthcare. Artificial intelligence (AI), big data analytics, cloud computing, and the Internet of Things (IoT) are transforming the industry, driving efficiency, and enhancing patient care. The demand for digital health solutions continues to surge, fueled by the need for improved accessibility, cost-effective treatments, and real-time patient monitoring. The rapid evolution of digital healthcare solutions is not just improving operational efficiency but also redefining patient engagement, paving the way for more personalized and data-driven medical approaches.

Governments and private investors worldwide are heavily funding digital health initiatives, further accelerating the market's expansion. Strong policy frameworks supporting telehealth adoption, AI-driven diagnostics, and digital therapeutics are playing a pivotal role in reshaping healthcare delivery. The rise of connected devices and mobile health (mHealth) applications has significantly influenced patient behaviors, prompting a shift toward preventive and remote care models. Additionally, the increasing prevalence of chronic diseases and aging populations has heightened the demand for digital health platforms, making them indispensable components of modern healthcare ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $312.9 Billion |

| Forecast Value | $2.19 trillion |

| CAGR | 21.2% |

The digital health market is categorized into three core components: hardware, software, and services. The services segment, valued at USD 122.8 billion in 2024, is expected to grow at a CAGR of 21.3% through 2034. This expansion is driven by the soaring demand for remote patient monitoring, telehealth, and healthcare analytics. With the integration of advanced technologies such as AI and IoT, digital health services are streamlining operations, enhancing care delivery, and fostering seamless patient-provider interactions. As healthcare organizations seek to optimize workflows and improve patient outcomes, digital services are becoming a critical enabler of efficient and proactive medical interventions.

Telehealthcare, mobile health (mHealth), health analytics, and digital health systems remain at the forefront of industry advancements. The telehealthcare segment accounted for 43.1% of the market share in 2024, propelled by the growing reliance on virtual consultations, remote diagnostics, and telemedicine platforms. The COVID-19 pandemic accelerated the adoption of these technologies, highlighting the necessity of accessible and scalable healthcare solutions. As a result, healthcare providers globally continue to integrate telehealth services to expand their reach and enhance care accessibility, ensuring patients receive timely and cost-effective medical attention.

The U.S. digital health market generated USD 123.6 billion in 2024, with a projected CAGR of 20.7% between 2025 and 2034. The country remains a global leader in digital healthcare adoption, backed by strong regulatory frameworks, high investment levels, and an advanced digital infrastructure. The widespread implementation of AI-powered diagnostic tools, remote patient monitoring solutions, and data-driven healthcare models has cemented the U.S. market's dominance. With the increasing integration of next-gen technologies and a robust push toward value-based care, the digital health sector in the U.S. is set to experience sustained growth, reinforcing its position as a driving force in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for remote patient monitoring services

- 3.2.1.2 Increasing smartphone penetration and internet connectivity

- 3.2.1.3 Favorable government initiatives and fundings in digital health

- 3.2.1.4 Growing venture capital investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 High implementation cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Market entry landscape

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.6 Investment analysis, by region

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.7 Merger and acquisition landscape

- 3.8 Reimbursement scenario

- 3.9 Digital health project/initiatives

- 3.10 Technology landscape

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.3.1 Cloud-based

- 5.3.2 On-premises

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Telehealthcare

- 6.2.1 Telecare

- 6.2.1.1 Activity monitoring

- 6.2.1.2 Remote medication management

- 6.2.2 Telehealth

- 6.2.2.1 LTC monitoring

- 6.2.2.2 Video consultation

- 6.2.1 Telecare

- 6.3 mHealth

- 6.3.1 Wearables and connected medical devices

- 6.3.1.1 Blood pressure monitors

- 6.3.1.2 Heart rate monitors

- 6.3.1.3 Blood glucose monitor

- 6.3.1.4 Pulse oximeters

- 6.3.1.5 Sleep trackers

- 6.3.1.6 Neurological monitors

- 6.3.1.7 Other wearables and connected medical devices

- 6.3.2 mHealth apps

- 6.3.2.1 Medical apps

- 6.3.2.1.1 Womens health apps

- 6.3.2.1.2 Chronic disease management apps

- 6.3.2.1.3 Personal health record apps

- 6.3.2.1.4 Medication management apps

- 6.3.2.1.5 Remote monitoring apps

- 6.3.2.1.6 Other medical apps

- 6.3.2.2 Fitness apps

- 6.3.2.1 Medical apps

- 6.3.1 Wearables and connected medical devices

- 6.4 Health analytics

- 6.4.1 Predictive analytics

- 6.4.2 Prescriptive analytics

- 6.4.3 Descriptive analytics

- 6.5 Digital health systems

- 6.5.1 Electronic health records (EHRs)

- 6.5.2 e-prescribing systems

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare providers

- 7.3 Patients

- 7.4 Payers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accenture

- 9.2 AMD Global Telemedicine

- 9.3 American Well (Amwell)

- 9.4 Athenahealth

- 9.5 Capsa Healthcare

- 9.6 Eagle Telemedicine

- 9.7 Firstbeat Technologies

- 9.8 GE Healthcare

- 9.9 Health Catalyst

- 9.10 Honeywell International

- 9.11 IBM

- 9.12 iHealth Lab

- 9.13 Koninklijke Philips N.V.

- 9.14 McKesson Corporation

- 9.15 Oracle (Cerner Corporation)

- 9.16 Qualcomm Technologies

- 9.17 Teladoc Health

- 9.18 Veradigm LLC (Allscripts Healthcare Solutions)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日