|

市場調査レポート

商品コード

1699360

ヘルスケアデータ収益化ソリューション市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Healthcare Data Monetization Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| ヘルスケアデータ収益化ソリューション市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

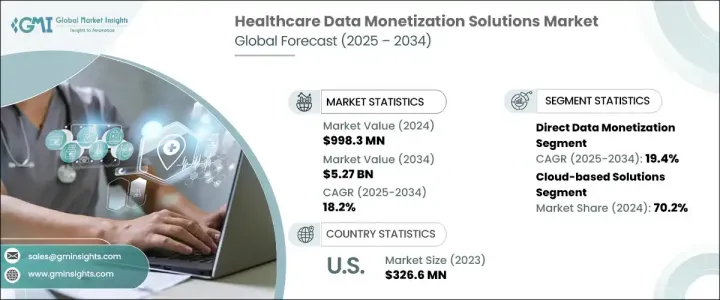

世界のヘルスケアデータ収益化ソリューション市場は、2024年には9億9,830万米ドルとなり、2025年から2034年にかけてCAGR 18.2%で成長すると予測されています。

ヘルスケア業界はデジタル革命の真っただ中にあり、データ収益化が重要な促進要因として浮上しています。電子カルテ(EHR)、AIを活用した診断、コネクテッド医療機器の導入が進むなか、ヘルスケア機関は膨大な量のデータを生み出しています。企業はこのデータの価値を認識し、新たな収益源の開発、患者ケアの最適化、業務効率の向上に活用しています。

ヘルスケアデータ収益化ソリューションに対する需要は、デジタルプラットフォームの進歩、クラウドベースのサービスの普及、テクノロジープロバイダーと医療機関の戦略的提携によって高まっています。ヘルスケアシステムがかつてない量の患者データを生成・保存する中、企業はアナリティクス、AI、機械学習を活用して実用的な知見を引き出そうとしています。これらの洞察により、製薬会社、保険会社、ヘルスケアプロバイダーはデータ主導の意思決定を行い、業務を合理化し、患者の転帰を改善することができます。規制機関が厳格なコンプライアンス対策を実施する中、企業は進化する市場情勢の中で競争力を維持するため、安全でスケーラブル、かつコンプライアンスに準拠したデータ収益化ソリューションに投資しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9億9,830万米ドル |

| 予測金額 | 52億7,000万米ドル |

| CAGR | 18.2% |

直接データ収益化分野は大幅な成長が見込まれ、予測期間中のCAGRは19.4%と予測されます。開発企業は、新サービスの開発、製品オファリングの最適化、業務効率の改善などを通じて、独自のデータを活用する傾向を強めています。直接収益化により、ヘルスケア機関は非識別化された患者データの販売、分析サービスの提供、研究目的のデータセットのライセンス供与によって収益を上げることができます。一方、間接データ収益化も依然として重要な戦略であり、企業はデータインサイトを活用してマーケティング活動を強化し、顧客エンゲージメントを促進し、ビジネスの意思決定プロセスを改善します。

ヘルスケアデータの収益化市場では、クラウドベースのソリューションが引き続き優位を占めており、2024年の市場シェアは70%に達します。クラウド技術への信頼が高まっているのは、コスト効率が高く、拡張性があり、簡単にアクセスできるソリューションを提供できるからです。クラウドベースのプラットフォームにより、ヘルスケアプロバイダーはデータをリモートで管理・分析できるようになり、高価なオンプレミスインフラを必要としなくなります。自動更新、強化されたセキュリティ機能、AI主導の分析ツールとのシームレスな統合により、クラウドベースのデータ収益化ソリューションは、ヘルスケア部門のデータ資産の管理と活用方法に革命をもたらしています。

米国のヘルスケアデータ収益化ソリューション市場の2022年の市場規模は2億8,020万米ドルで、北米をリードし続けています。同国の確立されたヘルスケアインフラは、デジタルトランスフォーメーションイニシアチブの早期導入と相まって、データ主導型ソリューションへの需要を加速させています。米国中のヘルスケア機関は、AIを活用したアナリティクス、予測モデリング、ブロックチェーン技術を活用し、患者データを安全かつ確実に収益化しています。ヘルスケアセクターの進化に伴い、データ収益化は収益創出戦略の不可欠な要素となりつつあり、米国はこの急拡大する市場のフロントランナーとして位置づけられています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 電子カルテ(EHR)の採用拡大

- デジタルヘルスソリューションの普及

- データ分析の技術的進歩

- デジタルヘルス収益化プロジェクトを合理化するAI主導型ソリューションのダイナミックな採用

- 業界の潜在的リスク&課題

- 規制上の制約

- データプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- 技術的展望

- 規制状況

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 直接データ収益化

- 間接的データ収益化

第6章 市場推計・予測:展開タイプ別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:アプリケーション別、2021年~2032年

- 主要動向

- 予測分析と疾病管理

- ポピュレーションヘルス管理

- 収益サイクル管理

- 精密医療

- その他のアプリケーション

第8章 市場推計・予測:データタイプ別、2021年~2034年

- 主要動向

- 臨床データ

- 請求データ

- EHRデータ

- ゲノムデータ

- その他のデータタイプ

第9章 市場推計・予測:最終用途別、2021年~2032年

- 製薬・バイオテクノロジー企業

- ヘルスケア支払者

- ヘルスケアプロバイダー

- 医療技術企業

- その他の最終用途

第10章 市場推計・予測:地域別、2021年~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Accenture

- H1

- IBM

- Infor

- Innovaccer

- LexisNexis Risk Solutions

- Microsoft

- Oracle

- Salesforce

- SAS Institute

- Siemens Healthineers

- Snowflake

- Thoughtspot

- Verato

The Global Healthcare Data Monetization Solutions Market was valued at USD 998.3 million in 2024 and is projected to grow at a CAGR of 18.2% between 2025 and 2034. The healthcare industry is undergoing a digital revolution, and data monetization is emerging as a crucial growth driver. With the increasing adoption of electronic health records (EHRs), AI-powered diagnostics, and connected medical devices, healthcare institutions are generating vast amounts of data. Companies are recognizing the value of this data, using it to develop new revenue streams, optimize patient care, and enhance operational efficiency.

The demand for healthcare data monetization solutions is being fueled by advancements in digital platforms, the proliferation of cloud-based services, and strategic collaborations between technology providers and healthcare organizations. As healthcare systems generate and store an unprecedented amount of patient data, businesses are leveraging analytics, AI, and machine learning to extract actionable insights. These insights are enabling pharmaceutical companies, insurers, and healthcare providers to make data-driven decisions, streamline operations, and improve patient outcomes. With regulatory bodies enforcing stringent compliance measures, organizations are investing in secure, scalable, and compliant data monetization solutions to remain competitive in the evolving market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $998.3 Million |

| Forecast Value | $5.27 Billion |

| CAGR | 18.2% |

The direct data monetization segment is expected to witness substantial growth, with a projected CAGR of 19.4% during the forecast period. Businesses are increasingly capitalizing on their proprietary data by developing new services, optimizing product offerings, and improving operational efficiencies. Direct monetization allows healthcare organizations to generate revenue by selling de-identified patient data, offering analytics-as-a-service, and licensing datasets for research purposes. Meanwhile, indirect data monetization remains a critical strategy, as companies utilize data insights to enhance marketing efforts, drive customer engagement, and improve business decision-making processes.

Cloud-based solutions continue to dominate the healthcare data monetization market, holding a 70% market share in 2024. The growing reliance on cloud technology stems from its ability to offer cost-effective, scalable, and easily accessible solutions. Cloud-based platforms empower healthcare providers to manage and analyze data remotely, eliminating the need for expensive on-premises infrastructure. With automatic updates, enhanced security features, and seamless integration with AI-driven analytics tools, cloud-based data monetization solutions are revolutionizing how the healthcare sector manages and leverages data assets.

The U.S. Healthcare Data Monetization Solutions Market was valued at USD 280.2 million in 2022 and continues to lead North America. The country's well-established healthcare infrastructure, coupled with its early adoption of digital transformation initiatives, has accelerated the demand for data-driven solutions. Healthcare institutions across the U.S. are leveraging AI-powered analytics, predictive modeling, and blockchain technology to monetize patient data securely and compliantly. As the healthcare sector evolves, data monetization is becoming an integral component of revenue generation strategies, positioning the U.S. as a frontrunner in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of electronic health records (EHRs)

- 3.2.1.2 Growing adoptability of digital health solutions

- 3.2.1.3 Technological advancement in data analysis

- 3.2.1.4 Dynamic adoption of AI-driven solutions streamlining digital health monetization projects

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory constraints

- 3.2.2.2 Data privacy and security concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological landscape

- 3.5 Regulatory landscape

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Direct data monetization

- 5.3 Indirect data monetization

Chapter 6 Market Estimates and Forecast, By Deployment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Predictive analytics and disease management

- 7.3 Population health management

- 7.4 Revenue cycle management

- 7.5 Precision medicine

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Data Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical data

- 8.3 Claims data

- 8.4 EHR data

- 8.5 Genomic data

- 8.6 Other data types

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2032 ($ Mn)

- 9.1 Pharmaceutical and biotechnology companies

- 9.2 Healthcare payers

- 9.3 Healthcare providers

- 9.4 Medical technology companies

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2032 ($ Mn

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Accenture

- 11.2 Google

- 11.3 H1

- 11.4 IBM

- 11.5 Infor

- 11.6 Innovaccer

- 11.7 LexisNexis Risk Solutions

- 11.8 Microsoft

- 11.9 Oracle

- 11.10 Salesforce

- 11.11 SAS Institute

- 11.12 Siemens Healthineers

- 11.13 Snowflake

- 11.14 Thoughtspot

- 11.15 Verato