EaaS(Energy as a Service)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Energy as a Service (EaaS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699261

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

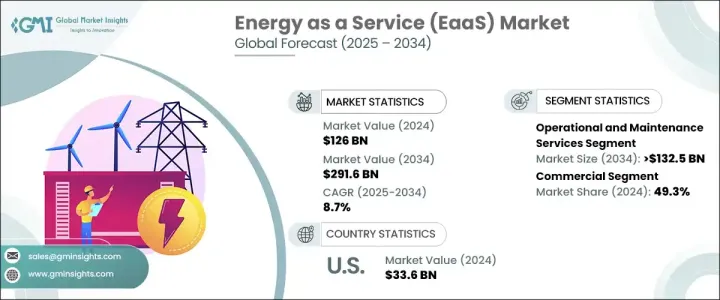

世界のEaaS(Energy As A Service)市場は、2024年に1,260億米ドルの評価額に達し、2025年から2034年にかけてCAGR 8.7%で成長すると予測されています。

この成長の原動力となっているのは、持続可能性へのシフトの高まりであり、政府による支援策や各業界におけるエネルギー需要の急増によって強化されています。企業や機関は、消費を最適化し効率を高めるために、費用対効果が高く弾力性のある分散型エネルギー・ソリューションを積極的に求めています。サブスクリプション・ベースのエネルギー・サービス・モデルは、長期的なコスト削減と運用上の利点をもたらすことから、支持を集めています。市場力学は、エネルギー効率化、送電網の近代化、デジタル・トランスフォーメーションを重視する傾向が強まっていることも影響しています。IoTセンサー、予知保全ツール、リアルタイム分析などの先進技術の統合が進むにつれ、エネルギー管理が改善され、EaaSソリューションが企業にとってより現実的なものとなっています。世界各国の政府も、持続可能なエネルギーへの取り組みを促進するため、厳しいエネルギー規制や資金提供プログラムを実施しており、これが導入をさらに促進しています。二酸化炭素排出量の削減とエネルギー回復力の向上への注目が高まる中、柔軟でスケーラブルなEaaSモデルへの需要が高まり、今後10年間の持続的な市場拡大の舞台が整いつつあります。

この業界は、エネルギー供給サービス、運用・保守サービス、エネルギー効率化・最適化サービスに分類されます。運用・保守サービスは、エネルギー・システムの信頼性と性能を確保する上で重要な役割を果たします。これらのサービスは、企業が効率性と持続可能性を高めるソリューションを優先するため、2034年までに1,325億米ドルを生み出すと予測されています。継続的なエネルギー供給、最適化されたオペレーション、ダウンタイムの最小化を提供することで、これらのサービスは、費用対効果を維持しながらより良いエネルギー管理を達成するのに役立っています。シームレスなインフラ・メンテナンスと運用サポートに対するニーズの高まりが普及の原動力となっており、企業はリスクを削減し、長期的なエネルギー性能を向上させることができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,260億米ドル |

| 予測金額 | 2,916億米ドル |

| CAGR | 8.7% |

最終用途の観点から、市場は住宅、商業、工業、公益事業に区分されます。商業部門は2024年の市場シェアの49.3%を占め、企業におけるエネルギー効率の高いソリューションに対する需要の高まりを反映しています。運用コストの上昇と規制要件の厳格化により、商業施設はコスト削減、エネルギー最適化、持続可能性義務への準拠を確実にするEaaSモデルの採用を余儀なくされています。これらのサービスはまた、商業施設の特定のニーズに合わせた拡張可能なエネルギー・ソリューションを提供し、効率を高めて経費を削減します。

戦略的パートナーシップは、この市場で事業を展開する企業にとって重要な成長戦略として浮上しており、事業領域の拡大と革新的なサービスの開発に役立っています。米国市場の2024年の評価額は336億米ドルで、北米が世界市場シェアの30.8%以上を占めています。この地域の優位性は、エネルギー・コストの上昇とエネルギー・インフラの近代化の必要性に後押しされ、2034年までにさらに拡大すると予想されます。電力網の老朽化は効率低下と停電リスクの増大につながり、企業は設備投資を抑え、信頼性を高めるEaaSソリューションへの投資を促しています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- 1次調査と検証

- 市場の定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションとテクノロジーの展望

第5章 市場規模・予測:タイプ別、2021年~2034年

- 主要動向

- エネルギー供給サービス

- 運用・保守サービス

- エネルギー効率化・最適化サービス

第6章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 商業

- 産業

- ユーティリティ

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- 英国

- フランス

- デンマーク

- アジア太平洋

- 中国

- 韓国

- インド

- 日本

- 世界のその他の地域

第8章 企業プロファイル

- Alpiq

- Ameresco

- Bernhard Energy Solutions

- Capstone Green Energy Corporation

- Centrica

- Contemporary Energy Solutions

- Edison Energy

- Enel X

- EDF Energy

- Honeywell International

- IonicBlue

- Schneider Electric

- Siemens

- WGL Energy

目次

The Global Energy As A Service (EaaS) Market reached a valuation of USD 126 billion in 2024 and is projected to grow at a CAGR of 8.7% from 2025 to 2034. This growth is driven by the increasing shift toward sustainability, reinforced by supportive government incentives and surging energy demand across industries. Businesses and institutions are actively seeking cost-effective, resilient, and decentralized energy solutions to optimize consumption and enhance efficiency. Subscription-based energy service models are gaining traction as they provide long-term cost savings and operational advantages. Market dynamics are further influenced by the rising emphasis on energy efficiency, grid modernization, and digital transformation in the sector. The growing integration of advanced technologies, such as IoT sensors, predictive maintenance tools, and real-time analytics, is improving energy management, making EaaS solutions more viable for businesses. Governments worldwide are also implementing stringent energy regulations and funding programs to promote sustainable energy initiatives, further driving adoption. With an increasing focus on reducing carbon footprints and improving energy resilience, the demand for flexible and scalable EaaS models is rising, setting the stage for sustained market expansion over the next decade.

The industry is categorized into energy supply services, operational and maintenance services, and energy efficiency and optimization services. Operational and maintenance services play a crucial role in ensuring the reliability and performance of energy systems. These services are projected to generate USD 132.5 billion by 2034 as businesses prioritize solutions that enhance efficiency and sustainability. By providing continuous energy supply, optimized operations, and minimized downtime, these services help organizations achieve better energy management while maintaining cost-effectiveness. The rising need for seamless infrastructure maintenance and operational support is driving widespread adoption, allowing businesses to reduce risks and improve long-term energy performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $126 Billion |

| Forecast Value | $291.6 Billion |

| CAGR | 8.7% |

In terms of end use, the market is segmented into residential, commercial, industrial, and utility sectors. The commercial sector accounted for 49.3% of the market share in 2024, reflecting the growing demand for energy-efficient solutions among businesses. Rising operational expenses and stricter regulatory requirements are compelling commercial establishments to adopt EaaS models that ensure cost savings, energy optimization, and compliance with sustainability mandates. These services also offer scalable energy solutions tailored to the specific needs of commercial facilities, boosting efficiency and lowering expenses.

Strategic partnerships are emerging as a key growth strategy for companies operating in this market, helping them expand their reach and develop innovative service offerings. The U.S. market held a valuation of USD 33.6 billion in 2024, with North America accounting for more than 30.8% of the global market share. This regional dominance is expected to grow further by 2034, fueled by increasing energy costs and the need for modernized energy infrastructure. Aging power grids are leading to efficiency declines and higher risks of outages, prompting businesses to invest in EaaS solutions that offer lower capital investment and greater reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Energy supply service

- 5.3 Operational and Maintenance services

- 5.4 Energy Efficiency and Optimization services

Chapter 6 Market Size and Forecast, By End Use, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

- 6.5 Utility

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 UK

- 7.3.4 France

- 7.3.5 Denmark

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 South Korea

- 7.4.3 India

- 7.4.4 Japan

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Alpiq

- 8.2 Ameresco

- 8.3 Bernhard Energy Solutions

- 8.4 Capstone Green Energy Corporation

- 8.5 Centrica

- 8.6 Contemporary Energy Solutions

- 8.7 Edison Energy

- 8.8 Enel X

- 8.9 EDF Energy

- 8.10 Honeywell International

- 8.11 IonicBlue

- 8.12 Schneider Electric

- 8.13 Siemens

- 8.14 WGL Energy

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日