|

市場調査レポート

商品コード

1699260

ウェアラブル心臓機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Wearable Cardiac Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| ウェアラブル心臓機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

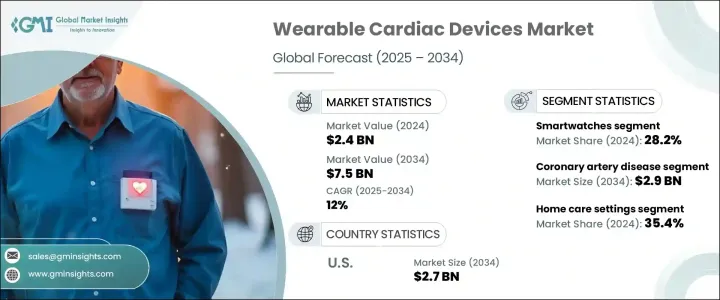

世界のウェアラブル心臓機器市場は、2024年に24億米ドルと評価され、2025年から2034年にかけてCAGR 12%で拡大すると予想されています。

これらの携帯型医療機器は、個人が心臓の健康を毎日モニターし、心拍数、リズム、身体活動、睡眠パターンに基づく長期的データを収集・分析することを可能にします。遠隔モニタリングを可能にすることで、頻繁な臨床受診を不要にし、患者の利便性と医療効率を向上させる。高度なセンサーとAIを活用した分析機能を備えたこれらのデバイスは、リアルタイムの洞察を提供し、ヘルスケア専門家が十分な情報に基づいた意思決定を行えるよう支援します。予防ヘルスケアに対する意識の高まり、心血管疾患の患者数の増加、患者の遠隔モニタリングに対する需要の高まりが、市場成長の原動力となっています。ウェアラブル心臓機器は、不整脈モニタリングや心不全や末梢動脈疾患などの状態管理に広く使用されています。

市場は製品別にスマートウォッチ、ホルターモニター、パッチ、パルスオキシメーター、除細動器、その他のウェアラブルデバイスに区分されます。スマートウォッチはセグメントをリードし、2024年には総売上の28.2%を占める。そのユーザーフレンドリーなデザインは、専門家の支援なしにシームレスな心臓の健康追跡を可能にし、幅広い人々がアクセスできるようにします。AIを搭載したアルゴリズムは、不規則な心臓リズムを検出し、リアルタイムの健康洞察を提供するのに役立ちます。これらの時計はECG、心拍数、酸素レベルなど様々なバイタルをモニターするため、心臓血管の健康状態を包括的に把握することができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 75億米ドル |

| CAGR | 12% |

用途別では、冠動脈疾患、心筋症、心筋梗塞後、先天性心疾患、手術後の心臓ケア、その他の関連疾患に分けられます。冠動脈疾患分野は2024年に37.4%の市場シェアを占め、2034年には29億米ドルに達すると予測されています。運動不足、肥満、喫煙などのライフスタイルに関連する危険因子の急増が、このセグメントにおけるウェアラブル心臓機器の需要を促進しています。冠動脈疾患患者の増加に伴い、ヘルスケアプロバイダーは早期発見と疾患管理のためにウェアラブル技術への依存度を高めています。

市場はさらに、最終用途別に病院、専門センター、在宅ケア環境、その他の施設に分類されます。快適な環境での継続的な心臓モニタリングに対する嗜好の高まりを反映して、2024年の在宅ケア環境のシェアは35.4%でした。これらのデバイスは、個人が自宅で心血管系の健康状態を追跡することを可能にし、ヘルスケア施設への依存を軽減します。規制遵守は、ポイントオブケア設定におけるウェアラブルデバイスの有効性を保証し、このセグメントの採用をさらに促進します。

地域別では、米国のウェアラブル心臓機器市場は、心血管疾患の高い有病率と発達したヘルスケアシステムに後押しされて、2034年までに27億米ドルに達すると予測されています。消費者の意識の高まりとウェアラブル健康機器の技術的進歩が、市場の成長をさらに強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患を患う患者の増加

- ウェアラブル心臓機器の急速な技術進歩

- 低侵襲デバイスへの嗜好の高まり

- 健康意識の高まりと予防医療

- 業界の潜在的リスク&課題

- データ・プライバシーの問題

- 厳しい規制政策

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ホルターモニター

- スマートウォッチ

- パッチ

- 除細動器

- パルスオキシメーター

- その他の製品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 冠動脈疾患(CAD)

- 心筋症

- 心筋梗塞後

- 先天性心疾患

- 心臓手術後のケア

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門センター

- 在宅医療

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Boston Scientific

- Cardiac Insight

- CardiacSense

- Cardiac Rhythm

- iRhythm Technologies

- Integra LifeSciences

- Koninklijke Philips

- Medtronic

- Proteus Digital Health

- Qardio

- ZOLL Medical Corporation

- Welch Allyn

- VitalConnect

- Zimmer Biomet

The Global Wearable Cardiac Devices Market was valued at USD 2.4 billion in 2024 and is expected to expand at a CAGR of 12% from 2025 to 2034. These portable medical devices allow individuals to monitor their heart health daily, collecting and analyzing long-term data based on heart rate, rhythm, physical activity, and sleep patterns. By enabling remote monitoring, they eliminate the need for frequent clinical visits, improving patient convenience and medical efficiency. Equipped with advanced sensors and AI-powered analytics, these devices provide real-time insights, helping healthcare professionals make informed decisions. Growing awareness about preventive healthcare, rising cases of cardiovascular diseases, and increasing demand for remote patient monitoring are driving market growth. Wearable cardiac devices are widely used for cardiac arrhythmia monitoring and managing conditions such as heart failure and peripheral artery disease.

The market is segmented by product into smartwatches, Holter monitors, patches, pulse oximeters, defibrillators, and other wearable devices. Smartwatches led the segment, capturing 28.2% of total revenue in 2024. Their user-friendly design allows seamless heart health tracking without professional assistance, making them accessible to a broad audience. AI-powered algorithms help detect irregular heart rhythms and provide real-time health insights. As these watches monitor various vitals, including ECG, heart rate, and oxygen levels, they offer a comprehensive view of cardiovascular health.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 12% |

By application, the market is divided into coronary artery disease, cardiomyopathies, post-myocardial infarction, congenital heart diseases, post-surgical cardiac care, and other related conditions. The coronary artery disease segment held a 37.4% market share in 2024 and is projected to reach USD 2.9 billion by 2034. A surge in lifestyle-related risk factors such as physical inactivity, obesity, and smoking is fueling the demand for wearable cardiac devices in this segment. With rising cases of coronary artery disease, healthcare providers are increasingly relying on wearable technology for early detection and disease management.

The market is further categorized by end use into hospitals, specialty centers, home care settings, and other facilities. Home care settings accounted for a 35.4% share in 2024, reflecting a growing preference for continuous heart monitoring in comfortable environments. These devices enable individuals to track their cardiovascular health at home, reducing dependency on healthcare facilities. Regulatory compliance ensures the effectiveness of wearable devices in point-of-care settings, further driving adoption in this segment.

Regionally, the U.S. wearable cardiac devices market is anticipated to reach USD 2.7 billion by 2034, fueled by a high prevalence of cardiovascular diseases and a well-developed healthcare system. Increasing consumer awareness and technological advancements in wearable health devices are further strengthening market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

- 3.2.1.2 Rapid technological advancements in wearable cardiac devices

- 3.2.1.3 Growing preference of minimally invasive devices

- 3.2.1.4 Rising health consciousness and preventive care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy issues

- 3.2.2.2 Stringent regulatory policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Holter monitors

- 5.3 Smartwatches

- 5.4 Patch

- 5.5 Defibrillators

- 5.6 Pulse oximeters

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease (CAD)

- 6.3 Cardiomyopathies

- 6.4 Post-myocardial infarction

- 6.5 Congenital heart diseases

- 6.6 Post-surgical cardiac care

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty centers

- 7.4 Home care settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Boston Scientific

- 9.3 Cardiac Insight

- 9.4 CardiacSense

- 9.5 Cardiac Rhythm

- 9.6 iRhythm Technologies

- 9.7 Integra LifeSciences

- 9.8 Koninklijke Philips

- 9.9 Medtronic

- 9.10 Proteus Digital Health

- 9.11 Qardio

- 9.12 ZOLL Medical Corporation

- 9.13 Welch Allyn

- 9.14 VitalConnect

- 9.15 Zimmer Biomet