|

市場調査レポート

商品コード

1699294

心血管デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cardiovascular Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 心血管デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月19日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

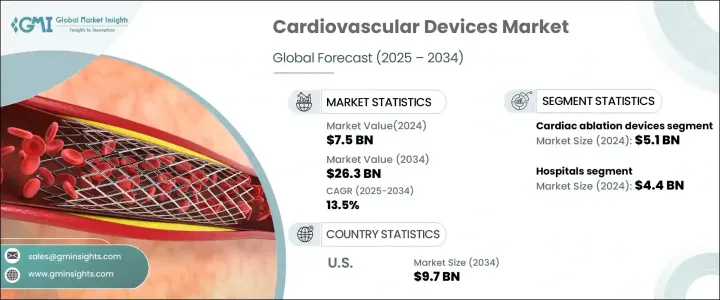

世界の心血管デバイス市場は、2024年に75億米ドルと評価され、心血管疾患(CVDs)の症例の増加、技術の進歩、ヘルスケア支出の増加を背景に、2025年から2034年にかけて13.5%のCAGRを記録すると予測されています。

人口の高齢化と生活習慣病が主な原因となって、心臓関連の疾病の負担が増大していることが、先進的な心血管ソリューションの需要を大きく押し上げています。座りっぱなしの習慣、食生活の乱れ、高ストレスレベルが世界的にCVDの一因であり続ける中、革新的な診断・治療機器の必要性はこれまで以上に高まっています。加えて、予防ヘルスケアや早期発見戦略に対する意識の高まりが、市場導入をさらに後押ししています。

医療技術における最先端の進歩は、心血管治療に革命をもたらしています。AIを活用した診断、ロボット支援手術、低侵襲手術の導入は、回復時間を短縮しながら患者の予後を向上させています。業界では規制当局の承認が急増しており、最先端の心血管デバイスへのアクセスが拡大しています。政府や民間のヘルスケア機関は、進化する患者のニーズに応える次世代ソリューションを導入するため、研究開発に多額の投資を行っています。特に新興経済諸国における医療費の増加は、最先端の心臓機器の普及を促進し、市場開拓をさらに後押ししています。さらに、外来での心血管介入や在宅モニタリングシステムの増加により、患者にとって治療がより身近で便利になりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 75億米ドル |

| 予測金額 | 263億米ドル |

| CAGR | 13.5% |

同市場は、機器タイプ別に心臓アブレーション機器、左心房付属器閉鎖機器、内視鏡的血管採取機器に分類されます。このうち、心臓アブレーションデバイスは2024年に51億米ドルの評価額で市場をリードし、予測期間中のCAGRは13.7%と予測されています。心房細動の有病率の上昇は、これらの機器の需要を支える主要なドライバーです。不規則な心拍リズムと診断される患者の増加に伴い、低侵襲アブレーション技術の採用が増加しています。さらに、アブレーション技術の継続的な進歩と相まって、効果的な治療オプションに対する意識の高まりが市場拡大を促進しています。

エンドユース別では、心血管デバイス市場は病院、外来手術センター、心臓センター、その他のヘルスケア施設に区分されます。病院がこの分野を支配し、2024年には44億米ドルを生み出し、総売上の58.3%を占めています。バイパス手術、カテーテル治療、機器移植などの複雑な心臓治療に対する患者の流入が増加しており、この分野での病院のリーダーシップは確固たるものとなっています。高度な画像処理技術、心臓専門ユニット、集学的チームを備えた病院は、重要な心臓血管症例の主要治療拠点であり続けています。さらに、緊急処置や入院処置に対応できることから、患者とヘルスケア提供者の両方から好まれています。

米国の心血管デバイス市場は、2023年には25億米ドルで、2034年には97億米ドルに成長すると予測されています。同国は、確立されたヘルスケア・インフラ、最先端の心血管技術の急速な導入、心臓外科医、インターベンショナル・カーディオロジスト、電気生理学者を含む熟練した専門家の強力なネットワークなどのメリットを享受しています。治療手法の絶え間ない革新と支持的な規制政策が市場浸透を加速しています。好意的な償還制度の枠組みが先進的な心臓血管機器の採用をさらに後押しし、米国は心臓ケアソリューションの主要市場として位置づけられています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患を患う患者の増加

- 高齢人口の拡大

- 政府のイニシアチブの高まり

- 心血管デバイスの技術的進歩

- 低侵襲手技に対する需要の高まり

- 業界の潜在的リスク&課題

- 心臓手術に伴う高いリスク

- 厳しい規制シナリオ

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:デバイスタイプ別、2021年~2034年

- 主要動向

- 心臓アブレーションデバイス

- 高周波アブレーター

- 電気アブレーター

- 冷凍アブレーションデバイス

- 超音波デバイス

- その他の心臓アブレーションデバイス

- 左心房付属器閉鎖装置

- 心内膜型LAA閉鎖装置

- 心外膜LAA閉鎖装置

- 内視鏡下血管採取デバイス

- EVHシステム

- 内視鏡

- 付属品

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 心臓センター

- その他の最終用途

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Abbott Laboratories

- AngioDynamics

- AtriCure

- Biosense Webster

- Boston Scientific Corporation

- Biotronik

- CardioFocus

- Getinge

- Japan Lifeline

- Karl Storz

- Lepu Medical Technology

- Lifetech Scientific

- Livanova

- Microport Scientific Corporation

- Medical Instruments

- Medtronic

- Occlutech

- Saphena Medical

- Stereotaxis

- Terumo Corporation

The Global Cardiovascular Devices Market was valued at USD 7.5 billion in 2024 and is projected to register a CAGR of 13.5% from 2025 to 2034, driven by rising cases of cardiovascular diseases (CVDs), technological advancements, and increasing healthcare expenditures. The escalating burden of heart-related ailments, largely fueled by an aging population and lifestyle-related disorders, is significantly propelling demand for advanced cardiovascular solutions. As sedentary habits, poor dietary choices, and high-stress levels continue to contribute to CVDs worldwide, the need for innovative diagnostic and treatment devices is becoming more pressing than ever. Additionally, greater awareness regarding preventive healthcare and early detection strategies is further boosting market adoption.

Cutting-edge advancements in medical technology are revolutionizing cardiovascular care. The introduction of AI-powered diagnostics, robotic-assisted surgeries, and minimally invasive procedures is enhancing patient outcomes while reducing recovery time. The industry is witnessing a surge in regulatory approvals, expanding access to state-of-the-art cardiovascular devices. Governments and private healthcare entities are heavily investing in research and development to introduce next-generation solutions that cater to evolving patient needs. Rising healthcare expenditures, particularly in developed economies, are facilitating the widespread availability of advanced cardiac devices, further propelling market growth. Moreover, the increasing number of outpatient cardiovascular interventions and home-based monitoring systems is making treatments more accessible and convenient for patients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $26.3 Billion |

| CAGR | 13.5% |

The market is categorized by device type into cardiac ablation devices, left atrial appendage closure devices, and endoscopic vessel harvesting devices. Among these, cardiac ablation devices led the market with a valuation of USD 5.1 billion in 2024 and are projected to witness a CAGR of 13.7% over the forecast period. The rising prevalence of atrial fibrillation is a key driver behind the demand for these devices. With more individuals diagnosed with irregular heart rhythms, the adoption of minimally invasive ablation techniques is on the rise. Additionally, growing awareness about effective treatment options, coupled with continuous advancements in ablation technology, is fostering market expansion.

By end use, the cardiovascular devices market is segmented into hospitals, ambulatory surgical centers, cardiac centers, and other healthcare facilities. Hospitals dominated the sector, generating USD 4.4 billion in 2024 and accounting for 58.3% of the total revenue. A higher patient influx for complex cardiac interventions, including bypass surgeries, catheterizations, and device implantations, is solidifying hospitals' leadership in this space. Equipped with advanced imaging technologies, specialized cardiac units, and multidisciplinary teams, hospitals remain the primary treatment hubs for critical cardiovascular cases. Additionally, their ability to handle emergency and inpatient procedures makes them a preferred choice among both patients and healthcare providers.

The U.S. cardiovascular devices market stood at USD 2.5 billion in 2023 and is projected to grow to USD 9.7 billion by 2034. The country benefits from a well-established healthcare infrastructure, rapid adoption of cutting-edge cardiovascular technologies, and a strong network of skilled professionals, including cardiac surgeons, interventional cardiologists, and electrophysiologists. Continuous innovation in treatment methodologies and supportive regulatory policies are accelerating market penetration. Favorable reimbursement frameworks are further encouraging the adoption of advanced cardiovascular devices, positioning the U.S. as a leading market for cardiac care solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

- 3.2.1.2 Expanding geriatric population

- 3.2.1.3 Rising government initiatives

- 3.2.1.4 Technological advancements in cardiovascular devices

- 3.2.1.5 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk associated with cardiac procedures

- 3.2.2.2 Stringent regulatory scenario

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiac ablation devices

- 5.2.1 Radiofrequency ablators

- 5.2.2 Electric ablators

- 5.2.3 Cryoablation devices

- 5.2.4 Ultrasound devices

- 5.2.5 Other cardiac ablation devices

- 5.3 Left atrial appendage closure devices

- 5.3.1 Endocardial LAA closure devices

- 5.3.2 Epicardial LAA closure devices

- 5.4 Endoscopic vessel harvesting devices

- 5.4.1 EVH systems

- 5.4.2 Endoscopes

- 5.4.3 Accessories

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Cardiac centers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 AngioDynamics

- 8.3 AtriCure

- 8.4 Biosense Webster

- 8.5 Boston Scientific Corporation

- 8.6 Biotronik

- 8.7 CardioFocus

- 8.8 Getinge

- 8.9 Japan Lifeline

- 8.10 Karl Storz

- 8.11 Lepu Medical Technology

- 8.12 Lifetech Scientific

- 8.13 Livanova

- 8.14 Microport Scientific Corporation

- 8.15 Medical Instruments

- 8.16 Medtronic

- 8.17 Occlutech

- 8.18 Saphena Medical

- 8.19 Stereotaxis

- 8.20 Terumo Corporation