|

市場調査レポート

商品コード

1822602

自己血糖モニタリングデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Self-Monitoring Blood Glucose Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自己血糖モニタリングデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月28日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

概要

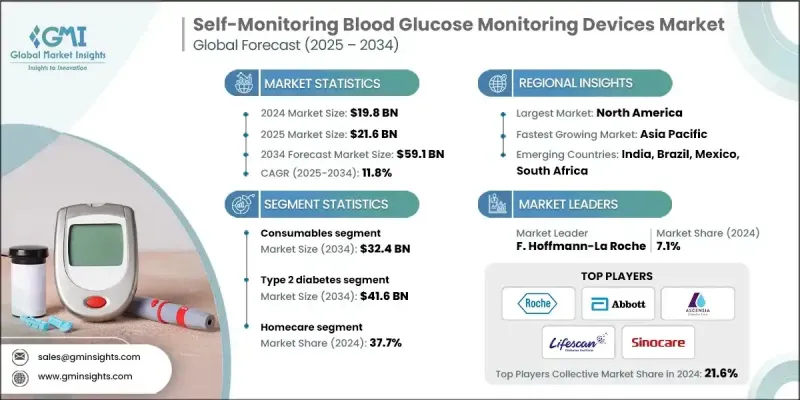

Global Market Insights Inc.が発行した最新レポートによると、世界の自己血糖モニタリングデバイス市場は2024年に198億米ドルと推定され、CAGR 11.8%で2025年の216億米ドルから2034年には591億米ドルに成長すると予測されています。

特に新興市場における1型および2型糖尿病患者の世界的な急増は、毎日のグルコース追跡のための便利で信頼性の高いSMBGデバイスの需要を促進しています。座りがちなライフスタイル、不健康な食生活、肥満率の上昇が糖尿病罹患率の上昇に寄与しているため、若年層や幅広い層で糖尿病と診断される人が増えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 198億米ドル |

| 予測金額 | 591億米ドル |

| CAGR | 11.8% |

消耗品需要の高まり

消耗品セグメントは2024年に顕著なシェアを占め、検査ストリップ、ランセット、コントロールソリューションが牽引しました。これらの品目は日々のモニタリングに不可欠であるため、その需要は常に高く、市場の着実な成長を牽引しています。検査ストリップは交換サイクルが頻繁であるため、消耗品売上高の大半を占めています。消費者がより正確で便利な検査を求める中、各社はより少量の血液サンプルで迅速な結果が得られるストリップを製造するよう技術革新を進めています。消耗品セグメントの拡大は患者のアドヒアランス維持に不可欠であり、長期的な顧客ロイヤリティの確保を目指す業界各社から引き続き多額の投資を集めています。

2型糖尿病の有病率の上昇

2型糖尿病セグメントは、生活習慣に関連する糖尿病患者の世界的な増加を反映して、2024年に大きな収益を上げました。2型糖尿病患者は、食事療法や薬物療法と並行して、病状を効果的に管理するために定期的なグルコースモニタリングを必要とすることが多いです。この分野は、疾病管理に対する意識が向上し、ヘルスケアプロバイダーが合併症予防における血糖コントロールの重要性を強調するにつれて急成長しています。2型糖尿病患者にとって、SMBG機器は手頃な価格で使いやすいため、なくてはならないツールとなっています。

ホームケアが牽引役に

在宅ケア分野は、患者中心の遠隔ヘルスケア管理の動向に牽引され、2024年に大きなシェアを占めました。利便性、プライバシー、遠隔医療サービスの継続的な拡大が動機となって、自宅で快適に血糖値をモニタリングすることを好む個人が増加しています。このセグメントは、ヘルスケア専門家とのリアルタイムのデータ共有を可能にするスマートフォン対応デバイスやデジタルヘルスプラットフォームなどの技術的進歩の恩恵を受けています。在宅医療の採用はまた、臨床の場以外での慢性疾患管理をますます重視するようにもなっています。

地域別の洞察

北米が有望な地域として台頭

北米自己血糖モニタリングデバイス市場は2024年に注目すべきシェアを獲得しました。強力なヘルスケアインフラ、糖尿病罹患率の高さ、保険適用範囲の広さが、こうした機器の旺盛な需要に寄与しています。この地域の消費者は、正確性、利便性、デジタルヘルスエコシステムとの統合を優先しており、これがメーカーの急速な技術革新を後押ししています。さらに、業界大手の存在と確立された規制環境が、高品質な標準と製品の信頼性を保証しています。

自己血糖モニタリングデバイス市場の主要企業は、All Medicus、DarioHealth、B. Braun Melsungen、Ypsomed Holding、Sanofi、Bionime Corporation、AgaMatrix、Nova Biomedical、LifeScan、Arkray、Omnis Health、Sinocare、Abbott Laboratories、F. Hoffmann-La Roche、Ascensia Diabetes Care Holdingsです。

市場の足場を固めるため、自己血糖モニタリングデバイス市場の各社はイノベーション、パートナーシップ、患者エンゲージメントに重点を置いています。製品開発は精度、使いやすさ、接続性を重視しており、多くのメーカーがより広範なデジタルヘルスプラットフォームと統合するアプリ対応メーターを発売しています。ヘルスケアプロバイダーや保険会社との戦略的提携は、償還スキームやバンドルケアプログラムを通じてデバイスの利用可能性を拡大しています。各社はまた、特に新興市場において、患者のリテラシーとアドヒアランスを向上させるための教育イニシアチブに投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 世界中で糖尿病の有病率が上昇

- 国民の意識を高めるための政府の取り組み

- 先進国における自己血糖モニタリングデバイスの技術進歩

- 業界の潜在的リスク&課題

- 新興諸国における高度な機器や付属品の高コスト

- 厳格な規制要件

- 市場機会

- 新興市場への拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーンと流通分析

- 払い戻しシナリオ

- 価格分析、2024

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 自己血糖測定器

- 消耗品

- 検査ストリップ

- ランセット

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 1型糖尿病

- 2型糖尿病

- 妊娠糖尿病

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- 診断センター

- ホームケア

- その他の用途

第8章 市場推計・予測:国別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- オランダ

- スウェーデン

- ベルギー

- デンマーク

- フィンランド

- ノルウェー

- リトアニア

- ラトビア

- エストニア

- ロシア

- ポーランド

- スイス

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- 台湾

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- チリ

- ペルー

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- エジプト

- イスラエル

- クウェート

- カタール

第9章 企業プロファイル

- Abbott Laboratories

- AgaMatrix

- All Medicus

- Arkray

- Ascensia Diabetes Care Holdings

- B. Braun Melsungen

- Bionime Corporation

- DarioHealth

- F. Hoffmann-La Roche

- LifeScan

- Nova Biomedical

- Omnis Health

- Sanofi

- Sinocare

- Ypsomed Holding