|

市場調査レポート

商品コード

1698583

Cアーム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測C-arm Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| Cアーム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月13日

発行: Global Market Insights Inc.

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

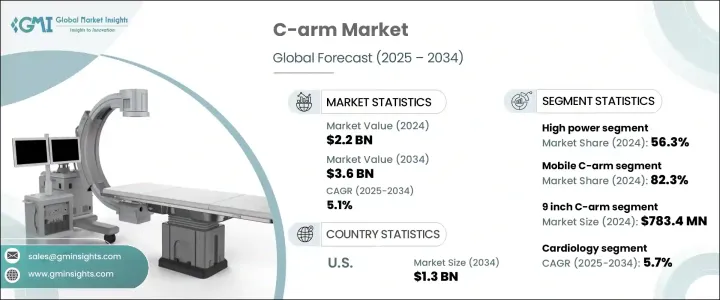

Cアームの世界市場は、2024年に22億米ドルと評価され、2025年から2034年にかけて5.1%のCAGRで成長すると予測されています。

Cアームは、移動式と固定式の両方があり、医療処置のためにリアルタイムのX線画像を提供するように設計された高度なイメージング装置です。これらの装置は、整形外科、心臓病学、腫瘍学など様々な専門分野の手術、診断、インターベンショナル・ラジオロジーにおいて重要な役割を果たしています。高齢化、座りっぱなしの生活、食生活の乱れなどに起因する慢性疾患の増加により、高度な画像ソリューションに対する需要が高まっています。

慢性疾患が蔓延するにつれ、診断、治療、外科的介入における高解像度画像の必要性は拡大し続けています。Cアームシステムは、血管形成術、整形外科手術、腫瘍摘出術などの複雑な手技を、鮮明でリアルタイムの画像を提供することで容易にし、手術の精度と患者の転帰を向上させる。画像品質、使いやすさ、携帯性の向上は、市場拡大にさらに貢献しています。病院や手術センターでは、診断精度と治療効率を高めるため、これらの機器を統合するケースが増えており、市場の着実な成長軌道を後押ししています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 36億米ドル |

| CAGR | 5.1% |

製品タイプ別では、モバイルCアームが2024年の世界市場で82.3%のシェアを占めました。可搬性に優れているため、病院のさまざまな部門をシームレスに移動でき、スペースに制約がある施設や複数の手技が異なる場所で行われる施設に最適です。画像品質の向上、操作性の改善、ユーザーフレンドリーな設計が普及に寄与しています。また、これらのシステムは、外傷症例、整形外科手術、透視処置など、さまざまな用途にリアルタイムで画像を提供するため、需要を押し上げ、市場の優位性を確固たるものにしています。

発電機の出力に基づいて、市場は高出力セグメントと低出力セグメントに分類されます。2024年に56.3%のシェアを獲得した高出力Cアームは、正確な診断と治療に不可欠な高解像度画像を提供できることから、外科、整形外科、外傷の用途で好まれています。これらのシステムは、高密度組織や複雑な解剖学的構造を画像化する際に特に有用であり、複雑な医療処置の際の正確さを保証します。慢性疾患の患者数の増加、世界の高齢化、低侵襲手術の進歩は、高出力Cアーム装置の需要を促進し続けています。放射線被曝を最小限に抑えながらリアルタイム撮影が可能なCアームは、現代のヘルスケア現場で好まれています。

同市場はイメージインテンシファイアのタイプ別にも細分化されており、2024年には9インチCアームカテゴリーが7億8,340万米ドルでトップとなります。これらのシステムは、可搬性と画像解像度の最適なバランスを提供し、手術室や外来センターでの処置に非常に適しています。整形外科手術、血管インターベンション、疼痛管理などのアプリケーションをサポートする汎用性が、普及を後押ししています。

さまざまな医療用途の中で、心臓病学は2034年まで5.7%のCAGRで最も急速に成長すると予測されています。心血管疾患の有病率の増加が、複雑な介入を容易にする高度な画像システムの必要性を煽っています。リアルタイムイメージングは、血管造影やステント留置のような手技に不可欠であり、この分野におけるCアームsの需要拡大を牽引しています。低侵襲な心臓病治療への世界のシフトが市場拡大をさらに加速させています。

最終用途別では、病院が2024年の売上高12億米ドルで市場を独占しています。幅広い診断や外科手術の主要ヘルスケアプロバイダーである病院は、Cアームシステムの主要な消費者です。高い予算と先進医療技術へのアクセスにより、これらの画像処理装置の迅速な導入と統合が可能になっています。特に救急部や重症治療室での患者数の増加が引き続き需要を牽引しており、病院は市場の主要セグメントとなっています。

米国のCアーム市場は、整形外科、心臓病学、神経学分野での低侵襲手術の需要増に牽引され、2034年までに13億米ドルに達する見込みです。リアルタイムイメージング技術の広範な採用は、外科手術の精度を高め、ヘルスケア施設全体で患者の転帰を改善する上で重要な役割を果たしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 手術件数の増加

- 慢性疾患の増加

- Cアーム装置の技術的進歩

- 低侵襲手術に対する需要の高まり

- 業界の潜在的リスク&課題

- Cアーム機器に関連する高コスト

- 熟練したヘルスケア専門家の不足

- 促進要因

- 成長可能性分析

- 規制状況

- 技術動向

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 固定式Cアーム

- モバイルCアーム

第6章 市場推計・予測:発電機電力別、2021年~2034年

- 主要動向

- 高電力

- 低電力

第7章 市場推計・予測:イメージインテンシファイアタイプ別、2021年~2034年

- 主要動向

- 9インチCアーム

- 12インチCアーム

- 4/6インチCアーム

- その他のイメージインテンシファイアタイプ

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 整形外科および外傷

- 循環器

- 神経

- 消化器

- 腫瘍

- 歯科

- その他の用途

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 診断センター

- その他の最終用途

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Canon

- Fujifilm

- GE Healthcare

- Genoray

- Hologic

- Philips

- Perlove Medical

- Shimadzu Corporation

- Siemens Healthineers

- StrenMed

- Trivitron Healthcare

- Turner Imaging Systems

- UMG/DEL Medical

- Villa Sistemi Medicali

- Ziehm Imaging

The Global C-Arm Market, valued at USD 2.2 billion in 2024, is set to grow at a CAGR of 5.1% from 2025 to 2034. A C-arm is an advanced imaging device, available in both mobile and fixed configurations, designed to deliver real-time X-ray imaging for medical procedures. These devices play a critical role in surgeries, diagnostics, and interventional radiology across various specialties, including orthopedics, cardiology, and oncology. The rising incidence of chronic diseases, fueled by aging populations, sedentary lifestyles, and poor dietary habits, is driving demand for advanced imaging solutions.

As chronic conditions become more prevalent, the need for high-resolution imaging in diagnosis, treatment, and surgical interventions continues to expand. C-arm systems facilitate complex procedures such as angioplasty, orthopedic surgeries, and tumor removals by providing clear, real-time visuals that enhance surgical precision and patient outcomes. Advances in imaging quality, ease of use, and portability further contribute to market expansion. Hospitals and surgical centers are increasingly integrating these devices to enhance diagnostic accuracy and treatment efficiency, reinforcing the market's steady growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 5.1% |

In terms of product type, mobile C-arms dominated the global market with an 82.3% share in 2024. Their portability enables seamless transport across various hospital departments, making them ideal for facilities where space is constrained and multiple procedures occur in different locations. Enhanced imaging quality, improved maneuverability, and user-friendly designs have contributed to their widespread adoption. These systems also provide real-time imaging for a variety of applications, such as trauma cases, orthopedic surgeries, and fluoroscopic procedures, boosting demand and solidifying their market dominance.

Based on generator power, the market is categorized into high-power and low-power segments. High-power C-arms, which captured a 56.3% share in 2024, are preferred in surgical, orthopedic, and trauma applications due to their ability to deliver high-resolution images critical for accurate diagnoses and treatments. These systems are particularly valuable in imaging dense tissues and complex anatomical structures, ensuring precision during intricate medical procedures. Growing cases of chronic diseases, an aging global population, and advancements in minimally invasive surgeries continue to propel demand for high-power C-arm devices. Their ability to deliver real-time imaging while minimizing radiation exposure makes them a preferred choice in modern healthcare settings.

The market is also segmented by image intensifier type, with the 9-inch C-arm category leading at USD 783.4 million in 2024. These systems offer an optimal balance between portability and imaging resolution, making them highly suitable for procedures in operating rooms and outpatient centers. Their versatility in supporting orthopedic surgeries, vascular interventions, and pain management applications further contributes to their widespread adoption.

Among various medical applications, cardiology is projected to grow at the fastest CAGR of 5.7% through 2034. The increasing prevalence of cardiovascular conditions is fueling the need for advanced imaging systems to facilitate complex interventions. Real-time imaging is essential in procedures like angiography and stent placement, driving the growing demand for C-arms in this segment. The global shift toward minimally invasive cardiology treatments is further accelerating market expansion.

By end use, hospitals dominated the market with USD 1.2 billion in revenue in 2024. As the primary healthcare providers for a vast range of diagnostic and surgical procedures, hospitals are major consumers of C-arm systems. Their higher budgets and access to advanced medical technologies enable faster adoption and integration of these imaging devices. Increasing patient volumes, particularly in emergency departments and critical care units, continue to drive demand, positioning hospitals as the leading segment in the market.

The U.S. C-arm market is on track to reach USD 1.3 billion by 2034, driven by the rising demand for minimally invasive procedures across orthopedic, cardiology, and neurology fields. The widespread adoption of real-time imaging technology is playing a crucial role in enhancing surgical precision and improving patient outcomes across healthcare facilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of surgical procedures

- 3.2.1.2 Rising prevalence of chronic diseases

- 3.2.1.3 Technological advancements of C-arm machines

- 3.2.1.4 Growing demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with C-arm machines

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fixed C-arm

- 5.3 Mobile C-arm

Chapter 6 Market Estimates and Forecast, By Generator Power, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 High power

- 6.3 Low power

Chapter 7 Market Estimates and Forecast, By Image Intensifier Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 9 inch C-arm

- 7.3 12 inch C-arm

- 7.4 4/6 inch C-arm

- 7.5 Other image intensifier types

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Orthopedics and trauma

- 8.3 Cardiology

- 8.4 Neurology

- 8.5 Gastroenterology

- 8.6 Oncology

- 8.7 Dental

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Diagnostic centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Canon

- 11.2 Fujifilm

- 11.3 GE Healthcare

- 11.4 Genoray

- 11.5 Hologic

- 11.6 Philips

- 11.7 Perlove Medical

- 11.8 Shimadzu Corporation

- 11.9 Siemens Healthineers

- 11.10 StrenMed

- 11.11 Trivitron Healthcare

- 11.12 Turner Imaging Systems

- 11.13 UMG/DEL Medical

- 11.14 Villa Sistemi Medicali

- 11.15 Ziehm Imaging