プロセスオーケストレーション市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Process Orchestration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698522

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

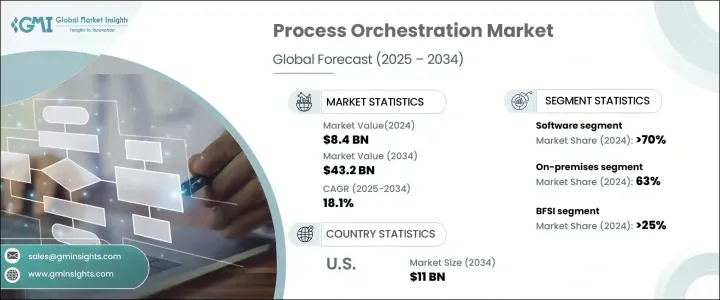

プロセスオーケストレーションの世界市場は、2024年に84億米ドルと評価され、業務効率を高め、手作業への依存を減らすための自動化需要の高まりにより、2025年から2034年にかけてCAGR 18.1%で拡大すると予測されています。

各業界の組織は、ワークフローを合理化し、生産性を向上させ、リアルタイムの意思決定を可能にするために、AI主導のオーケストレーション・ツールを優先しています。人工知能(AI)と機械学習(ML)を産業プロセスに統合することは、業務の自動化、コスト削減、ビジネスパフォーマンスの最適化に不可欠となっています。デジタルトランスフォーメーションへの取り組みが世界中で牽引力を増す中、企業は俊敏性、拡張性、競合を強化するためにプロセスオーケストレーションソリューションの採用を増やしています。

プロセスオーケストレーション・ソリューションの需要は、クラウド・コンピューティングの採用の増加、規制遵守の必要性の高まり、インテリジェントなプロセス自動化の推進など、いくつかの要因によって促進されています。企業は複雑な業務環境に対応するため、ワークフローを自動化し、異種システムを統合し、データ主導の洞察を提供できる高度なツールを求めています。企業はAIを活用したオーケストレーション・プラットフォームに投資することで、プロセスをリアルタイムで可視化し、予測分析とプロアクティブな意思決定を可能にしています。これらのソリューションは、効率を改善するだけでなく、シームレスでエラーのないオペレーションを保証することで、顧客体験も向上させる。デジタル・エコシステムが進化し続ける中、プロセスオーケストレーションを活用する企業は、新たな機会を活用し、長期的な成長を促進する上で有利な立場になると思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 84億米ドル |

| 予測金額 | 432億米ドル |

| CAGR | 18.1% |

市場の構成要素から見ると、プロセスオーケストレーション業界はソフトウェアとサービスに区分されます。2024年の市場シェアはソフトウェア部門が70%を占め、この勢いは今後も続くと予想されます。スケーラブルでカスタマイズ可能、かつコスト効率の高いソフトウェア・ソリューションは、ビジネス・オペレーションの最適化において極めて重要な役割を果たします。AIとMLの統合により、ソフトウェア・プラットフォームは予測的洞察を提供し、反復作業を自動化し、データ主導の意思決定を促進することができます。一方、サービス分野は、オーケストレーションツールの導入と管理について専門的なサポートを求める企業が増えていることから、2034年まで約18%のCAGRで成長すると予測されます。

同市場は業界別にも分類されており、主な分野はBFSI、ヘルスケア、小売・eコマース、IT、製造、エネルギー・公益事業、物流、公共部門などです。BFSI分野は、複雑な金融取引と規制要件を管理するための効率的で安全な自動化された業務の必要性によって、2024年の市場シェアが25%に達しました。金融機関は顧客体験の向上と業務効率の改善に努めており、プロセスオーケストレーション・ソリューションはリアルタイムのデータ処理、不正検知、リスク管理に不可欠となっています。

地域別では、北米が世界のプロセスオーケストレーション市場をリードし、2024年には26億米ドルの収益を生み出します。2034年までに、この地域市場は110億米ドルに達すると予測され、米国が支配的な役割を果たしています。同国は、強力な技術インフラと大手テクノロジー・プロバイダーが集中しているという利点があります。BFSI、ヘルスケア、小売などの業界は、オーケストレーション・ソリューション導入の最前線にあり、自動化を活用して業務の合理化と効率化を図っています。デジタルトランスフォーメーションを支援する政府の取り組みは、プロセスオーケストレーションツールの採用をさらに加速させ、同市場における同地域のリーダーシップを強化しています。イノベーションと製品開発への継続的な投資により、北米は世界のプロセスオーケストレーションの展望における主要な促進要因であり続けています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ソフトウェアプロバイダー

- サービスプロバイダー

- 流通業者

- エンドユース

- サプライヤーの状況

- 利益率分析

- 特許状況

- コスト内訳

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- ビジネスプロセスにおける自動化とAIの導入の増加

- リアルタイムの業務効率化とプロセスの最適化に対する需要の高まり

- 各業界におけるデジタルトランスフォーメーションへの取り組みの拡大

- より幅広いアクセスを可能にするローコード/ノーコード・プラットフォームの拡大

- 業界の潜在的リスク&課題

- 中小企業にとっての高い導入コスト

- プロセスオーケストレーションとレガシーシステムの統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソフトウェア

- サービス

- プロフェッショナルサービス

- マネージドサービス

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第7章 市場推計・予測:組織規模別、2021年~2032年

- 主要動向

- 中小企業(SME)

- 大企業

第8章 市場推計・予測:業界別、2021年~2032年

- 主要動向

- BFSI

- ヘルスケア

- 小売・eコマース

- ITセクター

- 製造業

- エネルギー・公益事業

- 物流

- 公共部門

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Appian

- BMC Software

- CA Technologies

- Camunda

- Celonis

- Cortex

- Dell Technologies

- Fujitsu

- HCL Technologies

- IBM

- Kyndryl

- Micro Focus

- Microsoft

- Newgen Software

- Oracle

- Pega

- SAP

- ServiceNow

- Software AG

- Wipro

目次

The Global Process Orchestration Market, valued at USD 8.4 billion in 2024, is projected to expand at a CAGR of 18.1% from 2025 to 2034, driven by the increasing demand for automation to enhance operational efficiency and reduce reliance on manual tasks. Organizations across industries are prioritizing AI-driven orchestration tools to streamline workflows, improve productivity, and enable real-time decision-making. The integration of artificial intelligence (AI) and machine learning (ML) into industrial processes has become essential for automating operations, reducing costs, and optimizing business performance. With digital transformation initiatives gaining traction worldwide, businesses are increasingly adopting process orchestration solutions to enhance agility, scalability, and competitiveness.

The demand for process orchestration solutions is fueled by several factors, including the rising adoption of cloud computing, the growing need for regulatory compliance, and the push for intelligent process automation. As organizations navigate complex operational landscapes, they seek advanced tools that can automate workflows, integrate disparate systems, and deliver data-driven insights. Companies are investing in AI-powered orchestration platforms to gain real-time visibility into processes, allowing for predictive analytics and proactive decision-making. These solutions not only improve efficiency but also enhance customer experience by ensuring seamless, error-free operations. As digital ecosystems continue to evolve, businesses that leverage process orchestration will be well-positioned to capitalize on emerging opportunities and drive long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $43.2 Billion |

| CAGR | 18.1% |

In terms of market components, the process orchestration industry is segmented into software and services. The software segment accounted for 70% of the market share in 2024, with strong momentum expected to continue in the coming years. Scalable, customizable, and cost-effective software solutions play a pivotal role in optimizing business operations. The integration of AI and ML enables software platforms to provide predictive insights, automate repetitive tasks, and facilitate data-driven decision-making. Meanwhile, the services segment is projected to grow at a CAGR of approximately 18% through 2034 as organizations increasingly seek specialized support for implementing and managing orchestration tools.

The market is also categorized by industry verticals, with key sectors including BFSI, healthcare, retail and e-commerce, IT, manufacturing, energy and utilities, logistics, and the public sector. The BFSI segment held a 25% market share in 2024, driven by the need for efficient, secure, and automated operations to manage complex financial transactions and regulatory requirements. As financial institutions strive to enhance customer experience and improve operational efficiency, process orchestration solutions are becoming essential for real-time data processing, fraud detection, and risk management.

Regionally, North America leads the global process orchestration market, generating USD 2.6 billion in revenue in 2024. By 2034, the regional market is projected to reach USD 11 billion, with the United States playing a dominant role. The country benefits from a strong technological infrastructure and a high concentration of leading technology providers. Industries such as BFSI, healthcare, and retail are at the forefront of adopting orchestration solutions, leveraging automation to streamline operations and improve efficiency. Government initiatives supporting digital transformation further accelerate the adoption of process orchestration tools, reinforcing the region's leadership in the market. With ongoing investments in innovation and product development, North America remains a key growth driver in the global process orchestration landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Software providers

- 3.1.2 Service providers

- 3.1.3 Distributors

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Patent landscape

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of automation and AI in business processes

- 3.9.1.2 Rising demand for real-time operational efficiency and process optimization

- 3.9.1.3 Growth in digital transformation initiatives across industries

- 3.9.1.4 Expansion of low-code/no-code platforms enabling broader accessibility

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation costs for small and medium-sized enterprises (SME)

- 3.9.2.2 Complexity in integrating process orchestration with legacy systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud-Based

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2032 ($Bn)

- 7.1 Key trends

- 7.2 Small and Medium-Sized Enterprises (SME)

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Industry Vertical, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Healthcare

- 8.4 Retail & e-Commerce

- 8.5 IT Sector

- 8.6 Manufacturing

- 8.7 Energy & utilities

- 8.8 Logistics

- 8.9 Public sector

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Appian

- 10.2 BMC Software

- 10.3 CA Technologies

- 10.4 Camunda

- 10.5 Celonis

- 10.6 Cortex

- 10.7 Dell Technologies

- 10.8 Fujitsu

- 10.9 HCL Technologies

- 10.10 IBM

- 10.11 Kyndryl

- 10.12 Micro Focus

- 10.13 Microsoft

- 10.14 Newgen Software

- 10.15 Oracle

- 10.16 Pega

- 10.17 SAP

- 10.18 ServiceNow

- 10.19 Software AG

- 10.20 Wipro

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日