|

|

市場調査レポート

商品コード

1698513

アナログ半導体市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Analog Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| アナログ半導体市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月05日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界のアナログ半導体市場は2024年に875億米ドルと評価され、2025年から2034年にかけてCAGR 7.4%で成長すると予測されています。

成長の原動力は、エネルギー効率の高いデバイスへのニーズの高まり、5GおよびIoTネットワークの急速な展開、自動車の電動化の採用拡大です。アナログ半導体は電力管理、信号処理、電圧調整に不可欠で、家電、通信、産業オートメーション、自動車システムなどの産業で重要な役割を果たしています。これらの分野での継続的な進歩に伴い、高性能でエネルギー効率の高いアナログ・ソリューションへの需要が高まっています。

業界全体がデジタルトランスフォーメーションへと急速にシフトしていることが、市場の成長をさらに後押ししています。企業は、効率を高め、消費電力を最小化し、性能を最適化するために、アナログ半導体をデバイスに統合する傾向を強めています。センサー技術、ワイヤレス接続、人工知能の革新は、高精度アナログチップの需要を押し上げています。さらに、持続可能性がメーカーの重要な焦点となるにつれ、エネルギー効率の高いアナログ・コンポーネントが再生可能エネルギー・システム、スマート・グリッド、電気自動車で脚光を浴びています。政府や企業は半導体の研究開発に多額の投資を行っており、今後10年間の市場見通しを強めています。産業オートメーションやヘルスケア機器における電化の動向も、ミッションクリティカルなアプリケーションにおけるアナログ半導体の採用を後押ししています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 875億米ドル |

| 予測金額 | 1,789億米ドル |

| CAGR | 7.4% |

アナログ半導体市場をタイプ別に分類すると、汎用部品と特定用途向け部品があります。汎用セグメントは大きな成長を遂げ、2034年には1,321億米ドルに達すると予測されています。この拡大には、複数の産業でコスト効率が高く汎用性の高いソリューションに対する需要が高まっていることが背景にあります。オペアンプ、電圧レギュレータ、コンパレータなどの汎用アナログ半導体は、信号増幅やコンディショニングなどの重要な機能を実行できるため、産業用アプリケーションで広く使用されています。これらの部品は電力管理やデータ変換に不可欠であり、様々な電子システムに不可欠なものとなっています。

フォームファクター別に分類すると、市場は集積回路(IC)とディスクリート部品で構成されます。2024年には、集積回路が市場シェアの73.4%を占め、小型化傾向の高まりがその原動力となっています。家電メーカーや自動車メーカーがより小型で効率的なデバイスを開発するにつれて、アナログICの需要は急増し続けています。パワーマネージメントICやセンサーICは、ウェアラブル機器やモバイル機器から高度な車載システムまで、幅広いアプリケーションに不可欠です。小型軽量設計の推進がアナログICの採用を加速し、市場の成長をさらに強めています。

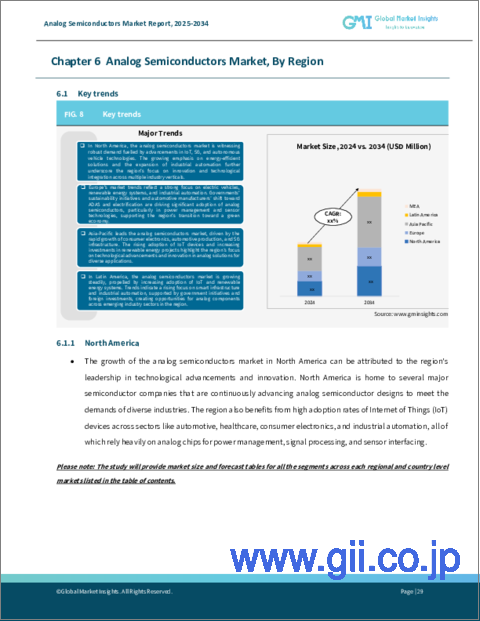

北米は依然としてアナログ半導体産業の主要プレーヤーであり、2034年には467億米ドルに達すると予想されています。米国がこの拡大をリードしており、同期間中に410億米ドルを生み出すと予測されています。自動車、通信、家電分野からの旺盛な需要が引き続きこの地域の成長を牽引しています。5G対応デバイス、人工知能、IoT技術の急速な統合は、研究開発、生産設備への投資を促進しています。大手半導体メーカーは、高性能アナログ部品の需要急増に対応するため、製造能力の拡大に注力しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- エネルギー効率の高い機器への需要の高まり

- IoTと5G技術の拡大

- 自動車産業における電動化の進展

- 再生可能エネルギー・アプリケーションの成長

- 業界の潜在的リスク&課題

- 世界半導体サプライチェーンの制約

- 激しい市場競争と代替案

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 汎用

- 特定用途向け

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- データコンバータ

- アンプ

- パワーマネージメントIC

- インターフェースIC

- センサー

- その他

第7章 市場推計・予測:フォームファクター別、2021年~2034年

- 主要動向

- 集積回路(IC)

- ディスクリート部品

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 航空宇宙・防衛

- 自動車

- 家電

- ヘルスケア

- 産業

- 通信

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Analog Devices

- Broadcom

- Diodes

- Infineon Technologies

- MediaTek

- Microchip Technology

- MinebeaMitsumi

- Murata Manufacturing

- NXP Semiconductors

- ON Semiconductor

- Qorvo

- Qualcomm Technologies

- Renesas Electronics

- Semtech

- Skyworks Solutions

- ST Microelectronics

- Taiwan Semiconductor Manufacturing

- Texas Instruments

- Toshiba

The Global Analog Semiconductors Market, valued at USD 87.5 billion in 2024, is expected to grow at a CAGR of 7.4% between 2025 and 2034. The growth is driven by the increasing need for energy-efficient devices, the rapid deployment of 5G and IoT networks, and the growing adoption of automotive electrification. Analog semiconductors are essential for power management, signal processing, and voltage regulation, playing a vital role in industries such as consumer electronics, telecommunications, industrial automation, and automotive systems. With continuous advancements in these sectors, demand for high-performance, energy-efficient analog solutions is on the rise.

The rapid shift toward digital transformation across industries is further fueling market growth. Companies are increasingly integrating analog semiconductors into devices to enhance efficiency, minimize power consumption, and optimize performance. Innovations in sensor technology, wireless connectivity, and artificial intelligence are pushing demand for high-precision analog chips. Additionally, as sustainability becomes a key focus for manufacturers, energy-efficient analog components are gaining prominence in renewable energy systems, smart grids, and electric vehicles. Governments and corporations are investing heavily in semiconductor R&D, strengthening the market outlook for the next decade. The ongoing trend of electrification in industrial automation and healthcare equipment is also driving the adoption of analog semiconductors in mission-critical applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $87.5 Billion |

| Forecast Value | $178.9 Billion |

| CAGR | 7.4% |

Segmented by type, the analog semiconductors market includes general-purpose and application-specific components. The general-purpose segment is projected to experience significant growth, reaching USD 132.1 billion by 2034. This expansion is fueled by the rising demand for cost-effective and versatile solutions across multiple industries. General-purpose analog semiconductors, such as operational amplifiers, voltage regulators, and comparators, are widely used in industrial applications due to their capability to perform essential functions like signal amplification and conditioning. These components are integral to power management and data conversion, making them indispensable in various electronic systems.

Classified by form factor, the market comprises integrated circuits (ICs) and discrete components. In 2024, integrated circuits accounted for 73.4% of the market share, driven by the growing trend toward miniaturization. As consumer electronics and automotive manufacturers develop smaller, more efficient devices, the demand for analog ICs continues to surge. Power management ICs and sensor ICs are essential in applications ranging from wearables and mobile devices to advanced automotive systems. The push for compact and lightweight designs is accelerating the adoption of analog ICs, further strengthening market growth.

North America remains a key player in the analog semiconductors industry, with the market expected to reach USD 46.7 billion by 2034. The United States leads this expansion, projected to generate USD 41 billion within the same period. Strong demand from the automotive, telecommunications, and consumer electronics sectors continues to drive growth in the region. The rapid integration of 5G-enabled devices, artificial intelligence, and IoT technologies is fueling investment in research, development, and production facilities. Leading semiconductor manufacturers are focusing on expanding their fabrication capabilities to meet the surging demand for high-performance analog components.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for energy-efficient devices

- 3.6.1.2 Expansion of IoT and 5G technologies

- 3.6.1.3 Rising electrification in automotive industry

- 3.6.1.4 Growth of renewable energy applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Global semiconductor supply chain constraints

- 3.6.2.2 Intense market competition and alternatives

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 General purpose

- 5.3 Application specific

Chapter 6 Market Estimates & Forecast, By Components, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Data converters

- 6.3 Amplifiers

- 6.4 Power management ICs

- 6.5 Interface ICs

- 6.6 Sensors

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Form Factor, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Integrated circuits (ICs)

- 7.3 Discrete components

Chapter 8 Market Estimates & Forecast, By End-use Industry, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 aerospace & defense

- 8.3 automotive

- 8.4 consumer electronics

- 8.5 Healthcare

- 8.6 Industrial

- 8.7 Telecommunications

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Analog Devices

- 10.2 Broadcom

- 10.3 Diodes

- 10.4 Infineon Technologies

- 10.5 MediaTek

- 10.6 Microchip Technology

- 10.7 MinebeaMitsumi

- 10.8 Murata Manufacturing

- 10.9 NXP Semiconductors

- 10.10 ON Semiconductor

- 10.11 Qorvo

- 10.12 Qualcomm Technologies

- 10.13 Renesas Electronics

- 10.14 Semtech

- 10.15 Skyworks Solutions

- 10.16 ST Microelectronics

- 10.17 Taiwan Semiconductor Manufacturing

- 10.18 Texas Instruments

- 10.19 Toshiba