水素燃料電池車両市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Hydrogen Fuel Cell Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698338

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

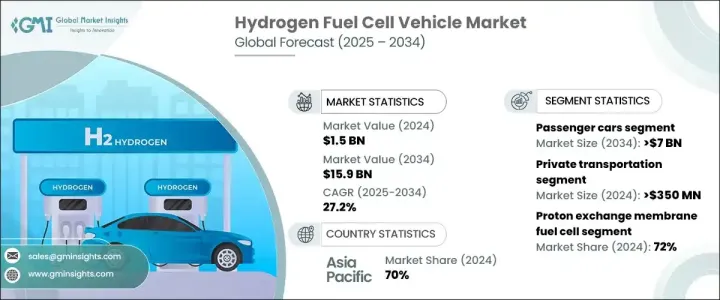

水素燃料電池車両の世界市場は2024年に15億米ドルに達し、2025年から2034年にかけてCAGR27.2%で堅調に拡大すると予測されます。

クリーンエネルギー・ソリューションに対する需要の高まりと、水素燃料補給インフラへの投資の増加が、市場拡大を後押ししています。世界各国政府は、広範な水素補給ネットワークを構築し、水素自動車へのアクセスを確保し、水素自動車の普及を促進するために、多額の資金を投入しています。こうした取り組みは、各国が厳しい排出量目標を達成し、持続可能な輸送ソリューションへの移行を目指す上で極めて重要です。

世界の自動車メーカーがゼロ・エミッション車に重点を移す中、水素燃料電池技術は、従来の内燃機関やバッテリー式電気自動車に代わる有力な選択肢として支持を集めています。水素を燃料とする自動車は、長距離走行性能と急速な燃料補給時間を併せ持つというユニークな利点があり、充電時間の長さといったバッテリー電気自動車に関連する主要な懸念に対処しています。この利点は、クリーンエネルギーへの取り組みを支援する政府の政策とともに、消費者の関心を高め、普及率を加速させています。主要自動車企業は需要増に対応するため生産を拡大しており、複数のメーカーが市場のニーズに応えて水素燃料電池の新モデルを発表しています。さらに、燃料電池技術の進歩により、水素を動力源とするモビリティのコスト効率と効率が向上しており、将来の輸送手段における水素燃料電池の地位はさらに強固なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 159億米ドル |

| CAGR | 27.2% |

水素燃料電池車両市場は、乗用車、商用車、特殊車両など車両タイプ別に区分されます。2024年の市場シェアは乗用車が50%を占め、2034年には70億米ドルに達すると予想されます。ゼロ・エミッション輸送の推進が強まっていることから、自動車メーカーは、航続距離と効率を高めるために燃料電池技術とバッテリー・システムを統合した水素自動車を開発せざるを得なくなっています。消費者は、バッテリー式電気自動車に伴う長時間の充電なしで長距離走行が可能な水素自動車を好む傾向が強まっています。こうした消費者心理の変化が、自動車メーカーによる水素技術への投資を促し、市場成長をさらに後押ししています。

技術面では、市場はプロトン交換膜(PEM)燃料電池、固体酸化物燃料電池、アルカリ燃料電池、リン酸燃料電池、その他のバリエーションに分類されます。2024年には、PEM燃料電池が、その優れた効率、軽量構造、迅速な起動能力により、72%のシェアを占め、市場を独占します。これらの特性により、PEM燃料電池は水素自動車に適した選択肢となっています。膜材料と燃料電池スタック設計の絶え間ない進歩が、製造コストを削減しながら性能向上を促進し、この技術を大量導入に適したものにしています。

アジア太平洋地域は、水素燃料電池車両市場の主要地域となり、2024年には70%のシェアを獲得します。この成長の原動力となっているのは、水素燃料補給インフラへの大規模な政府投資と大規模な水素生産イニシアティブです。同地域の国々は、水素を長期的なエネルギー戦略に積極的に組み入れ、自動車の普及を加速させるために多額の財政的インセンティブを提供しています。自動車メーカーが増大する需要に対応するために生産規模を拡大する中、水素を動力源とするモビリティは勢いを増しており、この地域が世界市場の支配的プレーヤーとしての地位を強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- 価格動向

- コスト内訳分析

- 影響要因

- 促進要因

- 水素燃料電池車両導入に対する政府のインセンティブと補助金の増加

- 水素燃料補給インフラの拡大

- グリーン水素製造への投資の増加

- ゼロエミッション商業輸送への需要の高まり

- 業界の潜在的リスク&課題

- 高い製造コストと燃料補給コスト

- 限られた水素補給インフラ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:自動車別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- 特殊車両

- 産業車両

- 軍用車両

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 固体高分子形燃料電池(PEMFC)

- 固体酸化物形燃料電池(SOFC)

- アルカリ燃料電池

- リン酸型燃料電池

- その他

第7章 市場推計・予測:範囲別、2021年~2034年

- 主要動向

- 短距離(0~250マイル)

- 中距離(251~500マイル)

- 長距離(500マイル以上)

第8章 市場推計・予測:出力範囲別、2021年~2034年

- 主要動向

- 150kW未満

- 150~250kW未満

- 250kW以上

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 民間輸送

- 公共交通

- 産業

- 軍事・防衛

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- BMW

- FAW Group

- Ford

- General Motors

- Great Wall Motor

- Honda

- Hyundai

- Hyzon Motors

- Iveco Group

- MAN Energy Solutions

- Mercedes-Benz

- Nikola Corporation

- Porsche

- Renault

- Riversimple

- SAIC

- Stellantis

- Toyota

- Volkswagen

- Volvo

目次

The Global Hydrogen Fuel Cell Vehicle Market reached USD 1.5 billion in 2024 and is projected to expand at a robust CAGR of 27.2% between 2025 and 2034. The surging demand for clean energy solutions, in line with increasing investments in hydrogen refueling infrastructure, is propelling market expansion. Governments worldwide are making substantial financial commitments to build an extensive hydrogen refueling network, ensuring accessibility and encouraging widespread adoption of hydrogen-powered vehicles. These efforts are crucial as nations strive to meet stringent emissions targets and transition toward sustainable transportation solutions.

As global automotive manufacturers shift focus toward zero-emission vehicles, hydrogen fuel cell technology is gaining traction as a viable alternative to conventional internal combustion engines and battery electric vehicles. Hydrogen-powered vehicles offer a unique advantage by combining long-range capabilities with rapid refueling times, addressing key concerns associated with battery electric vehicles, such as lengthy charging durations. This advantage, along with government policies supporting clean energy initiatives, is fueling consumer interest and accelerating adoption rates. Leading automotive companies are ramping up production to cater to the rising demand, with several manufacturers unveiling new hydrogen fuel cell models in response to market needs. Additionally, ongoing advancements in fuel cell technology are making hydrogen-powered mobility more cost-effective and efficient, further solidifying its position in the future of transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $15.9 Billion |

| CAGR | 27.2% |

The hydrogen fuel cell vehicle market is segmented by vehicle type, including passenger cars, commercial vehicles, and specialized vehicles. In 2024, the passenger car segment held a dominant 50% market share and is expected to generate USD 7 billion by 2034. The increasing push for zero-emission transportation is compelling automakers to develop hydrogen-powered passenger cars that integrate fuel cell technology with battery systems to enhance driving range and efficiency. Consumers are showing a growing preference for hydrogen vehicles due to their ability to travel long distances without the extended charging times associated with battery electric vehicles. This shift in consumer sentiment is driving automakers to invest in hydrogen technology, further boosting market growth.

In terms of technology, the market is categorized into proton exchange membrane (PEM) fuel cells, solid oxide fuel cells, alkaline fuel cells, phosphoric acid fuel cells, and other variants. In 2024, PEM fuel cells dominated the market, holding a 72% share due to their superior efficiency, lightweight structure, and rapid start-up capability. These characteristics make PEM fuel cells the preferred choice for hydrogen-powered vehicles. Continuous advancements in membrane materials and fuel cell stack design are driving performance improvements while reducing production costs, making the technology more accessible for mass adoption.

Asia Pacific emerged as the leading region in the hydrogen fuel cell vehicle market, capturing a significant 70% share in 2024. This growth is driven by extensive government investments in hydrogen refueling infrastructure and large-scale hydrogen production initiatives. Countries across the region are actively incorporating hydrogen into their long-term energy strategies, providing substantial financial incentives to accelerate vehicle adoption. As automakers scale up production to meet growing demand, hydrogen-powered mobility is gaining momentum, reinforcing the region's position as a dominant player in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End Use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trends

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising government incentives and subsidies for adoption of hydrogen fuel cell vehicles

- 3.10.1.2 Expanding hydrogen refueling infrastructure

- 3.10.1.3 Increasing investments in green hydrogen production

- 3.10.1.4 Growing demand for zero-emission commercial transport

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High production and refueling costs

- 3.10.2.2 Limited hydrogen refueling infrastructure

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Heavy Commercial Vehicles (HCV)

- 5.4 Specialized Vehicles

- 5.4.1 Industrial vehicles

- 5.4.2 Military vehicles

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Proton Exchange Membrane Fuel Cells (PEMFCs)

- 6.3 Solid Oxide Fuel Cells (SOFCs)

- 6.4 Alkaline fuel cell

- 6.5 Phosphoric acid fuel cell

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Range, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short range (0-250 Miles)

- 7.3 Medium range (251-500 Miles)

- 7.4 Long range (Above 500 Miles)

Chapter 8 Market Estimates & Forecast, By Power Range, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Less than 150kW

- 8.3 150-250kW

- 8.4 Above 250kW

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Private transportation

- 9.3 Public transportation

- 9.4 Industrial

- 9.5 Military & defense

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 BMW

- 11.2 FAW Group

- 11.3 Ford

- 11.4 General Motors

- 11.5 Great Wall Motor

- 11.6 Honda

- 11.7 Hyundai

- 11.8 Hyzon Motors

- 11.9 Iveco Group

- 11.10 MAN Energy Solutions

- 11.11 Mercedes-Benz

- 11.12 Nikola Corporation

- 11.13 Porsche

- 11.14 Renault

- 11.15 Riversimple

- 11.16 SAIC

- 11.17 Stellantis

- 11.18 Toyota

- 11.19 Volkswagen

- 11.20 Volvo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日