|

市場調査レポート

商品コード

1698333

スマートドラッグデリバリーシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Smart Drug Delivery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| スマートドラッグデリバリーシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

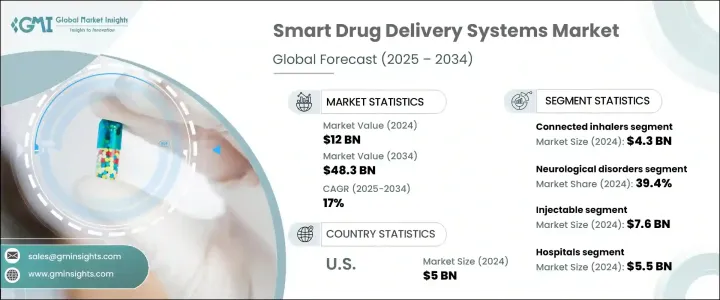

スマートドラッグデリバリーシステムの世界市場は、2024年に120億米ドルと評価され、2025年から2034年にかけてCAGR 17%で成長すると予測されています。

これらの先進システムは、治療薬を正確に送達し、副作用を低減し、患者の転帰を改善することにより、薬効を高める。スマートドラッグデリバリーは、ナノテクノロジー、マイクロセンサー、制御放出メカニズムを統合し、薬剤投与を最適化します。糖尿病、がん、心血管疾患などの慢性疾患の有病率の上昇が、標的ドラッグデリバリーソリューションの需要に拍車をかけています。ヘルスケアはデジタルヘルス技術や患者中心のケアへとシフトしており、こうしたインテリジェントなドラッグデリバリーシステムの採用が増加しています。ナノテクノロジー、バイオマテリアル、センサーの技術的進歩は、これらのシステムの精度と効率を向上させ、市場拡大の原動力となっています。

市場は製品別に分類され、コネクテッド吸入器は2024年に43億米ドルの売上を上げ、CAGR 16.8%で成長する見込みです。喘息や慢性呼吸器疾患の罹患率の上昇が、リアルタイムのデータ追跡や使用状況のモニタリングを提供し、治療のアドヒアランスを向上させるこれらのデバイスの需要を促進しています。センサーとデジタルアプリケーションの統合は、患者の関与と症状管理を強化し、市場成長をさらに促進します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 120億米ドル |

| 予測金額 | 483億米ドル |

| CAGR | 17% |

用途別では、神経疾患分野が39.4%の売上シェアを占め、2024年には47億米ドルに達しました。アルツハイマー病、パーキンソン病、てんかん、多発性硬化症の増加により、治療効果を高める高度なドラッグデリバリーソリューションに対する需要が高まっています。これらの技術は薬剤投与の精度を高め、治療成果を最適化し、治療に関連する課題を軽減します。複雑な神経疾患に対して標的療法を提供する能力は、セグメントの成長に大きく寄与しています。

市場は投与経路別に注射剤、吸入剤、経口ドラッグデリバリーに区分されます。注射剤セグメントは、材料科学、ナノテクノロジー、スマートセンサーの進歩が牽引し、2024年の売上高が76億米ドルでリードしています。これらの技術革新はドラッグデリバリー、モニタリング、カスタマイズを強化し、正確な投与と治療結果の改善を保証します。米国FDAなどの規制当局による承認がこれらのソリューションの商業化を後押しし、市場の成長を加速させています。

病院は最大の最終用途セグメントを占め、2024年には55億米ドルの収益を生み出します。病院におけるスマートドラッグデリバリー技術の採用が増加していることで、投薬管理が改善され、治療のアドヒアランスが向上し、患者の治療が最適化されています。入院率の増加、ヘルスケアインフラの進歩、スマート医療機器への投資が、セグメント拡大の原動力となっています。

地域別では北米がスマートドラッグデリバリーシステム市場をリードし、2024年には55億米ドルに達し、2034年には222億米ドルに達すると予測されています。米国は2024年に50億米ドルの収益を上げ、地域市場を独占しました。製薬企業と医療機器企業の強力な協力関係、革新的医療技術に対する規制当局の支援が、この地域の市場成長を後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の増加

- デジタルヘルス技術の採用拡大

- 患者中心の在宅医療へのシフト

- ドラッグデリバリーの技術進歩

- 業界の潜在的リスク&課題

- デバイスの開発と生産に伴う高コスト

- 標準化の欠如

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- コネクテッド吸入器

- コネクテッド自動注射器

- コネクテッドペン型注射器

- 接続型ウェアラブル注射器

- アドオンセンサー

- その他の製品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 代謝疾患

- 神経疾患

- 呼吸器疾患

- ホルモン障害

- その他の用途

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 注射剤

- 吸入

- 経口

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 診療所

- 在宅医療

- 外来医療

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amiko Digital Health

- Becton, Dickinson and Company

- Biocorp

- Elcam Medical

- Johnson &Johnson

- Medtronic

- Merck

- Nemera

- Novo Nordisk

- Pfizer

- Phillips-Medisize

- Portal Instruments

- Teva Pharmaceutical Industries

- West Pharmaceutical Services

- Ypsomed

The Global Smart Drug Delivery Systems Market was valued at USD 12 billion in 2024 and is projected to grow at a CAGR of 17% from 2025 to 2034. These advanced systems enhance drug efficacy by delivering therapeutic agents with precision, reducing side effects, and improving patient outcomes. Smart drug delivery integrates nanotechnology, microsensors, and controlled-release mechanisms to optimize medication administration. The rising prevalence of chronic diseases, including diabetes, cancer, and cardiovascular conditions, is fueling the demand for targeted drug delivery solutions. With healthcare shifting towards digital health technologies and patient-centric care, the adoption of these intelligent drug delivery systems is increasing. Technological advancements in nanotechnology, biomaterials, and sensors are refining the accuracy and efficiency of these systems, driving market expansion.

The market is categorized by product, with connected inhalers generating USD 4.3 billion in revenue in 2024 and set to grow at a CAGR of 16.8%. The rising incidence of asthma and chronic respiratory diseases is driving demand for these devices, which offer real-time data tracking and usage monitoring, improving treatment adherence. The integration of sensors and digital applications enhances patient engagement and symptom management, further propelling market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12 Billion |

| Forecast Value | $48.3 Billion |

| CAGR | 17% |

By application, the neurological disorders segment held a 39.4% revenue share, reaching USD 4.7 billion in 2024. The increasing occurrence of Alzheimer's disease, Parkinson's disease, epilepsy, and multiple sclerosis is generating demand for advanced drug delivery solutions that enhance treatment efficacy. These technologies improve drug administration accuracy, optimizing therapeutic outcomes and reducing treatment-related challenges. The ability to deliver targeted therapies for complex neurological conditions contributes significantly to segment growth.

The market is segmented by route of administration into injectables, inhalation, and oral drug delivery. The injectable segment led with USD 7.6 billion in revenue in 2024, driven by advancements in materials science, nanotechnology, and smart sensors. These innovations enhance drug delivery, monitoring, and customization, ensuring precise dosing and improved treatment outcomes. Regulatory approvals from agencies like the U.S. FDA are supporting the commercialization of these solutions, accelerating market growth.

Hospitals represent the largest end-use segment, generating USD 5.5 billion in revenue in 2024. The increasing adoption of smart drug delivery technologies in hospitals is improving medication management, ensuring better treatment adherence, and optimizing patient care. Growing hospitalization rates, advancements in healthcare infrastructure, and investments in smart medical devices are driving segment expansion.

Regionally, North America led the smart drug delivery systems market, reaching USD 5.5 billion in 2024, with projections to hit USD 22.2 billion by 2034. The U.S. dominated the regional market with USD 5 billion in revenue in 2024. Strong collaborations between pharmaceutical and medical device companies, along with regulatory support for innovative medical technologies, are propelling market growth in the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Growing adoption of digital health technologies

- 3.2.1.3 Shift towards patient-centric and home-based care

- 3.2.1.4 Technological advancements in drug delivery

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with device development and production

- 3.2.2.2 Lack of standardization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Connected inhalers

- 5.3 Connected autoinjectors

- 5.4 Connected pen injectors

- 5.5 Connected wearable injectors

- 5.6 Add-on sensors

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metabolic disorders

- 6.3 Neurological disorders

- 6.4 Respiratory disorders

- 6.5 Hormonal disorders

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Inhalation

- 7.4 Oral

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Clinics

- 8.4 Home care

- 8.5 Ambulatory care settings

- 8.6 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amiko Digital Health

- 10.2 Becton, Dickinson and Company

- 10.3 Biocorp

- 10.4 Elcam Medical

- 10.5 Johnson & Johnson

- 10.6 Medtronic

- 10.7 Merck

- 10.8 Nemera

- 10.9 Novo Nordisk

- 10.10 Pfizer

- 10.11 Phillips-Medisize

- 10.12 Portal Instruments

- 10.13 Teva Pharmaceutical Industries

- 10.14 West Pharmaceutical Services

- 10.15 Ypsomed