|

市場調査レポート

商品コード

1698324

人工知能端末市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Artificial Intelligence (AI) Terminal Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 人工知能端末市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月14日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

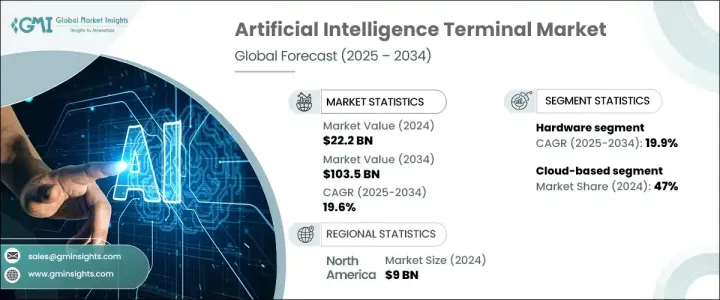

世界の人工知能端末市場の2024年の市場規模は222億米ドルで、2025年から2034年にかけてCAGR 19.6%で拡大すると予測されています。

AIチップセット、ニューラル・プロセッシング・ユニット(NPU)、AIアクセラレータの進歩が成長の原動力となっており、エネルギー効率を改善しながら性能を向上させる。AI端末は、クラウドコンピューティングへの依存を減らし、ローカルでデータを処理するエッジAIの恩恵を受ける。これにより、応答時間が改善され、セキュリティが強化され、企業はリアルタイムの意思決定のための低遅延AI処理を実現できます。AIを搭載したIoT機器、家電製品、スマートヘルスケアソリューションの採用増加が市場拡大に寄与しています。AIプロセッサの技術向上により、AI端末は次世代コンピューティングに不可欠なものとなっています。

市場はコンポーネント別にハードウェアとソフトウェアに分類されます。2024年には、ハードウェアがこの分野を支配し、152億米ドルの収益を上げており、予測期間を通じてCAGR 19.9%で成長すると予測されています。AI端末はGPU、FPGA、ASICなどの強力なプロセッサに依存しており、これらはリアルタイムのAI計算に不可欠です。自動車、ヘルスケア、製造業などの業界では、自動化をサポートし、AIベースの意思決定を強化するために、AI推論ハードウェアを統合しています。AIチップセット、組み込みデバイス、AI対応サーバーへの投資の増加は、ハードウェアの優位性をさらに強化しています。AIoT、自律システム、AI主導の監視ソリューションの拡大も成長を促進しており、フィンテックAIハードウェアの市場を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 222億米ドル |

| 予測金額 | 1,035億米ドル |

| CAGR | 19.6% |

AI端末市場の展開形態には、オンプレミス、クラウドベース、ハイブリッドソリューションがあります。2024年には、クラウドベースのソリューションが47%のシェアで市場をリードし、2034年までのCAGRは20%を超えると予想されます。クラウドコンピューティングにより、企業は多額のハードウェア投資をすることなくAIアプリケーションを拡張することができ、複数の業界にわたってAIモデルのトレーニング、リアルタイムのデータ分析、推論をサポートすることができます。企業が生成するAI主導のデータ量が増加するにつれて、クラウド・インフラストラクチャに対する需要は増加の一途をたどっています。クラウドベースのシステムと統合されたAI端末は、効率的なデータ収集と処理を可能にし、高度なAI機能を求める企業にとって不可欠なツールとなっています。

技術別に見ると、市場は機械学習(ML)および深層学習(DL)、コンピューター・ビジョン、ロボティック・プロセス・オートメーション、IoTセンサー、その他のAI駆動技術に区分されます。MLとDLは、膨大な量のデータを処理し、パターンを特定し、リアルタイムでアクションを実行する能力により、優位性を保っています。ディープラーニング・ニューラルネットワークを活用したAIシステムは、自然言語処理(NLP)、音声認識、自律システムの能力を強化します。銀行、小売、ヘルスケアにおけるAIソリューションのニーズの高まりが、この分野での採用を加速させています。

北米は2024年に最大の市場シェアを占め、世界のAI端末市場の約40%を占め、約90億米ドルの収益を生み出しました。この地域は、AI主導のハードウェア、エッジコンピューティング・ソリューション、半導体技術への強力な投資から利益を得ています。大手テクノロジー企業やAIチップセットメーカーの存在が、ヘルスケア、防衛、小売を含む業界全体の市場拡大を支えています。エッジベースのAIコンピューティング・ソリューションの開発強化は、特にデータ・プライバシーとセキュリティの向上を必要とするアプリケーションでの採用をさらに促進しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- メーカー

- センサープロバイダー

- ソフトウェア開発企業

- テクノロジー・インテグレーター

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 促進要因

- エッジAI技術の進歩

- AI搭載デバイスの需要増加

- 5GおよびIoTネットワークの拡大

- 自動車とヘルスケアにおけるAI統合の拡大

- AIインフラへの政府と企業の投資

- 業界の潜在的リスク&課題

- 高い初期投資と導入コスト

- データプライバシーとセキュリティへの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- MLとDL

- コンピュータビジョン

- ロボティック・プロセス・オートメーション

- IoTセンサー

- その他

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 輸送

- ヘルスケア

- 小売

- BFSI

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Adobe

- Alibaba Group

- Amazon

- Apple

- Bosch

- Cisco

- Dell Technologies

- Google(Alphabet inc.)

- Huawei Technologies

- IBM

- Intel

- Meta Platforms

- Microsoft

- Nvidia

- Oracle

- Sony

- Tencent Holdings

- Tesla

- VMware

- Zoom Video Communications

The Global Artificial Intelligence Terminal Market was valued at USD 22.2 billion in 2024 and is expected to expand at a CAGR of 19.6% from 2025 to 2034. Growth is fueled by advancements in AI chipsets, neural processing units (NPUs), and AI accelerators, which enhance performance while improving energy efficiency. AI terminals benefit from edge AI, which processes data locally, reducing reliance on cloud computing. This improves response times, strengthens security, and enables businesses to achieve low-latency AI processing for real-time decision-making. Increasing adoption of AI-powered IoT devices, consumer electronics, and smart healthcare solutions contributes to market expansion. Technological improvements in AI processors are making AI terminals essential for next-generation computing.

The market is categorized by component into hardware and software. In 2024, hardware dominated the sector, generating USD 15.2 billion in revenue, and is projected to grow at a CAGR of 19.9% through the forecast period. AI terminals rely on powerful processors, including GPUs, FPGAs, and ASICs, which are crucial for real-time AI computations. Industries such as automotive, healthcare, and manufacturing are integrating AI inference hardware to support automation and enhance AI-based decision-making. Increased investments in AI chipsets, embedded devices, and AI-enabled servers further reinforce hardware's dominance. The expansion of AIoT, autonomous systems, and AI-driven surveillance solutions is also driving growth, strengthening the market for fintech AI hardware.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.2 Billion |

| Forecast Value | $103.5 Billion |

| CAGR | 19.6% |

Deployment modes in the AI terminal market include on-premises, cloud-based, and hybrid solutions. In 2024, cloud-based solutions led the market with a 47% share and are expected to grow at a CAGR exceeding 20% through 2034. Cloud computing allows enterprises to scale AI applications without substantial hardware investments, supporting AI model training, real-time data analysis, and inference across multiple industries. As businesses generate increasing amounts of AI-driven data, demand for cloud infrastructure continues to rise. AI terminals integrated with cloud-based systems enable efficient data collection and processing, making them an essential tool for enterprises seeking advanced AI capabilities.

By technology, the market is segmented into machine learning (ML) and deep learning (DL), computer vision, robotic process automation, IoT sensors, and other AI-driven technologies. ML and DL remain dominant due to their ability to process vast amounts of data, identify patterns, and execute actions in real-time. AI systems utilizing deep learning neural networks enhance capabilities in natural language processing (NLP), speech recognition, and autonomous systems. The increasing need for AI solutions across banking, retail, and healthcare is accelerating adoption in this segment.

North America held the largest market share in 2024, accounting for approximately 40% of the global AI terminal market, generating around USD 9 billion in revenue. The region benefits from strong investments in AI-driven hardware, edge computing solutions, and semiconductor technologies. The presence of leading technology firms and AI chipset manufacturers supports market expansion across industries, including healthcare, defense, and retail. Enhanced development of edge-based AI computing solutions is further fueling adoption, particularly in applications requiring improved data privacy and security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturer

- 3.2.2 Sensor providers

- 3.2.3 Software developers

- 3.2.4 Technology Integrators

- 3.2.5 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Advancements in edge AI technology

- 3.8.1.2 Rising demand for AI-powered devices

- 3.8.1.3 Expansion of 5G and IoT networks

- 3.8.1.4 Growing AI integration in automotive and healthcare

- 3.8.1.5 Government and enterprise investments in AI infrastructure

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial investment and deployment costs

- 3.8.2.2 Data privacy and security concerns

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 ML and DL

- 6.3 Computer vision

- 6.4 Robotic process automation

- 6.5 IOT sensors

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Transportation

- 8.3 Healthcare

- 8.4 Retail

- 8.5 BFSI

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Adobe

- 10.2 Alibaba Group

- 10.3 Amazon

- 10.4 Apple

- 10.5 Bosch

- 10.6 Cisco

- 10.7 Dell Technologies

- 10.8 Google (Alphabet inc.)

- 10.9 Huawei Technologies

- 10.10 IBM

- 10.11 Intel

- 10.12 Meta Platforms

- 10.13 Microsoft

- 10.14 Nvidia

- 10.15 Oracle

- 10.16 Sony

- 10.17 Tencent Holdings

- 10.18 Tesla

- 10.19 VMware

- 10.20 Zoom Video Communications