|

市場調査レポート

商品コード

1892877

自動車用スパークプラグ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Spark Plug Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用スパークプラグ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月05日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

概要

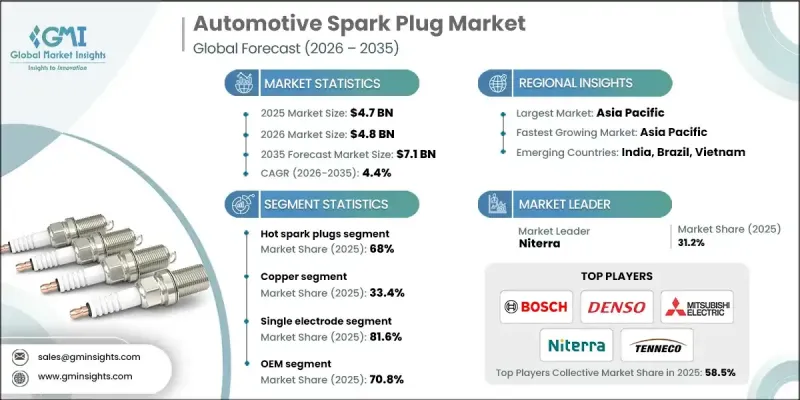

世界の自動車用スパークプラグ市場は、2025年に47億米ドルと評価され、2035年までにCAGR4.4%で成長し、71億米ドルに達すると予測されています。

この成長は、世界の新車生産台数の着実な増加と、ガソリン車に対する消費者の継続的な選好によって支えられています。また、燃費効率の向上への移行も、先進的なスパークプラグ技術の採用拡大を促進しており、効率を最大化するように設計された新しいエンジン構造が採用されています。メーカー各社は、イリジウムやプラチナなどの材料の使用を製品ライン全体に拡大しており、これによりより耐久性が高く効率的な点火性能が実現されています。現代の燃焼システムは燃料効率を約10%向上させており、これにより高品質スパークプラグ部品の普及が促進されています。都市部のモビリティ拡大動向に伴い、火花点火システムに依存するコンパクトエンジンの需要が増加しています。アフターマーケットも引き続き大きな貢献要因であり、特に2024年に車両の平均使用年数が12年を超えたことで、年間交換サイクルが増加しています。高性能金属の継続的な改良も、スパークプラグの寿命と点火信頼性の向上に寄与し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 47億米ドル |

| 予測金額 | 71億米ドル |

| CAGR | 4.4% |

2025年時点で、高温スパークプラグセグメントは68%のシェアを占めており、このカテゴリーは2026年から2035年にかけてCAGR 4.7%で拡大すると予測されています。これらのプラグは、広い温度範囲で信頼性の高い点火を維持するため、従来型ガソリンエンジン向けに引き続き好まれています。その設計は効果的な放熱をサポートし、主要な世界の地域の大都市圏で一般的な低速走行時の汚れを抑制するのに役立ちます。

単極スパークプラグセグメントは2025年に81.6%のシェアを占めました。2024年の世界乗用車生産台数が7,600万台を超えることを背景に、大衆向け乗用車および二輪車向けの主要選択肢としての地位を維持しています。エントリーレベルおよびミドルクラスのエンジンの多くは、依然として単極電極システムに依存しています。これは予測可能な動作と低いメンテナンスコストを提供するためです。これにより、老朽化した車両の基盤が大きな地域のアフターマーケットにおいて、特に魅力的な選択肢となっています。

中国自動車用スパークプラグ市場は2024年に46.8%のシェアを占め、2025年には8億2,440万米ドルの規模に達しました。成長は自動車販売台数の増加と急速な都市拡大に連動しており、乗用車生産台数は2,800万台を超えて増加を続けています。これにより主要都市と地方コミュニティ双方において、OEM需要と交換サイクルが加速しています。二輪車による移動手段は依然として交通構造の大きな構成要素であり、2024年には約700万台のオートバイおよびスクーターが生産されました。その大半は銅またはプラチナ製スパークプラグに依存しており、今後も継続的な交換需要が堅調に推移することが見込まれます。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- ガソリン車市場の成長

- 高効率エンジンへの移行

- アフターマーケット活動の増加

- 貴金属プラグの採用状況

- 業界の潜在的リスク&課題

- 電気自動車の普及拡大

- 原材料コストの上昇

- 市場機会

- 世界アフターマーケットの拡大

- 先進点火システムの開発

- 新興市場における二輪車需要の成長

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 電極材料の進化(銅からルテニウムへ)

- 微細線技術の開発

- 多電極設計の革新

- プレチャンバースパークプラグ技術

- IoTおよびスマート診断の統合

- レーザー溶接製造技術の進展

- 温度範囲最適化技術

- 次世代材料

- 新興技術

- 現在の技術動向

- 価格動向

- OEMとアフターマーケットの価格差

- 地域別価格変動

- 原材料コストの影響

- 輸入・輸出価格分析

- 将来の価格推移

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許・知的財産分析

- 電極材料別有効特許

- 地理的特許分布

- 主要特許保有者

- 新興技術特許(スマートプラグ)

- 特許満了時期のタイムライン(2024-2034)

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 投資・資金調達分析

- メーカー別研究開発投資動向

- 代替燃料対応投資

- 製造能力の拡張

- 戦略的提携及び合弁事業

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:製品別2022 2035

- 主要動向

- 高温スパークプラグ

- コールドスパークプラグ

第6章 市場推計・予測:材料別、2022-2035

- 主要動向

- 銅

- プラチナ

- イリジウム

- その他

第7章 市場推計・予測:電極別、2022-2035

- 主要動向

- 単一電極

- ツイン電極

- マルチ電極

- 表面放電

第8章 市場推計・予測:販売チャネル別、2022-2035

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:車両別、2022-2035

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 軽自動車

- 中型トラック

- 大型車両

- 二輪車

- オートバイ

- スクーター

第10章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第11章 企業プロファイル

- 世界プレイヤー

- ACDelco

- Autolite

- Bosch

- DENSO

- MAHLE

- Mitsubishi Electric

- Niterra

- Tenneco

- Valeo

- 地域メーカー

- BorgWarner

- Brisk Spark Plug Company

- E3 Spark Plugs

- Hella

- MAGNETI MARELLI PARTS &SERVICES

- MSD Performance

- Stitt Spark Plug Company

- Zhuzhou Torch Spark Plug

- 新興企業/ディスラプター

- Iskra Spark Plugs

- Nanjing Leidian

- Prenco Progress &Engineering Corporation

- Pulstar

- SMP Automotive

- Weichai Power