ビール缶市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Beer Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698291

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

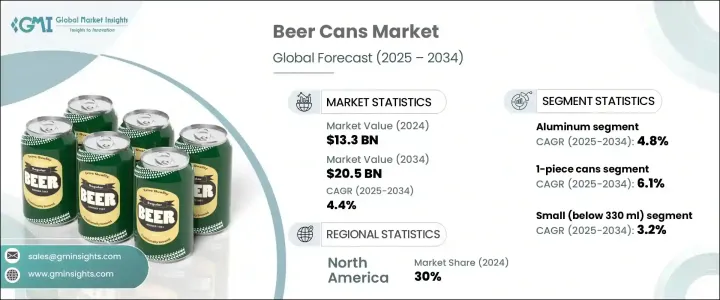

世界のビール缶市場は着実な成長を遂げており、2024年には133億米ドルに達し、2025年から2034年にかけてのCAGRは4.4%と予測されています。

特にクラフトビールとプレミアムビールの消費増加が市場拡大の主な要因です。消費者は、鮮度を保ち、光と酸素の暴露を遮断し、携帯性を高める缶ビールへの関心を高めています。一方、ビール会社は、持続可能性、製品保存、コスト効率を優先するため、アルミ包装にシフトしています。クラフトビール産業が繁栄を続ける中、独特の風味と炭酸を保持する高品質パッケージへの需要が急増しています。

市場関係者もまた、持続可能なパッケージング・ソリューションに注力することで、消費者の嗜好の変化に対応しています。軽量でリサイクル可能なことで知られるアルミ缶が、パッケージングの有力な選択肢として浮上しています。この分野は、ビールの品質に影響を与える可能性のある外的要因から優れた保護を提供する能力によって、予測期間中にCAGR 4.8%で成長すると予測されています。輸送コストの削減と製品の貯蔵寿命の延長により、アルミニウムは大規模・小規模のビール醸造所の両方に好まれる素材となっています。環境に対する責任が重視されるようになったことで、この傾向はさらに強まり、ビールメーカーは環境に優しい包装を生産戦略に取り入れるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 133億米ドル |

| 予測金額 | 205億米ドル |

| CAGR | 4.4% |

市場は製品タイプによっても区分され、1ピース缶、2ピース缶、3ピース缶があります。1ピース缶セグメントは力強い成長を遂げており、予測期間中にCAGR 6.1%を記録すると予測されています。これらの缶は継ぎ目のない構造で、漏れ防止と耐久性が強化されているため人気を集めています。加圧ビールや窒素注入ビールはこのフォーマットの恩恵を受け、プレミアムビールやスペシャルティビールに好まれる選択肢となっています。ビールメーカーがハイエンド商品の提供に注力する中、1ピース缶の需要は加速しています。

缶ビール市場では北米が大きなシェアを占めており、2024年には総売上の30%を占める。特にクラフトビールとプレミアム・セグメントにおける高いビール消費量が、この地域の需要を引き続き促進しています。米国だけでも2024年に32億米ドルの売上があり、クラフトビール人気の高まりとeコマース・チャネルの拡大が市場拡大を支えています。アルミリサイクルのエコシステムが発達し、持続可能なパッケージングに対する消費者の意識が高まっているため、ビール会社は軽量で環境に優しい缶への移行を促しています。消費者の嗜好が多様なビールフレーバーやパッケージング効率の改善にシフトする中、メーカーは進化する業界の需要に応えるべく生産戦略を最適化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ビール消費量の増加

- クラフトビールとプレミアムセグメントの成長

- 持続可能性のためのガラス瓶からアルミ缶へのシフト

- ノンアルコール・低アルコールビールの成長

- コスト効率と製造の進歩

- 業界の潜在的リスク&課題

- アルコール包装に関する規制上の課題と規制

- 代替包装材料との競合

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- アルミニウム

- スチール

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 1ピース缶

- 2ピース缶

- 3ピース缶

第7章 市場推計・予測:容量別、2021~2034年

- 主要動向

- 小容量(330ml以下)

- 中容量(330ml~500ml)

- 大容量(500ml以上)

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Ardagh Group

- Asahi Group

- Baixicans

- Ball

- Canpack

- Ceylon Beverage Can

- Crown

- Daiwa Can

- Erjin Packaging

- G3 Enterprises

- Hainan Zhenxi

- Nampak

- Orora Packaging

- Scan Holdings

- Shining Aluminum

- Thai Beverage Can

- Toyo Seikan

- Visy

目次

The Global Beer Cans Market is witnessing steady growth, reaching USD 13.3 billion in 2024, with projections indicating a CAGR of 4.4% between 2025 and 2034. Rising beer consumption, particularly in the craft and premium segments, is a key driver of market expansion. Consumers are increasingly gravitating toward canned beer for its ability to maintain freshness, block light and oxygen exposure, and enhance portability. Breweries, on the other hand, are shifting toward aluminum packaging as they prioritize sustainability, product preservation, and cost efficiency. With the craft beer industry continuing to thrive, demand for high-quality packaging that preserves unique flavors and carbonation is surging.

Market players are also responding to changing consumer preferences by focusing on sustainable packaging solutions. Aluminum cans, known for their lightweight nature and recyclability, are emerging as the dominant packaging choice. This segment is projected to grow at a CAGR of 4.8% during the forecast period, driven by its ability to provide superior protection against external elements that can impact beer quality. Reduced transportation costs and extended product shelf life make aluminum the preferred material for both large and small-scale breweries. The increasing emphasis on environmental responsibility is further reinforcing this trend, prompting beer manufacturers to integrate eco-friendly packaging into their production strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.3 Billion |

| Forecast Value | $20.5 Billion |

| CAGR | 4.4% |

The market is also segmented by product type, with 1-piece, 2-piece, and 3-piece cans available. The 1-piece can segment is experiencing robust growth, projected to register a CAGR of 6.1% over the forecast timeline. These cans are gaining popularity due to their seamless structure, which offers enhanced leak protection and durability. Pressurized and nitrogen-infused beers benefit from this format, making it a preferred choice for premium and specialty beer varieties. With breweries focusing on delivering high-end offerings, the demand for 1-piece cans is accelerating.

North America holds a significant share of the beer cans market, accounting for 30% of the total revenue in 2024. High beer consumption, particularly in craft and premium segments, continues to fuel regional demand. The United States alone generated USD 3.2 billion in 2024, with rising craft beer popularity and expanding e-commerce channels supporting market expansion. A well-developed aluminum recycling ecosystem and growing consumer awareness of sustainable packaging are prompting breweries to transition to lightweight, eco-friendly cans. As consumer preferences shift toward diverse beer flavors and improved packaging efficiency, manufacturers are optimizing their production strategies to meet evolving industry demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising beer consumption

- 3.2.1.2 Growth of craft beer and premium segments

- 3.2.1.3 Shift from glass bottles to aluminum cans for sustainability

- 3.2.1.4 Growth of non-alcoholic & low-alcohol beer

- 3.2.1.5 Cost efficiency & manufacturing advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory challenges and restrictions on alcohol packaging

- 3.2.2.2 Competition from alternative packaging materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn & Units)

- 6.1 Key trends

- 6.2 1-piece cans

- 6.3 2-piece cans

- 6.4 3-piece cans

Chapter 7 Market Estimates and Forecast, By Capacity, 2021 – 2034 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Small (Below 330 ml)

- 7.3 Medium (330 ml – 500 ml)

- 7.4 Large (Above 500 ml)

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ardagh Group

- 9.2 Asahi Group

- 9.3 Baixicans

- 9.4 Ball

- 9.5 Canpack

- 9.6 Ceylon Beverage Can

- 9.7 Crown

- 9.8 Daiwa Can

- 9.9 Erjin Packaging

- 9.10 G3 Enterprises

- 9.11 Hainan Zhenxi

- 9.12 Nampak

- 9.13 Orora Packaging

- 9.14 Scan Holdings

- 9.15 Shining Aluminum

- 9.16 Thai Beverage Can

- 9.17 Toyo Seikan

- 9.18 Visy

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日