データセンター支援インフラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Data Center Support Infrastructure Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698276

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

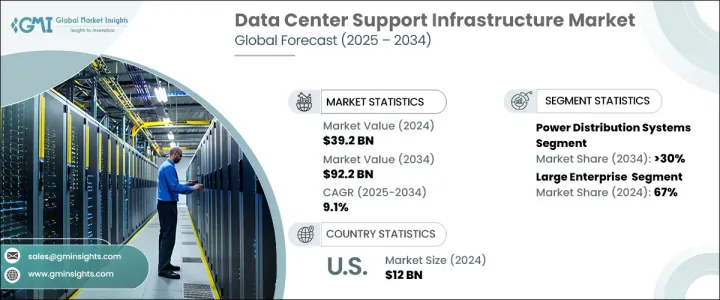

世界のデータセンター支援インフラ市場は、2024年に392億米ドルに達し、2025年から2034年にかけてCAGR 9.1%で成長すると予測されています。

デジタルトランスフォーメーション、クラウドコンピューティング、人工知能(AI)などの先進技術の採用が増加しており、効率的で拡張性の高いデータセンターインフラへの需要が引き続き高まっています。企業がデータ主導の業務にますます依存するようになる中、さまざまな業界の企業が、効率性、セキュリティ、持続可能性を高めるためにデータセンターの拡張と近代化を優先しています。

ビッグデータ分析、機械学習、モノのインターネット(IoT)の急速な進歩に伴い、信頼性の高いデータストレージ、処理、管理ソリューションに対するニーズはかつてないほど高まっています。企業は、運用の継続性を維持しダウンタイムを防止するため、配電、冷却ソリューション、セキュリティシステムに多額の投資を行っています。ハイブリッド・クラウド・モデルの採用が増加しており、企業はオンプレミス・インフラストラクチャとクラウドベースのサービスを統合してパフォーマンスとコスト効率を最適化するため、市場拡大にさらに拍車をかけています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 392億米ドル |

| 予測金額 | 922億米ドル |

| CAGR | 9.1% |

同市場には、配電システム、冷却システム、ラックとエンクロージャー、セキュリティ・システム、敷地・施設インフラなど、複数のインフラ・セグメントが含まれます。なかでも配電システムは2024年に30%のシェアを占め、最も重要なセグメントとなっています。これらのシステムは、発電機、無停電電源装置(UPS)、配電ユニット(PDU)で構成され、データセンター内の継続的な電力供給の維持に重要な役割を果たしています。PDUはさまざまなIT機器への配電に不可欠であり、UPSシステムは停電中も重要なシステムの稼働を確保します。発電機はバックアップ電源として機能し、データセンター運用の中断を防ぐ信頼性をさらに高めます。データトラフィックの増加やクラウドサービスへの依存度の高まりに伴い、企業は拡大するデータ処理ニーズをサポートするため、エネルギー効率と耐障害性に優れた電力インフラを重視するようになっています。

市場は、中小企業(SME)や大企業など、組織の規模に基づいてさらに細分化されます。2024年には、大企業が67%のシェアを占めています。これらの企業は、膨大なデータ負荷を管理し、処理能力を強化するためにITインフラを拡張しています。企業が運用効率の最適化とエネルギー消費の最小化を目指す中、高度な配電、高速ネットワーキング、次世代冷却ソリューションへの投資が加速しています。AI、自動化、リアルタイムのデータ分析が普及する中、企業はインテリジェントなインフラ管理ソリューションを統合し、運用の合理化とコスト削減を図っています。ハイブリッドクラウドソリューションも市場情勢を再構築しており、大企業はオンプレミスのデータセンターとクラウドベースのプラットフォームを組み合わせて活用することで、より高い柔軟性、拡張性、データセキュリティを実現しています。

北米のデータセンター支援インフラ市場は35%のシェアを占め、米国が最大の貢献国となっています。2024年、米国はクラウドコンピューティング、AIを活用したアプリケーション、デジタルサービスへの旺盛な需要に牽引され、データセンター支援インフラから120億米ドルの収益を上げました。最も技術的に進んだ地域の1つである米国は、引き続き世界のデータセンター産業をリードしており、ハイパースケールデータセンターやコロケーション施設は大幅な拡大を示しています。IT、通信、金融、ヘルスケアなど、さまざまな業界の企業が、デジタルトランスフォーメーションの取り組みを支援するため、最先端のインフラに多額の投資を行っています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- AIソフトウェアプロバイダー

- サービスプロバイダー

- データプロバイダー

- システムインテグレーター

- エンドユース

- サプライヤーの状況

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- ケーススタディ

- 影響要因

- 促進要因

- クラウド・サービスへの需要の高まり

- ハイパースケールとエッジデータセンターの台頭

- データセンター設計の技術的進歩

- 政府の取り組みと政策

- 業界の潜在的リスク&課題

- エネルギー消費と環境への影響の増大

- データの安全性とセキュリティへの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:インフラ別、2021年~2034年

- 主要動向

- 配電システム

- 冷却システム

- ラックとエンクロージャー

- サイト・施設インフラ

- セキュリティシステム

第6章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推定・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:ティア別、2021年~2034年

- 主要動向

- ティアI

- ティアII

- ティアIII

- ティアIV

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- IT &テレコム

- BFSI

- ヘルスケア&ライフサイエンス

- 政府&防衛

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ABB

- Asetek

- Black Box

- Cisco Systems

- Delta Electronics

- Eaton

- Fujitsu

- Hewlett Packard Enterprise(HPE)

- Huawei Technologies

- IBM

- Johnson Controls

- Legrand

- Mitsubishi Electric

- Raritan

- Rittal

- Schneider Electric

- Siemens

- STULZ

- Toshiba

- Vertiv

目次

The Global Data Center Support Infrastructure Market reached USD 39.2 billion in 2024 and is projected to grow at a CAGR of 9.1% between 2025 and 2034. The increasing adoption of digital transformation, cloud computing, and advanced technologies such as artificial intelligence (AI) continues to drive demand for efficient and scalable data center infrastructure. As businesses increasingly rely on data-driven operations, organizations across various industries are prioritizing the expansion and modernization of their data centers to enhance efficiency, security, and sustainability.

With rapid advancements in big data analytics, machine learning, and the Internet of Things (IoT), the need for reliable data storage, processing, and management solutions is at an all-time high. Enterprises are making substantial investments in power distribution, cooling solutions, and security systems to maintain operational continuity and prevent downtime. The rising adoption of hybrid cloud models is further fueling market expansion as businesses integrate on-premises infrastructure with cloud-based services to optimize performance and cost efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39.2 Billion |

| Forecast Value | $92.2 Billion |

| CAGR | 9.1% |

The market encompasses several infrastructure segments, including power distribution systems, cooling systems, racks and enclosures, security systems, and site and facility infrastructure. Among these, power distribution systems accounted for a 30% share in 2024, making them the most significant segment. These systems, comprising generators, uninterruptible power supplies (UPS), and power distribution units (PDUs), play a crucial role in maintaining continuous power supply within data centers. PDUs are essential for distributing electricity to various IT equipment, while UPS systems ensure that critical systems remain operational during outages. Generators act as backup power sources, offering an additional layer of reliability to prevent disruptions in data center operations. With the increasing volume of data traffic and the growing reliance on cloud services, organizations are placing greater emphasis on energy-efficient and resilient power infrastructure to support their expanding data processing needs.

The market is further segmented based on organization size, including small and medium enterprises (SME) and large enterprises. In 2024, large enterprises dominated the market with a 67% share. These companies are expanding their IT infrastructures to manage extensive data workloads and enhance processing capabilities. Investments in advanced power distribution, high-speed networking, and next-generation cooling solutions are accelerating as enterprises aim to optimize operational efficiency and minimize energy consumption. With AI, automation, and real-time data analytics gaining traction, businesses are integrating intelligent infrastructure management solutions to streamline operations and reduce costs. Hybrid cloud solutions are also reshaping the market landscape, with large enterprises leveraging a combination of on-premises data centers and cloud-based platforms to achieve greater flexibility, scalability, and data security.

North America data center support infrastructure market held a 35% share, with the U.S. being the largest contributor. In 2024, the U.S. generated USD 12 billion in revenue from data center support infrastructure, driven by strong demand for cloud computing, AI-powered applications, and digital services. As one of the most technologically advanced regions, the U.S. continues to lead the global data center industry, with hyperscale data centers and colocation facilities witnessing significant expansion. Enterprises across industries, including IT, telecom, finance, and healthcare, are heavily investing in state-of-the-art infrastructure to support their digital transformation initiatives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 AI software providers

- 3.1.2 Service providers

- 3.1.3 Data providers

- 3.1.4 System integrators

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case studies

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increased demand for cloud services

- 3.9.1.2 Rise of hyperscale and edge data centers

- 3.9.1.3 Technological advancements in data center design

- 3.9.1.4 Government initiatives and policies

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing energy consumption and environmental impact

- 3.9.2.2 Data safety and security concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Infrastructure, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Power distribution systems

- 5.3 Cooling systems

- 5.4 Racks and enclosures

- 5.5 Site and facility infrastructure

- 5.6 Security systems

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprise

Chapter 8 Market Estimates & Forecast, By Tier, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Tier I

- 8.3 Tier II

- 8.4 Tier III

- 8.5 Tier IV

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 IT & telecom

- 9.3 BFSI

- 9.4 Healthcare & life sciences

- 9.5 Government & defense

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Asetek

- 11.3 Black Box

- 11.4 Cisco Systems

- 11.5 Delta Electronics

- 11.6 Eaton

- 11.7 Fujitsu

- 11.8 Hewlett Packard Enterprise (HPE)

- 11.9 Huawei Technologies

- 11.10 IBM

- 11.11 Johnson Controls

- 11.12 Legrand

- 11.13 Mitsubishi Electric

- 11.14 Raritan

- 11.15 Rittal

- 11.16 Schneider Electric

- 11.17 Siemens

- 11.18 STULZ

- 11.19 Toshiba

- 11.20 Vertiv

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日