石油・ガスデータ管理市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Oil and Gas Data Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698274

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

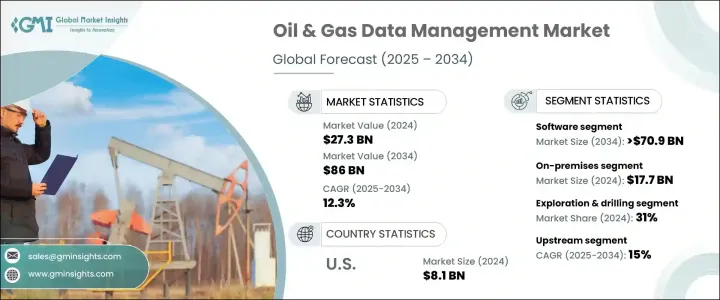

世界の石油・ガスデータ管理市場は、2024年に273億米ドルの評価額に達し、2025年から2034年にかけてCAGR 12.3%で拡大すると予測されています。

業界におけるAI、ビッグデータ、クラウドコンピューティングの急速な導入は、効率化を推進し、資産追跡を最適化し、ダウンタイムを削減しています。企業が業務強化に努める中、データ管理ソリューションの需要が急増しています。世界の厳しい規制により、効率的なデータ管理の必要性が高まっており、環境政策や安全基準の遵守を確保しつつ、法的な複雑さを防いでいます。

各国政府は、排出ガス、操業の安全性、資源利用に関する規制を強化しており、石油・ガス企業は高度なデータ報告とガバナンス・ソリューションの導入を余儀なくされています。これに対応するため、企業は排出量を追跡し、資産を監視し、進化する業界標準に準拠するための高度なソフトウェアを統合しています。デジタルトランスフォーメーションに伴い、サイバー脅威のリスクはエスカレートし続けており、企業は強固なセキュリティフレームワークへの投資を促しています。暗号化、多層認証、リアルタイムの脅威検知は、今やデータ管理システムに不可欠な機能となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 273億米ドル |

| 予測金額 | 860億米ドル |

| CAGR | 12.3% |

石油・ガスデータ管理市場はソフトウェア・ソリューションが圧倒的で、2024年の市場シェアは67%を超え、2034年には709億米ドルを超えると予想されます。AI、機械学習、ビッグデータ分析が大規模データセットの処理に導入され、予知保全、リアルタイム監視、意思決定の強化が可能になりつつあります。また、企業はクラウドベースのIoT対応プラットフォームへとシフトしており、遠隔地からのアクセスや複数拠点間でのシームレスなデータ交換を実現しています。クラウド・テクノロジーはコスト効率が高く安全なデータ・ストレージを提供し、IoTセンサーはリアルタイムの業務上の洞察を提供して効率をさらに向上させる。

オンプレミス展開は引き続き市場を独占しており、2024年には177億米ドルを占める。石油・ガス業界は、地質レポート、掘削分析、生産予測など、機密性の高いデータを扱っています。組織は、専有情報を厳格に管理し、規制コンプライアンスを確保し、サイバーセキュリティ・リスクを最小限に抑えるため、オンプレミス・ソリューションを優先しています。多くの政府がデータ主権法を施行し、オンプレミス・インフラの選好をさらに後押ししています。さらに、オフショア事業では、インターネット接続が限られているにもかかわらず、中断のない処理を保証するため、ローカライズされたデータ・ストレージに依存しています。

石油・ガスデータ管理では、探査と掘削が依然として重要なアプリケーションであり、2024年の市場シェアは31%です。これらのプロセスでは膨大な量の地質データや地震データが生成されるため、掘削精度を最適化し、リスクを最小限に抑えるための高度な管理ソリューションが必要となります。効率的な資源採掘が重視されるようになったことで、AIを活用したデータモデリングへの投資が促進され、企業は意思決定を改善し、運用上の不確実性を低減できるようになりました。世界のエネルギー需要の増加に伴い、企業は探査活動を強化し、高性能データ管理技術の必要性を煽っています。

データ管理ソリューションの導入は上流部門が業界をリードしており、2034年までのCAGRは15%と予測されています。探鉱、掘削、生産活動では膨大なデータセットが生成され、効率と炭化水素回収の強化のために高度な分析が必要となります。石油・ガス企業は探査・生産への支出を増やしており、地質マッピング、貯留層モニタリング、掘削最適化のためのデジタルツールが必要とされています。AI、IoT、ビッグデータ分析などの技術は、リアルタイムの追跡、予知保全、全体的な運用効率において重要な役割を果たしています。

北米は世界の石油・ガスデータ管理市場で最大のシェアを占め、2024年には34%を占め、米国は81億米ドルの収益を上げています。この地域は、石油・ガスのワークフローにAI、IoT、クラウド・ソリューションを統合する最前線にあります。規制機関は厳格なコンプライアンス要件を課しており、企業は排出量追跡、安全監視、リスク軽減のために高度なデータ管理システムの導入を余儀なくされています。デジタルトランスフォーメーションが加速する中、効率的なデータ管理は、業界全体のロジスティクス、保管、輸送業務の最適化に不可欠であることに変わりはないです。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- ソフトウェアベンダー

- クラウドプロバイダー

- テクノロジープロバイダー

- エンドユース

- 利益率分析

- サプライヤーの状況

- テクノロジーとイノベーションの展望

- 特許分析

- 規制状況

- 影響要因

- 促進要因

- 石油・ガス業界におけるデジタルトランスフォーメーションの拡大

- クラウドベースのソリューション採用の増加

- 予測分析とAIへのニーズの高まり

- 厳しい規制と環境コンプライアンス

- エネルギー効率とコスト最適化の需要の高まり

- 業界の潜在的リスク&課題

- 高い導入コストとレガシーシステムの統合

- サイバーセキュリティリスクとデータプライバシーへの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- ソフトウェア

- データ分析・可視化

- データ統合

- マスターデータ管理

- メタデータ管理

- その他

- サービス内容

- コンサルティング&プランニング

- 統合と実装

- サポート&メンテナンス

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 探鉱・掘削

- 生産最適化

- 精製・加工

- 輸送・貯蔵

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- アップストリーム

- ミッドストリーム

- ダウンストリーム

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Argus Media

- AVEVA Group

- Baker Hughes Company

- Cognite

- Emerson Electric

- Halliburton Energy Services

- Honeywell International

- IBM

- IMS PEI

- Infosys

- NetApp

- Oracle

- P2 Energy Solutions

- Quorum Business Solutions

- Rystad Energy

- SAP SE

- Schlumberger

- Teradata

- TGS-NOPEC Geophysical Company

- Wood Mackenzie

目次

The Global Oil And Gas Data Management Market reached a valuation of USD 27.3 billion in 2024 and is projected to expand at a CAGR of 12.3% from 2025 to 2034. The rapid adoption of AI, big data, and cloud computing in the industry is driving efficiency, optimizing asset tracking, and reducing downtime. As companies strive to enhance operations, demand for data management solutions is surging. Stringent regulations worldwide are reinforcing the need for efficient data management, ensuring compliance with environmental policies and safety standards while preventing legal complications.

Governments are tightening regulations around emissions, operational safety, and resource utilization, compelling oil and gas companies to implement advanced data reporting and governance solutions. In response, organizations are integrating sophisticated software to track emissions, monitor assets, and comply with evolving industry standards. The risk of cyber threats continues to escalate with digital transformation, prompting companies to invest in robust security frameworks. Encryption, multi-layer authentication, and real-time threat detection are now essential features in data management systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.3 Billion |

| Forecast Value | $86 Billion |

| CAGR | 12.3% |

Software solutions dominate the oil and gas data management market, holding a market share exceeding 67% in 2024, and are expected to surpass USD 70.9 billion by 2034. AI, machine learning, and big data analytics are increasingly being deployed to process large datasets, allowing predictive maintenance, real-time monitoring, and enhanced decision-making. Companies are also shifting towards cloud-based and IoT-enabled platforms, ensuring remote access and seamless data exchange across multiple locations. Cloud technology provides cost-effective and secure data storage, while IoT sensors offer real-time operational insights, further improving efficiency.

On-premises deployment continues to dominate the market, accounting for USD 17.7 billion in 2024. The oil and gas industry handles highly sensitive data, including geological reports, drilling analytics, and production forecasts. Organizations prioritize on-premises solutions to maintain strict control over proprietary information, ensuring regulatory compliance and minimizing cybersecurity risks. Many governments enforce data sovereignty laws, further driving the preference for on-premises infrastructure. Additionally, offshore operations rely on localized data storage to ensure uninterrupted processing despite limited internet connectivity.

Exploration and drilling remain critical applications within oil and gas data management, holding a 31% market share in 2024. These processes generate vast amounts of geological and seismic data, necessitating advanced management solutions to optimize drilling accuracy and minimize risks. The growing emphasis on efficient resource extraction has driven investments in AI-powered data modeling, enabling companies to improve decision-making and reduce operational uncertainties. As global energy demand rises, firms are intensifying exploration efforts, fueling the need for high-performance data management technologies.

The upstream sector leads the industry's adoption of data management solutions and is projected to grow at a CAGR of 15% through 2034. Exploration, drilling, and production activities generate extensive datasets that require sophisticated analytics for enhanced efficiency and hydrocarbon recovery. Oil and gas companies are ramping up spending on exploration and production, necessitating digital tools for geological mapping, reservoir monitoring, and drilling optimization. Technologies such as AI, IoT, and big data analytics play a crucial role in real-time tracking, predictive maintenance, and overall operational efficiency.

North America holds the largest share of the global oil and gas data management market, accounting for 34% in 2024, with the U.S. generating USD 8.1 billion in revenue. The region is at the forefront of integrating AI, IoT, and cloud solutions into oil and gas workflows. Regulatory bodies enforce strict compliance requirements, compelling companies to adopt advanced data management systems for emissions tracking, safety monitoring, and risk mitigation. As digital transformation accelerates, efficient data management remains essential for optimizing logistics, storage, and transportation operations across the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Software vendors

- 3.1.1.2 Cloud providers

- 3.1.1.3 Technology providers

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Growing digital transformation in the oil & gas industry

- 3.5.1.2 Increasing adoption of cloud-based solutions

- 3.5.1.3 Rising need for predictive analytics and ai

- 3.5.1.4 Stringent regulatory and environmental compliance

- 3.5.1.5 Rising demand for energy efficiency and cost optimization

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High implementation costs and legacy system integration

- 3.5.2.2 Cybersecurity risks and data privacy concerns

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Data analytics & visualization

- 5.2.2 Data integration

- 5.2.3 Master data management

- 5.2.4 Metadata management

- 5.2.5 Others

- 5.3 Services

- 5.3.1 Consulting & planning

- 5.3.2 Integration & implementation

- 5.3.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud based

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Exploration & drilling

- 7.3 Production optimization

- 7.4 Refining & processing

- 7.5 Transport & storage

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Upstream

- 8.3 Midstream

- 8.4 Downstream

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Argus Media

- 10.2 AVEVA Group

- 10.3 Baker Hughes Company

- 10.4 Cognite

- 10.5 Emerson Electric

- 10.6 Halliburton Energy Services

- 10.7 Honeywell International

- 10.8 IBM

- 10.9 IMS PEI

- 10.10 Infosys

- 10.11 NetApp

- 10.12 Oracle

- 10.13 P2 Energy Solutions

- 10.14 Quorum Business Solutions

- 10.15 Rystad Energy

- 10.16 SAP SE

- 10.17 Schlumberger

- 10.18 Teradata

- 10.19 TGS-NOPEC Geophysical Company

- 10.20 Wood Mackenzie

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日