石油・ガスにおけるクラウドコンピューティングの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Cloud Computing in Oil and Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665232

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

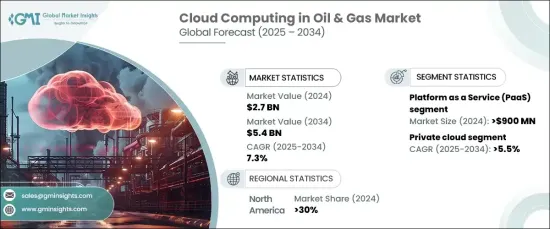

石油・ガスにおけるクラウドコンピューティングの世界市場規模は、2024年に27億米ドルとなり、2025~2034年にかけてCAGR 7.3%で力強い成長が見込まれています。

この成長の背景には、業務の俊敏性、ワークフローの最適化、データアクセスの強化に対するニーズの高まりがあります。石油・ガス企業が業務の近代化に努めるなか、クラウド技術を統合することで柔軟性が向上し、市場の変動への迅速な対応やより効率的なリソース管理が可能になります。

2024年、市場は、IaaS(Infrastructure-as-a-Service)、PaaS(Platform-as-a-Service)、SaaS(Software-as-a-Service)に区別されます。このうち、PaaSの市場シェアは9億米ドル(約9,000億円)と突出しています。このセグメントは、アプリケーションの開発と管理を簡素化し、基盤となるインフラを維持する複雑さを解消できることから、急速に拡大しています。PaaSソリューションを採用することで、石油・ガス企業は開発を効率化し、市場開拓までの時間を短縮し、需要に応じてリソースを容易に拡大することができます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 27億米ドル |

| 予測金額 | 54億米ドル |

| CAGR | 7.3% |

石油・ガスにおけるクラウドコンピューティングは、パブリック、プライベート、ハイブリッドクラウドソリューションなど、展開モードによっても区分されます。プライベートクラウドセグメントは、2025~2034年にかけてCAGR 5.5%で安定した成長が見込まれています。この成長を牽引しているのは、機密データを扱う企業にとって重要なセキュリティ機能を強化したプライベートクラウドソリューションの採用が増加していることです。プライベートクラウドの導入により、石油・ガス企業は、クラウド技術の拡大性と柔軟性の恩恵を受けながら、データプライバシーの管理を強化することができます。これは、厳格な規制基準の遵守が譲れない産業では特に重要です。

米国では、石油・ガスにおけるクラウドコンピューティング市場は2024年に30%のシェアを獲得します。この地域全体でクラウド技術が広く採用されているため、業務効率が大幅に向上し、コストが削減されています。米国の大手石油・ガス企業は、デジタルトランスフォーメーション戦略の一環として、クラウドインフラに多額の投資を行っています。さらに、同地域の強力な規制枠組みと先進的データ分析ソリューションに対する需要の高まりが、探査から流通まで幅広い石油・ガスにおけるクラウドコンピューティングの統合を加速させています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- ソフトウェアプロバイダー

- サービスプロバイダー

- 石油・ガス事業者

- 流通業者

- エンドユーザー

- 利益率分析

- 技術革新の状況

- 特許分析

- 規制状況

- 使用事例

- 使用事例1

- メリット

- 投資収益率

- 使用事例2

- 利益

- 投資利益率

- 使用事例1

- 使用事例

- 使用事例1

- 消費者名

- 課題

- 解決策

- インパクト

- 使用事例2

- 消費者名

- 課題

- 解決策

- インパクト

- 使用事例1

- 影響要因

- 促進要因

- リアルタイムのデータ分析とモニタリングに対する需要の高まり

- データ洞察による持続可能性の向上と環境負荷の低減へのシフト

- クラウドベースのソリューションによる業務効率の向上

- 石油・ガスセクターにおけるデジタルトランスフォーメーションへの取り組みへの注目の高まり

- 産業の潜在的リスク・課題

- レガシーシステムとの統合の課題

- データプライバシーとサイバーセキュリティの脅威に関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:サービス別、2021~2034年

- 主要動向

- IaaS(Infrastructure-as-a-Servic)

- PaaS(Platform-as-a-Service)

- SaaS(Software-as-a-Service)

第6章 市場推定・予測:展開モード別、2021~2034年

- 主要動向

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

第7章 市場推定・予測:運用別、2021~2034年

- 主要動向

- 上流

- 中流

- 下流

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- データ保管・管理

- 資産管理

- コラボレーション・コミュニケーションツール

- 遠隔モニタリング・制御

- シミュレーションとモデリング

- その他

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 国営石油会社(NOC)

- 独立系石油会社(IOC)

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- ABB

- Accenture

- Amazon Web Services(AWS)

- AVEVA

- Baker Hughes

- Cisco

- Dassault Systemes

- General Electric

- Halliburton

- Honeywell

- IBM

- Intel

- Microsoft

- Oracle

- Rockwell Automation

- SAP

- Schlumberger

- Siemens Energy

- Tata Consultancy Services(TCS)

- Yokogawa

目次

The Global Cloud Computing In Oil And Gas Market was valued at USD 2.7 billion in 2024 and is expected to experience robust growth at a CAGR of 7.3% from 2025 to 2034. This growth is fueled by the increasing need for operational agility, optimized workflows, and enhanced data access. As oil and gas companies strive to modernize their operations, integrating cloud technologies offers increased flexibility, enabling faster responses to market fluctuations and more efficient resource management.

In 2024, the market was divided into several key service offerings: Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). Among these, the PaaS segment commanded a substantial market share, valued at USD 900 million. This segment is expanding rapidly due to its ability to simplify application development and management, eliminating the complexities of maintaining underlying infrastructure. By adopting PaaS solutions, oil and gas companies can streamline development, reduce time to market, and easily scale their resources according to demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 7.3% |

Cloud computing in the oil and gas sector is also segmented by deployment mode, including public, private, and hybrid cloud solutions. The private cloud segment is expected to grow steadily at a CAGR of 5.5% from 2025 to 2034. This growth is driven by the rising adoption of private cloud solutions, which offer enhanced security features crucial for companies handling sensitive data. With private cloud deployments, oil and gas firms can enjoy greater control over data privacy while benefiting from the scalability and flexibility of cloud technologies. This is particularly important in an industry where compliance with stringent regulatory standards is non-negotiable.

In the U.S., the cloud computing market for oil and gas captured a 30% share in 2024. The widespread adoption of cloud technologies across the region is significantly boosting operational efficiency and reducing costs. Major oil and gas companies in the U.S. are investing heavily in cloud infrastructure as part of their digital transformation strategies. Furthermore, the region's strong regulatory framework and increasing demand for advanced data analytics solutions are accelerating the integration of cloud computing across a wide range of oil and gas operations, from exploration to distribution.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software providers

- 3.2.2 Service providers

- 3.2.3 Oil & gas operators

- 3.2.4 Distributors

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Used cases

- 3.7.1 Used case 1

- 3.7.1.1 Benefits

- 3.7.1.2 ROI

- 3.7.2 Used case 2

- 3.7.2.1 Benefits

- 3.7.2.2 ROI

- 3.7.1 Used case 1

- 3.8 Case study

- 3.8.1 Case study 1

- 3.8.1.1 Consumer name

- 3.8.1.2 Challenge

- 3.8.1.3 Solution

- 3.8.1.4 Impact

- 3.8.2 Case study 2

- 3.8.2.1 Consumer name

- 3.8.2.2 Challenge

- 3.8.2.3 Solution

- 3.8.2.4 Impact

- 3.8.1 Case study 1

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for real-time data analytics and monitoring

- 3.9.1.2 Shift towards improving sustainability and reducing environmental impact through data insights

- 3.9.1.3 Enhanced operational efficiency through cloud-based solutions

- 3.9.1.4 Growing focus on digital transformation initiatives in the oil and gas sector

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Integration challenges with legacy systems

- 3.9.2.2 Concerns regarding data privacy and cybersecurity threats

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Infrastructure as a Service (IaaS)

- 5.3 Platform as a Service (PaaS)

- 5.4 Software as a Service (SaaS)

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Public cloud

- 6.3 Private cloud

- 6.4 Hybrid cloud

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Upstream

- 7.3 Midstream

- 7.4 Downstream

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Data storage and management

- 8.3 Asset management

- 8.4 Collaboration and communication tools

- 8.5 Remote monitoring and control

- 8.6 Simulation and modeling

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 National Oil Companies (NOCs)

- 9.3 Independent Oil Companies (IOCs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Accenture

- 11.3 Amazon Web Services (AWS)

- 11.4 AVEVA

- 11.5 Baker Hughes

- 11.6 Cisco

- 11.7 Dassault Systèmes

- 11.8 General Electric

- 11.9 Halliburton

- 11.10 Honeywell

- 11.11 IBM

- 11.12 Intel

- 11.13 Microsoft

- 11.14 Oracle

- 11.15 Rockwell Automation

- 11.16 SAP

- 11.17 Schlumberger

- 11.18 Siemens Energy

- 11.19 Tata Consultancy Services (TCS)

- 11.20 Yokogawa

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 165 Pages

- 納期

- 2~3営業日