ヘルスケアバイオコンバージェンス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Healthcare Bioconvergence Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698266

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

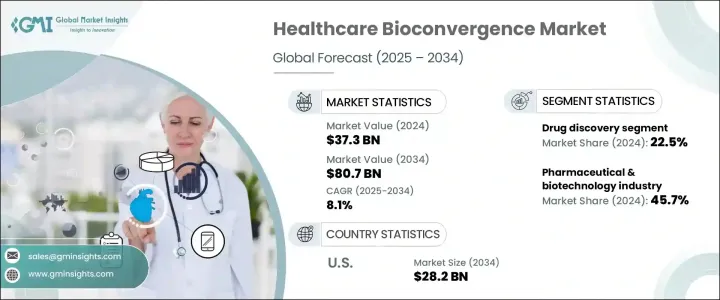

世界のヘルスケアバイオコンバージェンス市場は2024年に373億米ドルに達し、2025年から2034年にかけてCAGR 8.1%で成長すると予測されています。

急速に発展するこの市場は、コンピューターサイエンス、人工知能(AI)、エンジニアリング、バイオテクノロジーなどの最先端技術を統合することで、ヘルスケアの未来を再定義しています。ライフサイエンスとテクノロジーのギャップを埋めることで、バイオコンバージェンスは医療研究、診断、治療の個別化におけるイノベーションを加速させています。

慢性疾患の蔓延、人口の高齢化、治療費の高騰により、世界中のヘルスケア・システムが大きなプレッシャーに直面する中、高度なデータ主導型ソリューションへの需要が急増しています。個別化医療、再生療法、AI主導型診断の推進がこの分野への投資をさらに促進しており、バイオコンバージェンスは現代ヘルスケアの重要な柱となっています。さらに、大手製薬会社やバイオテクノロジー企業は、画期的なソリューションを開発するために技術主導の新興企業と協力しており、ますます競合情勢が激化しています。バイオエレクトロニクス、オプトジェネティクス、ナノロボティクスの採用拡大により、ヘルスケアの変革が進み、患者の転帰が改善され、医療介入が最適化されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 373億米ドル |

| 予測金額 | 807億米ドル |

| CAGR | 8.1% |

市場は、創薬、ドラッグデリバリー用ナノロボティクス、再生医療、精密医療など、さまざまな用途に区分されます。2024年には、創薬が22.5%と最大のシェアを占め、世界のヘルスケアコストの増加、慢性疾患の蔓延の増加、主要薬剤の特許切れなどがその要因となっています。製薬会社は、創薬を強化し、研究期間を短縮し、コストを削減するために、AIを搭載したツールを急速に統合しています。ドラッグデリバリーのためのナノロボティクスは、標的薬物送達を改善し、副作用を最小限に抑える能力があることから、予測期間を通じて最も速い成長が見込まれます。バイオエレクトロニクスやオプトジェネティクスといった他の革新的アプリケーションも勢いを増しており、神経治療、視力回復、慢性疾患管理における新たな可能性を引き出しています。

製薬企業とバイオテクノロジー企業は、2024年のヘルスケアバイオコンバージェンス市場の45.7%を占め、主要エンドユーザーとしての地位を固めています。これらの業界は、研究イニシアチブを推進し、資金を確保し、ヘルスケアの意思決定に影響を与える上で重要な役割を果たしています。製薬大手はバイオコンバージェンスを活用して業務効率を改善し、臨床試験を合理化し、次世代治療法を開発しています。また、多くの企業が健康データを研究拡張に活用したり、転売することで収益化しています。製薬企業やバイオテクノロジー企業と並んで、医薬品開発業務受託機関(CRO)やヘルスケアプロバイダーも市場拡大に貢献しており、病院や研究機関はAIを活用したバイオコンバージェンス・プラットフォームを採用して精密医療の進歩を推進しています。

米国ヘルスケアバイオコンバージェンス市場は2024年に142億米ドルを生み出し、AIを活用した診断技術への継続的な投資により、2034年には282億米ドルに達すると予測されています。大手病院、研究センター、バイオテクノロジー企業は、遺伝子、環境、ライフスタイルのデータを分析し、高度にカスタマイズされた治療戦略を作成するために、AI駆動型プラットフォームの採用を増やしています。デジタルヘルスソリューション、予測分析、AI支援臨床意思決定の統合が進む中、米国はヘルスケアバイオコンバージェンス革新の最前線にあり続け、長期的な市場成長を確実なものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 個別化治療に対する意識の高まり

- 新たな治療分野への応用

- 製薬・バイオテクノロジー分野における研究開発費の増加

- ヘルスケア業界におけるロボット工学のダイナミックな導入

- 業界の潜在的リスク&課題

- 個別化治療に関する長期データの不足

- 精密医療、再生医療、創薬に対する厳しい規制

- 促進要因

- 成長可能性分析

- 技術的展望

- 規制状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 創薬

- ドラッグデリバリー用ナノロボティクス

- 再生医療

- 診断・生体センサー

- バイオエレクトロニクス

- 人工生体材料

- オプトジェネティクス

- 精密医療

- その他の用途

第6章 市場推計・予測:最終用途別、2021年~2034年

- 製薬・バイオテクノロジー産業

- CRO(医薬品開発業務受託機関)

- その他の最終用途

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Anima Biotech

- BICO-The Bio Convergence Company

- BioConvergent Health

- Biomx

- Century Therapeutics

- Cytena

- Galvani Bioelectronics

- GE Healthcare

- Ginkgo Bioworks

- Merck

- Pangea Biomed

- Setpoint Medical Corporation

- Singota Solution

- Thermo Fisher Scientific

- Zymergen

目次

The Global Healthcare Bioconvergence Market reached USD 37.3 billion in 2024 and is expected to grow at a CAGR of 8.1% between 2025 and 2034. This rapidly evolving market is redefining the future of healthcare by integrating cutting-edge technologies such as computer science, artificial intelligence (AI), engineering, and biotechnology. By bridging the gap between life sciences and technology, bioconvergence is accelerating innovations in medical research, diagnostics, and treatment personalization.

As healthcare systems worldwide face increasing pressure due to rising chronic disease prevalence, aging populations, and escalating treatment costs, the demand for advanced, data-driven solutions is surging. The push for personalized medicine, regenerative therapies, and AI-driven diagnostics is further driving investments in this sector, making bioconvergence a key pillar of modern healthcare. Additionally, major pharmaceutical and biotechnology firms are collaborating with tech-driven startups to develop groundbreaking solutions, creating an increasingly competitive landscape. The growing adoption of bioelectronics, optogenetics, and nanorobotics is set to transform healthcare, enhancing patient outcomes and optimizing medical interventions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.3 Billion |

| Forecast Value | $80.7 Billion |

| CAGR | 8.1% |

The market is segmented into various applications, including drug discovery, nanorobotics for drug delivery, regenerative medicine, and precision medicine, among others. In 2024, drug discovery held the largest share at 22.5%, fueled by increasing global healthcare costs, the rising prevalence of chronic illnesses, and the expiration of key drug patents. Pharmaceutical companies are rapidly integrating AI-powered tools to enhance drug discovery, reduce research timelines, and cut costs. Nanorobotics for drug delivery is anticipated to experience the fastest growth throughout the forecast period, given its ability to improve targeted drug delivery and minimize adverse effects. Other innovative applications, such as bioelectronics and optogenetics, are also gaining momentum, unlocking new possibilities in neurological treatments, vision restoration, and chronic disease management.

Pharmaceutical and biotechnology companies accounted for 45.7% of the healthcare bioconvergence market in 2024, solidifying their position as the leading end-users. These industries play a crucial role in advancing research initiatives, securing funding, and influencing healthcare decision-making. Pharma giants are leveraging bioconvergence to improve operational efficiencies, streamline clinical trials, and develop next-generation therapies. Many companies are also monetizing health data by utilizing it for research expansion or reselling it to generate additional revenue. Alongside pharmaceutical and biotech firms, contract research organizations (CROs) and healthcare providers are also contributing to market expansion, with hospitals and research institutions adopting AI-powered bioconvergent platforms to drive precision medicine advancements.

The U.S. Healthcare Bioconvergence Market generated USD 14.2 billion in 2024 and is projected to reach USD 28.2 billion by 2034, driven by continuous investments in AI-powered diagnostic technologies. Leading hospitals, research centers, and biotech firms are increasingly adopting AI-driven platforms to analyze genetic, environmental, and lifestyle data, creating highly customized treatment strategies. With the rising integration of digital health solutions, predictive analytics, and AI-assisted clinical decision-making, the U.S. remains at the forefront of healthcare bioconvergence innovation, ensuring long-term market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing awareness towards personalized treatment

- 3.2.1.2 Emerging applications in new therapeutic areas

- 3.2.1.3 Growing R&D expenditure in pharma-biotech sector

- 3.2.1.4 Dynamic adoption of robotics in healthcare industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of long-term data for personalized treatments

- 3.2.2.2 Stringent regulations towards precision medicine, regenerative medicines and drug discovery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological landscape

- 3.5 Regulatory landscape

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Drug discovery

- 5.3 Nanorobotics for drug delivery

- 5.4 Regenerative medicine

- 5.5 Diagnostic and biological sensors

- 5.6 Bioelectronics

- 5.7 Engineered living materials

- 5.8 Optogenetics

- 5.9 Precision medicine

- 5.10 Other applications

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Bn)

- 6.1 Pharmaceutical & biotechnology industry

- 6.2 Contract research organization (CRO)

- 6.3 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Bn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Anima Biotech

- 8.2 BICO - The Bio Convergence Company

- 8.3 BioConvergent Health

- 8.4 Biomx

- 8.5 Century Therapeutics

- 8.6 Cytena

- 8.7 Galvani Bioelectronics

- 8.8 GE Healthcare

- 8.9 Ginkgo Bioworks

- 8.10 Merck

- 8.11 Pangea Biomed

- 8.12 Setpoint Medical Corporation

- 8.13 Singota Solution

- 8.14 Thermo Fisher Scientific

- 8.15 Zymergen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日