|

市場調査レポート

商品コード

1928912

自動運転車市場の機会、成長促進要因、業界動向分析、予測(2026年~2035年)Self-driving Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動運転車市場の機会、成長促進要因、業界動向分析、予測(2026年~2035年) |

|

出版日: 2026年01月09日

発行: Global Market Insights Inc.

ページ情報: 英文 245 Pages

納期: 2~3営業日

|

概要

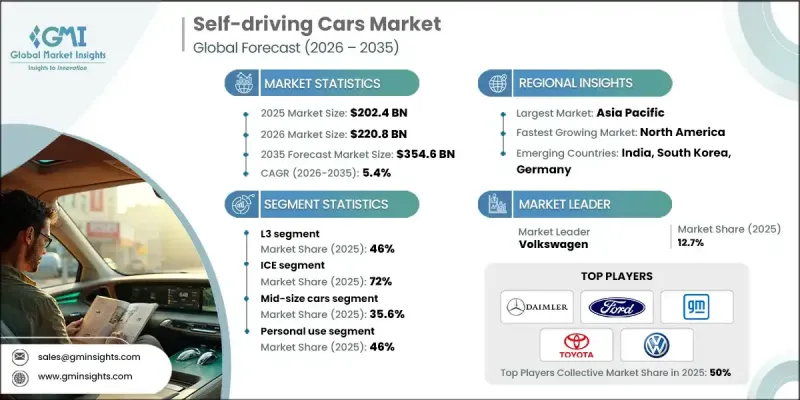

世界の自動運転車市場は、2025年に2,024億米ドルと評価され、2035年までにCAGR5.4%で成長し、3,546億米ドルに達すると予測されています。

交通関連のリスク最小化と移動効率の向上への関心の高まりが、導入を加速し続けております。制御された試験と早期導入を支援する規制枠組みが、自律技術の新たな商業化機会を開いています。人工知能、センシングシステム、高性能コンピューティングの進歩により、システムの信頼性と実環境での性能が向上しています。自律走行車とインテリジェント都市インフラの統合は、コネクテッド交通プラットフォーム、車両とインフラ間の通信、適応型経路設定機能を通じて市場の勢いを強化しています。これらの技術は交通流を改善し、渋滞レベルを低下させ、エネルギー消費の削減を支援しています。自律移動プラットフォームの拡大は、都市交通の経済性を再構築し、車両群の効率性を向上させると同時に、拡張可能な自動化輸送モデルを実現することで、さらなる成長を支えています。自律移動サービスプラットフォーム市場は、自動化に焦点を当てたシステムの導入後、車両群運営者が少なくとも30%の運用コスト削減を報告していることから、拡大を続けています。これらのプラットフォームは商業的に実行可能かつ拡張性があることが実証され、自動化輸送サービスに対する長期的な信頼を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 2,024億米ドル |

| 予測金額 | 3,546億米ドル |

| CAGR | 5.4% |

レベル3自動運転セグメントは2025年に46%のシェアを占め、2026年から2035年にかけてCAGR5.2%で成長すると予測されています。レベル3車両は運転タスクからの部分的な解放を可能としつつ運転者の準備態勢を確保するため、複数の車両カテゴリーで広く採用されています。自動運転開発プログラムの相当部分が引き続きレベル3機能に焦点を当てていることから、持続的な需要が見込まれます。

内燃機関車両セグメントは2025年に72%のシェアを占め、2035年までCAGR 4.8%で成長すると見込まれています。これらの車両は確立された製造プラットフォームの恩恵を受け、自動化統合を簡素化します。電気自動運転車両は、ソフトウェア駆動型アーキテクチャ、高度なセンサーアレイ、集中型コンピューティングシステムとの互換性により第2位のセグメントを占めていますが、内燃機関プラットフォームは機械的性能特性により大きく依存しています。

米国自動運転車市場は2025年に83%のシェアを占め、336億米ドルの市場規模を生み出しました。活発な投資活動、有利な政策イニシアチブ、加速する商用展開により、同国は自動運転車開発と長期的な市場成長の中核拠点としての地位を維持し続けています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 道路安全と事故削減

- 人工知能とセンサー技術の進歩

- 政府による試験承認と規制

- 自動運転モビリティサービスの成長

- 業界の潜在的リスク&課題

- 開発および検証コストの高さ

- 地域ごとの規制の不確実性

- 市場機会

- ロボタクシーおよび自動運転車両サービスの拡大

- 自律型物流および貨物輸送

- スマートシティインフラとの統合

- 成長可能性分析

- 規制情勢

- 北米

- 米国国家道路交通安全局(NHTSA)自動運転車向けFMVSS更新

- 米国運輸省(DOT)自動運転車両包括計画(AVCP)

- 州レベルの自動運転試験許可(カリフォルニア州DMV及びネバダ州DMVガイドライン)

- カナダ運輸省自動運転システム(ADS)試験ガイドライン

- 欧州

- 自動車線維持システム(ALKS)に関する国連欧州経済委員会規則第157号

- 欧州連合(EU)自動運転システム(ADS)型式認証に関する一般安全規制(GSR)

- ドイツ連邦自動車運輸局(KBA)レベル4運転許可

- 英国自動運転車法および責任枠組み

- アジア太平洋地域

- 中華人民共和国工業情報化部(MIIT)ICV市場参入ガイド

- 国土交通省(MLIT)レベル4ライセンシング

- 韓国国土交通省(MOLIT)自動運転車商用化安全基準

- 自動運転車に関するシンガポール技術基準68(TR 68)

- インド道路運輸・高速道路省(MoRTH)新興ADASガイドライン

- ラテンアメリカ

- ブラジル国家交通評議会(CONTRAN)による運転支援に関する決議

- メキシコ移動・道路安全基本法(LGMSV)が自動化に与える影響

- チリ運輸省による自動運転パイロット試験に関する規制

- 国連自動車規制調和世界フォーラム(WP.29)との地域連携

- 中東・アフリカ

- UAE道路交通局(RTA)自律走行輸送規制

- サウジアラビアSASO電気自動車および自動運転車向け技術基準

- イスラエル運輸省自動運転車両試験実施ガイドライン

- 南アフリカにおける高度道路交通システム(ITS)導入の基準

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 自動運転システムアーキテクチャとソフトウェアスタック

- 自動運転システムアーキテクチャとスタック分析

- コンピューティング、センサー、ソフトウェアのオーケストレーションモデル

- 自律走行ソフトウェア、AI及びデータ・フライホイール

- 検証、テスト及び安全性保証フレームワーク

- 自動運転車のビジネスモデルと収益化

- 高精度マッピング、V2Xおよびインフラ依存性

- 消費者の信頼と普及の障壁

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:自律性レベル別、2022-2035

- レベル1

- レベル2

- レベル3

- レベル4

- レベル5

第6章 市場推計・予測:推進別、2022-2035

- 内燃機関(ICE)

- 電気式

- ハイブリッド車

第7章 市場推計・予測:技術別、2022-2035

- カメラベースシステム

- レーダーベースシステム

- LiDARベースのシステム

- センサフュージョンシステム

第8章 市場推計・予測:車両別、2022-2035

- コンパクトカー

- 中型車

- SUVおよび高級車

第9章 市場推計・予測:用途別、2022-2035

- 個人利用

- シェアードモビリティ

- 物流・配送

- 公共輸送機関

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第11章 企業プロファイル

- 世界プレイヤー

- BMW

- Daimler(Mercedes-Benz)

- Ford Motor Company

- General Motors(GM)

- Honda Motor

- Hyundai Motor

- Stellantis

- Tesla

- Toyota Motor

- Volkswagen

- 地域プレイヤー

- BYD

- Geely

- Renault-Nissan-Mitsubishi Alliance

- SAIC Motor

- Tata Motors

- 新興プレイヤー/ディスラプター

- Aurora Innovation

- Baidu

- NIO

- Waymo

- XPeng Motors