|

市場調査レポート

商品コード

1998682

アトピー性皮膚炎治療薬市場:市場機会、成長要因、業界動向分析、および2026年~2035年の予測Atopic Dermatitis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| アトピー性皮膚炎治療薬市場:市場機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年03月12日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

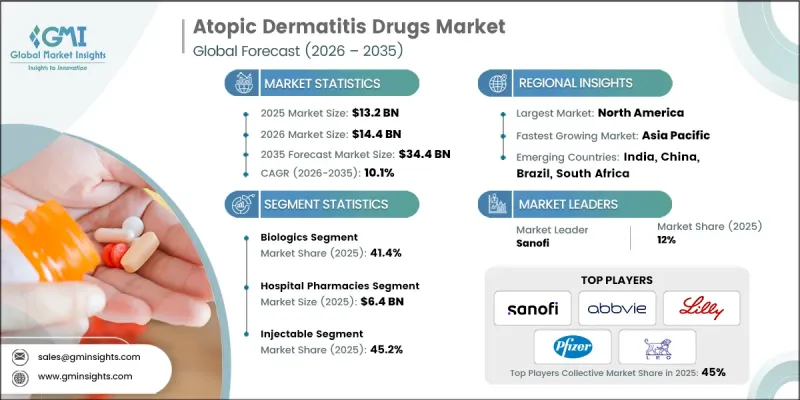

世界のアトピー性皮膚炎治療薬市場は、2025年に132億米ドルと評価され、2035年までにCAGR 10.1%で成長し、344億米ドルに達すると推定されています。

アトピー性皮膚炎治療薬市場は、この慢性炎症性皮膚疾患の世界の有病率の増加と、革新的な治療法の急速な開発に牽引され、力強い拡大を遂げています。アトピー性皮膚炎は小児および成人の両方の層において、ますます多くの人々に影響を及ぼし続けており、効果的な長期治療ソリューションに対する持続的な需要を生み出しています。製薬各社は、症状のコントロールと疾患管理の改善を実現できる先進的な治療法を導入するため、研究開発に積極的に投資しています。皮膚科治療における継続的なイノベーションにより、利用可能な治療アプローチの幅が広がり、医師は個々の患者のニーズに合わせて治療戦略を調整できるようになっています。さらに、新たな局所療法や全身療法が登場し、軽度、中等度、重度の各病期における治療枠組みの変革に寄与しています。新しい治療法が臨床現場で広く受け入れられ、実臨床において良好な長期的な治療成績を示していることから、その採用は増加し続けています。多様な治療薬の分類や投与経路が利用可能になりつつあることは、治療環境の強化に寄与しており、今後数年にわたりアトピー性皮膚炎治療薬市場の持続的な成長を支えると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 132億米ドル |

| 予測額 | 344億米ドル |

| CAGR | 10.1% |

アトピー性皮膚炎治療薬は、炎症、持続的なかゆみ、乾燥を特徴とする慢性皮膚疾患であるアトピー性皮膚炎の症状と進行を管理するために開発された医薬品です。これらの薬剤は、炎症反応を軽減し、症状の悪化に伴う不快感を和らげ、長期的に健康な皮膚状態を維持することを目的としています。治療アプローチは、標的を絞った治療メカニズムを通じて、症状のコントロール、疾患の再発予防、および長期的な疾患管理を支援するように設計されています。

2025年には、バイオロジクス部門が41.4%のシェアを占めました。バイオロジクス療法は、アトピー性皮膚炎に関連する特定の炎症経路に対して高度に標的を絞った介入を行うため、中等度から重度の病状を抱える患者にとって重要な治療選択肢となっています。これらの療法は、慢性炎症に関与する主要な免疫シグナル伝達分子を選択的に調節することで作用します。その結果、生物学的製剤は持続的な症状のコントロールを実現し、疾患の再発頻度を低減させ、皮膚の健康状態と患者の生活の質を大幅に改善することができます。免疫系を広く抑制するのではなく、炎症の正確な分子的要因を標的とするその能力は、臨床的有効性を強化すると同時に、継続的な治療を必要とする患者にとって良好な長期的な安全性を支えています。

2025年には、注射剤セグメントが45.2%のシェアを占めました。このセグメントの成長は、疾患の進行に関与する特定の炎症経路の調節に焦点を当てた、先進的な注射剤療法の利用可能性が高まっていることと密接に関連しています。標的を絞った治療選択肢の拡大は、中等度から重度の症状を有する患者における注射剤の採用に大きく寄与しています。さらに、主要な医薬品市場における規制当局は、アトピー性皮膚炎の管理を目的とした複数の注射剤療法を承認しています。これらの規制当局による承認は、新しい治療法の臨床現場への導入を加速させ、ヘルスケア従事者がより幅広い効果的な治療選択肢を利用できるようにし、ヘルスケアシステム全体での採用を促進しています。

北米のアトピー性皮膚炎治療薬市場は、2025年に大きなシェアを占めました。同地域は、高度な皮膚科医療インフラ、最新の治療選択肢への高いアクセス性、そして生物学的製剤や標的免疫調節薬を含む革新的な治療法の急速な導入により、強固な地位を維持しています。地域全体で確立された規制枠組みにより、高い臨床的安全基準を維持しつつ、新しい皮膚科治療法の一貫した評価と承認が保証されています。同地域の市場における主導的地位を支える主な要因は、人口におけるアトピー性皮膚炎の有病率の高さであり、これが先進的な治療ソリューションへの需要を牽引し続けています。中等度から重度の病状を抱える患者は、より効果的な症状のコントロールと長期的な疾患管理を可能にする新しい治療選択肢をますます求めており、これが同地域の市場見通しをさらに強固なものにしています。

よくあるご質問

目次

第1章 調査手法

- 調査アプローチ

- 品質に関する取り組み

- GMI AIポリシーおよびデータ完全性に関する取り組み

- 情報源の一貫性に関するプロトコル

- GMI AIポリシーおよびデータ完全性に関する取り組み

- 調査の経緯と信頼度スコアリング

- 調査の経緯の構成要素

- スコアリングの構成要素

- データ収集

- 一次情報の一部リスト

- データマイニング情報源

- 有料情報源

- 地域別情報源

- 有料情報源

- 基本推定および算出方法

- 各アプローチにおける基準年の算出

- 予測モデル

- 定量化された市場影響分析

- 成長パラメータが予測に与える数学的影響

- 定量化された市場影響分析

- 調査の透明性に関する補足

- 情報源の帰属フレームワーク

- 品質保証指標

- 信頼への取り組み

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- アトピー性皮膚炎の有病率の増加

- 生物学的製剤療法の進展

- 皮膚科医療への認識の高まりとアクセス拡大

- 臨床パイプラインの強化

- 業界の潜在的リスク&課題

- 生物学的製剤および先進的治療法の高コスト

- 副作用および服薬遵守の問題

- 市場機会

- 外用薬のイノベーションと非ステロイド系療法の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術動向(1次調査に基づく)

- 現在の技術

- 新興技術

- 将来の市場動向(1次調査に基づく)

- パイプライン分析(1次調査に基づく)

- AIおよび生成AIが市場に与える影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業のマトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:薬剤クラス別、2022-2035

- コルチコステロイド

- カルシニューリン阻害薬

- バイオ医薬品

- ホスホジエステラーゼ-4(PDE-4)阻害剤

- その他の薬剤分類

第6章 市場推計・予測:投与経路別、2022-2035

- 外用

- 経口

- 注射剤

第7章 市場推計・予測:患者層別、2022-2035

- 小児

- 成人

第8章 市場推計・予測:流通チャネル別、2022-2035

- 病院薬局

- 小売薬局

- Eコマース

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AbbVie

- Arcutis Biotherapeutics

- Chugai Pharmaceutical

- Eli Lilly and Company

- Galderma Laboratories

- Incyte Corporation

- Leo Pharma

- Maruho

- Otsuka Pharmaceutical

- Pfizer

- Sanofi

- Viatris