|

市場調査レポート

商品コード

1998678

獣医EHR市場の機会、成長促進要因、業界動向分析、予測、2026年~2035年Veterinary EHR Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 獣医EHR市場の機会、成長促進要因、業界動向分析、予測、2026年~2035年 |

|

出版日: 2026年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

概要

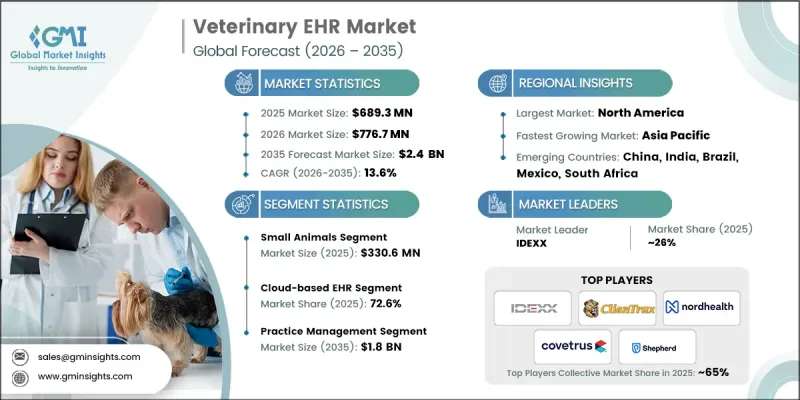

世界の獣医EHR市場は、2025年に6億8,930万米ドルと評価され、CAGR13.6%で成長し、2035年までに24億米ドルに達すると推定されています。

動物病院や診療所が業務効率と患者ケアの向上を図るため、デジタル技術の導入を加速させていることから、獣医EHR市場は強い勢いを見せています。動物の予防医療への関心の高まり、飼い主とのコミュニケーションの強化、遠隔診療機能の充実により、動物病院は記録管理システムの近代化を推進しています。デジタルソリューションへの移行により、動物病院は大量の臨床情報をより効率的に管理できると同時に、獣医療チームと飼い主との連携も改善されます。発展途上地域におけるデジタルプラットフォームの利用拡大も業界の成長を支えており、獣医療従事者は診療管理を効率化するソフトウェアベースのツールへのアクセスをより容易に得ています。同時に、診断機器の統合、画像診断機器との連携、および財務処理ソリューションに向けたソフトウェア開発への継続的な投資により、獣医EHRプラットフォームの技術的能力が強化されています。クラウドベースの技術の進歩や、獣医療システム間の相互運用性の向上も、診療所が患者データをより効果的に管理するのに役立っています。動物の健康とウェルネスに対する意識の高まりは、デジタル記録システムの導入拡大にさらに寄与しており、世界の獣医EHR市場の長期的な拡大を支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年 | 2026年~2035年 |

| 開始金額 | 6億8,930万米ドル |

| 予測金額 | 24億米ドル |

| CAGR | 13.6% |

獣医用電子健康記録(EHR)システムは、動物の健康情報を保存・管理すると同時に、獣医療施設内の臨床業務を支援するために設計されたデジタルプラットフォームとして機能します。これらのプラットフォームは、患者の病歴、治療記録、および管理データを一元化されたシステムに統合し、獣医療従事者が健康状態をより効率的に監視できるよう支援します。記録の整理を改善するだけでなく、獣医EHRシステムは、検査サービス、画像診断システム、およびクライアントとのコミュニケーションチャネルと連携することで、ワークフローの効率化を図ります。動物における慢性疾患の増加も、デジタル記録管理システムへの需要拡大に寄与しています。長期にわたる健康状態には、継続的なモニタリング、治療の調整、詳細な記録が必要となる場合が多く、効果的なケア管理にはデジタル記録システムが不可欠です。

2025年、小動物セグメントは3億3,060万米ドルの市場規模を記録しました。このセグメントが主導的な地位を維持しているのは、主に伴侶動物の飼育頭数の着実な増加と、専門的な獣医療サービスへの需要の高まりによるものです。伴侶動物を診療する獣医診療所は、患者情報、治療計画、および継続的なケア要件を管理するために、デジタル健康記録に大きく依存しています。EHRプラットフォームの利用により、獣医療専門家は、整理された病歴を維持し、予防ケアのスケジュールを追跡し、治療成果をより効果的にモニタリングすることが可能になります。ペットの飼い主が、より高い水準の獣医療や動物の医療管理の改善を求めるようになるにつれ、動物病院では効率的な患者記録管理をサポートする先進的なデジタルシステムを導入しています。小動物専門の動物病院や診療所は、事務作業の効率化、医療記録の管理、および診療所内の全体的なワークフロー効率の向上を実現するEHRの機能を活用しています。

2025年時点で、クラウド型EHRソリューションの市場シェアは72.6%を占めました。動物病院が患者データ管理のための柔軟かつ費用対効果の高い技術ソリューションを求める中、クラウド型システムの人気は高まり続けています。これらのプラットフォームにより、獣医療従事者は重要な健康情報を遠隔からアクセスできるようになり、獣医療チーム間の連携強化や、臨床現場での迅速な意思決定が可能になります。また、クラウドベースの導入により、大規模なオンプレミス型ITインフラの必要性が減り、動物病院の運営コストを削減できます。さらに、これらのシステムは自動更新、強化されたサイバーセキュリティ保護、安全なデータバックアップ機能を提供し、規制遵守やデータ保護要件をサポートします。遠隔診療やモバイル獣医療サービスの人気の高まりも、クラウドベースのEHRプラットフォームの導入をさらに加速させています。

北米の獣医EHR市場は2025年に40%のシェアを占め、2035年までCAGR13.4%で成長すると予測されています。北米における市場の成長は、獣医クリニックや病院全体でのデジタルヘルスケア技術の積極的な導入に支えられています。ペットの飼育率の高さと高度な獣医療サービスへの需要の増加が、デジタルヘルス管理システムの活用を後押しし続けています。同地域の獣医療従事者は、臨床ワークフローの効率化、データアクセスの改善、そしてより効率的な患者ケア管理を支援するため、EHRプラットフォームの導入をますます進めています。米国は、継続的な医療モニタリングと体系的な健康記録を必要とする伴侶動物の数が多いため、同地域における主要市場となっています。米国およびカナダの獣医療施設は、診断情報の統合を強化し、飼い主とのコミュニケーションを改善し、進化する遠隔医療サービスモデルを支援するクラウドベースのソリューションへと急速に移行しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- ペットの飼育率の増加

- 高度な獣医療への需要の高まり

- 獣医療現場における遠隔医療の統合

- 業界の潜在的リスク&課題

- 導入および維持管理コストの高さ

- サイバーセキュリティおよびデータ漏洩のリスク

- 市場機会

- 動物病院におけるクラウド型EHRの導入拡大

- AIを活用した診断およびワークフロー自動化ツールの統合

- 成長促進要因

- 成長可能性分析

- 規制状況(1次調査に基づく)

- 北米

- 米国

- カナダ

- 欧州

- アジア太平洋地域

- 北米

- 技術動向

- 現在の技術

- 新興技術

- 将来の市場動向(1次調査に基づく)

- AI/GEN AIの影響(1次調査に基づく)

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業のマトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:診療タイプ別、2022年~2035年

- 小動物

- 混合診療

- 馬

- 食肉用家畜

- その他の診療分野

第6章 市場推計・予測:提供形態別、2022年~2035年

- クラウド型EHR

- オンプレミス型EHR

第7章 市場推計・予測:用途別、2022年~2035年

- 診療管理

- 画像診断

第8章 市場推計・予測:最終用途別、2022年~2035年

- 動物病院・診療所

- 訪問診療・移動式動物病院

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2022年~2035年

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AcuroVet

- Animal Intelligence Software

- ClienTrax

- Covetrus

- DaySmart Software

- Digitail

- IDEXX

- Instinct Science

- Nordhealth

- Onward

- OSP

- Shepherd Veterinary Software