|

市場調査レポート

商品コード

1858974

缶入りアルコール飲料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Canned Alcoholic Beverages Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 缶入りアルコール飲料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年10月15日

発行: Global Market Insights Inc.

ページ情報: 英文 292 Pages

納期: 2~3営業日

|

概要

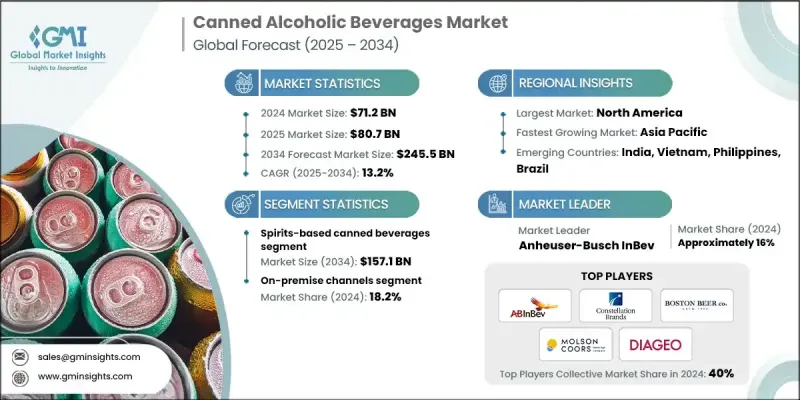

缶入りアルコール飲料の世界市場規模は2024年に712億米ドルで、CAGR 13.2%で成長し、2034年には2,455億米ドルに達すると予測されています。

市場成長の原動力となっているのは、利便性、持ち運びやすさ、現代消費者の間で高まる缶入りアルコール飲料の魅力です。これらの製品は、社交の場、お祭り、屋外イベント、気軽な飲み会など、幅広い場面で人気があります。カクテル、ワイン、ビール、ハードセルツァーなどの缶入りアルコール飲料は、多様な消費者の嗜好に対応し、ビーチ、公園、コンサートなど、ガラス包装が実用的でない、あるいは制限されている場所で特に支持されています。eコマースやデジタル・マーケティング・プラットフォームの台頭も、こうした製品をより身近で販促しやすくし、市場の成長に寄与しています。フレーバー、ブランディング、パッケージングにおける技術革新が進んでいることから、缶入りアルコール飲料業界は今後も拡大・多様化が続くものと思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 712億米ドル |

| 予測金額 | 2,455億米ドル |

| CAGR | 13.2% |

蒸留酒ベースの缶飲料セグメントは、2024年に467億米ドルを生み出し、2034年にはCAGR 12.9%で1,571億米ドルに達すると推定されます。このカテゴリーは、世界のレディ・トゥ・ドリンク(RTD)アルコール飲料の中で、最もダイナミックで高収益のセグメントとして急速に台頭してきました。その成長の原動力となっているのは、継続的な技術革新と製品のプレミアム化です。Tanqueray &Tonic RTD」、「Cutwater Spirits」、「On the Rocks」などの主要ブランドは、複雑なバー品質のカクテルを便利な缶入りで提供することで、消費者の期待を高めています。麦芽やワインベースの代替品とは異なり、スピリッツベースのRTD飲料は、テキーラ、ウォッカ、ラムなどの真のスピリッツの風味を再現し、プロが作るカクテルを反映した本格的な割合でミックスできる点が特徴です。

2024年のオフプレミス・チャネルのシェアは50%。このチャネルの優位性は、特に消費者行動がパンデミック後に家庭での消費とリラックスした社交の場へとシフトしたため、このチャネルのアクセスのしやすさと利便性に起因します。酒販店、食料品チェーン、コンビニエンスストアなどの小売業者は、まとめ買い割引や新フレーバーの提供を通じて価値を提供し、試飲購入やブランド発掘を促しています。季節ごとの発売や地域ごとの製品バリエーションも、忠実な消費者のリピート購入行動を後押ししています。

米国の缶入りアルコール飲料市場は2024年に259億米ドルに達し、CAGR 9.9%で成長すると予測されます。米国市場は、すぐに飲める(RTD)飲料に対する消費者の嗜好と、同国の堅調なクラフト飲料シーンに牽引され、缶入りアルコール飲料の需要をリードしています。缶入り飲料は持ち運びが容易で消費しやすいため、特に屋外環境での人気が高まっており、市場の成長をさらに後押ししています。

缶入りアルコール飲料世界市場の主要企業は、Cutwater Spirits、Boston Beer Company、Heineken N.V.、Carlsberg Group、Constellation Brands、Molson Coors Beverage Company、Diageo plc、White Claw(Mark Anthony Brands)、Asahi Group Holdings、Anheuser-Busch InBevです。缶入りアルコール飲料市場の各社は、競争力を強化するため、イノベーション、プレミアム化、市場拡大に注力しています。Diageo plc社、Boston Beer Company社、Constellation Brands社などの主要企業は、進化する味覚嗜好に対応するため、多様なフレーバープロファイルやスピリッツを前面に押し出した処方を導入しています。バーやレストラン、eコマース・プラットフォームとの戦略的パートナーシップは、流通を後押ししています。さらに、持続可能なパッケージング、地域ごとの製品ローカライゼーション、デジタル・マーケティング・キャンペーンへの投資が、ブランドの認知度を高めています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- アルコール度数別

- 今後の市場動向

- テクノロジーとイノベーションの展望

- 現在の技術動向

- 新たなテクノロジー

- 特許情勢

- 貿易統計

- 主要輸入国

- 主要輸出国

(注:貿易統計は主要国についてのみ提供されます)

- 持続可能性と環境側面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境にやさしい取り組み

- カーボンフットプリント

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- パートナーシップ

- 新製品発表

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- モルト缶飲料

- 伝統的なビール(ラガー、エール、スタウト)

- フレーバー麦芽飲料(FMBS)

- モルト系ハードセルツァー

- ワインベースの缶飲料

- 缶入りスティルワイン

- ワインスプリッツァー&クーラー

- フルーツ系ハードセルツァー

- スピリッツ系缶飲料

- Rtdカクテル

- 缶ロングドリンク

- プレミアム缶カクテル

- スペシャルティ缶入りアルコール飲料

- ハードティー

- ハードコーヒー

- ハードコンブチャ

第6章 市場推計・予測アルコール度数別、2021-2034

- 主要動向

- ノンアルコール製品(アルコール度数0.05%~0.5)

- 低アルコール製品(アルコール度数0.5%以上3.0%未満)

- 標準アルコール製品(アルコール度数3.0%~8.0)

- 高アルコール製品(アルコール度数8.0%以上)

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- オンプレミス・チャネル

- バー・居酒屋

- レストラン・フードサービス

- 娯楽施設

- ホテル&ホスピタリティ

- オフプレミス・チャネル

- 食料品店

- コンビニエンスストア

- 酒販店・専門店

- ビール販売業者

- 州内チャネル

- 消費者直販(DTC)

- eコマース&デジタル・チャネル

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Anheuser-Busch InBev

- Arbor Brewing Company India

- Asahi Group Holdings

- Barnstormer Brewing &Distilling Co.

- Boston Beer Company

- Carlsberg Group

- Cervejaria Cathedral

- Cervejaria Tarantino

- Cloudburst Brewing

- Constellation Brands

- Cutwater Spirits

- Diageo plc

- Fat Bottom Brewing

- Founders Brewing Co.

- Four Mile Brewing

- Goose Island Beer Company

- Heineken N.V.

- Lagunitas Brewing Company

- Molson Coors Beverage Company

- Parrotdog

- Purity Brewing Co

- Stone Brewing

- Thorn Brewing Co.

- Truly Hard Seltzer(Boston Beer)

- White Claw(Mark Anthony Brands)

- Others