精密農業市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Precision Farming Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685053

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

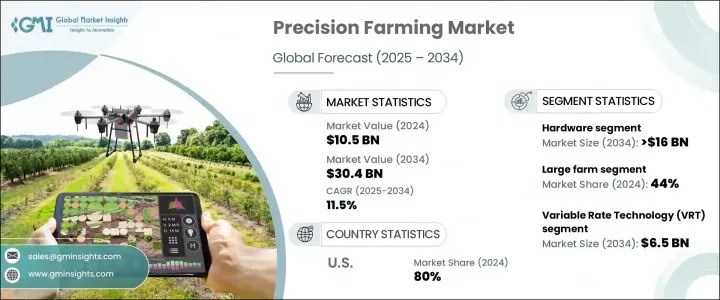

世界の精密農業市場は2024年に105億米ドルと評価され、2025~2034年にかけて11.5%のCAGRで成長すると予測されています。

急速な人口増加と食糧需要の増加が、この市場拡大の主要原動力となっています。世界人口が毎年約8,300万人ずつ増加する中、サステイナブル農業の実践がより急務となっています。作物の収量を最適化するために先端技術を活用する精密農業は、この課題に対する重要な解決策として浮上してきました。

精密農業の導入を促進する上で、世界各国の政府は重要な役割を果たしています。補助金や助成金、施策的インセンティブを提供することで、環境への影響を最小限に抑えながら農業の生産性を高めることを目指しています。精密農業は、IoT、AI、ドローン、データ分析などの技術を統合し、効率を向上させ、資源消費を削減します。これらの技術革新は、農業従事者の生産性向上、運営コスト削減、エコフレンドリー実践を支援し、長期的にサステイナブル食糧生産を保証します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 105億米ドル |

| 予測金額 | 304億米ドル |

| CAGR | 11.5% |

市場はコンポーネント別に区分され、2024年にはハードウェアが55%以上の市場シェアを占めてトップに立ちます。2034年までに、このセグメントは160億米ドルを超えると予測されます。農作業におけるGPS、センサ、自動化機器の採用が増加していることが、この成長を後押ししています。土壌センサ、ウェザーステーション、GPSレシーバーなどのハードウェアツールにより、農業従事者はコンディションをモニターし、灌漑を最適化し、植え付けや収穫などの重要な作業を自動化することができます。自動化はさらに効率を高め、従来は手作業で行っていた作業をロボットシステムが行っています。

農場規模別では、大規模農場が2024年の市場シェアの約44%を占めています。生産性と効率性を向上させるために先端技術に投資できることが、この優位性の一因となっています。GPS誘導トラクター、ドローン、スマート灌漑システムにより、作物の正確なモニタリングと資源管理が可能になります。大規模農場がオペレーションの最適化を目指す中、精密農業ソリューションの需要は高まり続けています。

技術面では、可変レート技術(VRT)が支配的なセグメントであり、2034年までに65億米ドルを生み出すと予想されています。この技術により、農業従事者は特定の圃場条件に基づいて肥料、種子、農薬の散布を調整することができます。センサ、GPS、先進的ソフトウェアからのデータを活用することで、VRTは最適な投入量配分を保証し、収穫量を最大化しながら無駄を省きます。コスト効率とサステイナブル農業が重視されるようになったことで、導入が加速しており、農業機関からの支援も増えているため、こうしたシステムはより身近なものとなっています。

用途別では、収量モニタリングが2024年のシェア25%で市場をリードしています。このシステムは、農業従事者が作物の出来をリアルタイムで追跡し、生産性を高めるためのデータ主導の意思決定を可能にします。センサ技術とデータ分析の進歩により、収量パターンと土壌状態に関する正確な洞察が得られ、長期的な農場管理が改善されます。食糧需要の増加に伴い、精密農業ソリューションは農業生産の最適化に不可欠となっています。

北米が世界市場をリードしており、2024年には米国が80%のシェアを占めます。先進農業技術の普及、政府補助金、強力なインフラが精密農業の拡大を支えています。ドローン、センサ、データ分析への依存の高まりは、農業経営を変革し続け、農業をより効率的で収益性の高いものにしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- ハードウェアプロバイダー

- ソフトウェアプロバイダー

- サービスプロバイダー

- 技術プロバイダー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 精密農業の進化

- 使用事例

- 影響要因

- 促進要因

- サステイナブル農業へのニーズの高まり

- 世界人口の増加と、それに伴う食糧増産への需要の高まり

- 農業技術への投資の増加

- デジタル農業技術を支援する政府の取り組みと補助金

- 産業の潜在的リスク・課題

- 先進的精密農業機械を操作する熟練労働者の不足

- 農村部における高速インターネットへのアクセス制限

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:コンポーネント別、2021~2034年

- 主要動向

- ハードウェア

- センサ

- 自動操舵システム

- ドローン、UAV、カメラ

- モバイル機器

- GPSとGNSS

- その他

- ソフトウェア

- 農場管理ソフトウェア(FMS)

- データ分析とビッグデータソリューション

- 地理情報システム(GIS)ソフトウェア

- クラウドベースのソフトウェアソリューション

- 人工知能と機械学習ソフトウェア

- サービス

- プロフェッショナルサービス

- マネージドサービス

第6章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 高精度測位システム

- ジオマッピング

- リモートセンシング

- 統合電子通信

- 可変レート技術(VRT)

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 天候モニタリング

- 収量モニタリング

- 圃場マッピング

- 灌漑管理

- 廃棄物管理

- 財務管理

- その他

第8章 市場推定・予測:農場規模別、2021~2034年

- 主要動向

- 小規模農場

- 中規模農場

- 大規模農場

第9章 市場推定・予測:地域別、2021~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AG Leader

- AGCO

- Agribotix

- AgSense

- AgSmarts

- Boumatic

- CNH

- CropMetrics

- CropX

- Delaval

- Dickey-John

- Farmers Edge

- GEA Group

- John Deere

- Monsanto

- Precision Planting

- Raven

- Topcon

- Trimble

- Yara

目次

The Global Precision Farming Market was valued at USD 10.5 billion in 2024 and is projected to grow at an 11.5% CAGR from 2025 to 2034. Rapid population growth and the increasing demand for food are key drivers behind this expansion. With the global population rising by approximately 83 million annually, the need for sustainable agricultural practices has become more urgent. Precision farming, which leverages advanced technologies to optimize crop yields, has emerged as a critical solution to this challenge.

Governments worldwide are playing a crucial role in promoting the adoption of precision agriculture. By offering subsidies, grants, and policy incentives, they aim to boost agricultural productivity while minimizing environmental impact. Precision farming integrates technologies such as IoT, AI, drones, and data analytics to improve efficiency and reduce resource consumption. These innovations help farmers enhance productivity, cut operational costs, and implement eco-friendly practices, ensuring sustainable food production in the long run.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 billion |

| Forecast Value | $30.4 billion |

| CAGR | 11.5% |

The market is segmented based on components, with hardware leading in 2024, holding over 55% market share. By 2034, the segment is anticipated to surpass USD 16 billion. The increasing adoption of GPS, sensors, and automated equipment in farming operations is driving this growth. Hardware tools such as soil sensors, weather stations, and GPS receivers enable farmers to monitor conditions, optimize irrigation, and automate critical tasks like planting and harvesting. Automation further enhances efficiency, with robotic systems performing tasks traditionally handled manually.

By farm size, large farms accounted for approximately 44% of the market share in 2024. Their ability to invest in advanced technology for improved productivity and efficiency contributes to this dominance. GPS-guided tractors, drones, and smart irrigation systems allow for precise crop monitoring and resource management. As large-scale farms seek to optimize operations, demand for precision farming solutions continues to rise.

Technology-wise, variable rate technology (VRT) is a dominant segment, expected to generate USD 6.5 billion by 2034. This technology allows farmers to tailor the application of fertilizers, seeds, and pesticides based on specific field conditions. By leveraging data from sensors, GPS, and advanced software, VRT ensures optimal input distribution, reducing waste while maximizing yield. The growing emphasis on cost efficiency and sustainable farming is accelerating adoption, with increased support from agricultural institutions making these systems more accessible.

In terms of applications, yield monitoring led the market in 2024 with a 25% share. This system helps farmers track crop performance in real time, enabling data-driven decisions to enhance productivity. Advancements in sensor technology and data analytics provide precise insights into yield patterns and soil conditions, improving long-term farm management. With increasing food demand, precision farming solutions are becoming essential for optimizing agricultural output.

North America leads the global market, with the US holding an 80% share in 2024. The widespread adoption of advanced agricultural technologies, government subsidies, and strong infrastructure support precision farming expansion. Increased reliance on drones, sensors, and data analytics continues to transform farming operations, making agriculture more efficient and profitable.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Hardware providers

- 3.1.2 Software providers

- 3.1.3 Service providers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Evolution of precision farming

- 3.9 Use cases

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 The growing need for sustainable farming practices

- 3.10.1.2 The rising global population and the corresponding demand for higher food production

- 3.10.1.3 Increased investment in agricultural technologies

- 3.10.1.4 Government initiatives and subsidies supporting digital farming technologies

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 The lack of skilled labor to operate advanced precision farming equipment

- 3.10.2.2 Limited access to high-speed internet in rural areas

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensor

- 5.2.2 Automated steering system

- 5.2.3 Drone, UAV, and camera

- 5.2.4 Mobile device

- 5.2.5 GPS and GNSS

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Farm Management Software (FMS)

- 5.3.2 Data analytics and big data solution

- 5.3.3 Geographic information system (GIS) software

- 5.3.4 Cloud-based software solution

- 5.3.5 Artificial intelligence and machine learning software

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 High precision positioning system

- 6.3 Geo mapping

- 6.4 Remote sensing

- 6.5 Integrated electronic communication

- 6.6 Variable Rate Technology (VRT)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Weather monitoring

- 7.3 Yield monitoring

- 7.4 Field mapping

- 7.5 Irrigation management

- 7.6 Waste management

- 7.7 Financial management

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Farm Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Small farm

- 8.3 Medium farm

- 8.4 Large farm

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AG Leader

- 10.2 AGCO

- 10.3 Agribotix

- 10.4 AgSense

- 10.5 AgSmarts

- 10.6 Boumatic

- 10.7 CNH

- 10.8 CropMetrics

- 10.9 CropX

- 10.10 Delaval

- 10.11 Dickey-John

- 10.12 Farmers Edge

- 10.13 GEA Group

- 10.14 John Deere

- 10.15 Monsanto

- 10.16 Precision Planting

- 10.17 Raven

- 10.18 Topcon

- 10.19 Trimble

- 10.20 Yara

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日