|

市場調査レポート

商品コード

1685052

クラウド移行サービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cloud Migration Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| クラウド移行サービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月07日

発行: Global Market Insights Inc.

ページ情報: 英文 211 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

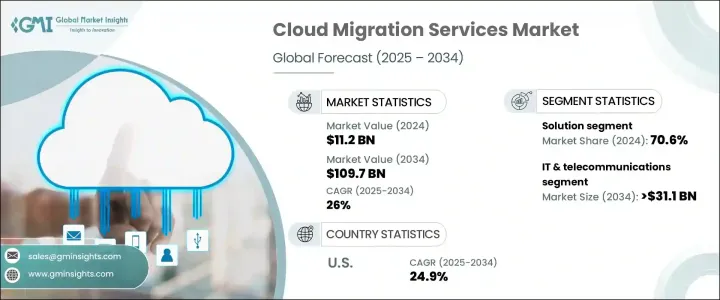

世界のクラウド移行サービス市場は、2024年に112億米ドルと評価され、2025年から2034年にかけてCAGR 26%という驚異的な成長率を遂げると予測されています。

企業が拡張性、柔軟性、効率性に優れたITインフラをますます求めるようになるにつれ、クラウド移行サービスの採用が急速に勢いを増しています。これらのサービスはIT戦略の近代化に不可欠であり、コスト削減、業務効率の改善、デジタルソリューションの迅速な展開を可能にします。今日の企業は、競争力を維持しなければならないというプレッシャーに直面しており、クラウド移行サービスは、インフラを最適化しながら、俊敏性を強化し、セキュリティを向上させ、進化する顧客ニーズに対応する方法を提供します。

しかし、クラウドへの移行に課題がないわけではありません。適切な計画と戦略の欠如は、多くの場合、遅延、予期せぬコスト、運用の非効率性をもたらします。構造化されたアプローチなしに移行すると、互換性の問題、データ・セキュリティの脆弱性、プロセス中の混乱につながる可能性があります。そのため、組織は綿密な計画と実行を優先し、スムーズで効率的なクラウド移行を実現する必要があります。これにより、こうした挫折のリスクを軽減し、長期的な成功を保証することができます。シームレスなクラウド移行を実現するには、インフラ、アプリケーション、データの複雑な移行を管理するための専門知識とツールを活用する必要があります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 112億米ドル |

| 予測金額 | 1,097億米ドル |

| CAGR | 26% |

市場はソリューションとサービスに分かれ、2024年にはソリューションが70.6%と圧倒的なシェアを占める。これには、インフラ、プラットフォーム、データベース、アプリケーション、ストレージの移行が含まれます。これらのソリューションは、複雑なIT環境を管理するために不可欠であり、クラウド移行を円滑かつ効果的に評価、計画、実行するために必要なツールと専門知識を企業に提供します。プロセスを合理化し生産性を向上させるためにクラウド移行サービスを採用する企業が増えるにつれ、包括的なクラウド・ソリューションに対する需要は急増の一途をたどっています。

業界別では、クラウド移行サービス市場はIT・通信、BFSI、ヘルスケア、政府・公共部門、その他に区分されます。特にIT・通信分野は大幅な成長が見込まれ、2034年には311億米ドルに達します。増大するデータ量を処理し、最先端技術をサポートするためのスケーラブルなインフラへのニーズが、この分野でのクラウド移行サービスへの需要に拍車をかけています。これらのサービスにより、企業はワークロードを最適化し、効率を高め、運用コストを削減することができます。

米国では、クラウド移行サービス市場は2034年までCAGR 24.9%で成長する見通しです。高度なITインフラが存在し、クラウドサービスプロバイダーが集中していることから、米国は世界市場の主要プレーヤーとして位置づけられています。全米の組織は、従来のオンプレミスシステムから脱却し、デジタルトランスフォーメーションの取り組みを加速させるため、クラウド移行サービスへの依存度を高めています。さらに、有利な規制や政府の支援プログラムにより、特に公共サービスにおいてクラウドの導入が進む環境が整いつつあります。大企業が市場をリードする一方で、中堅企業も独自の要件に対応したコスト効率の高いクラウド・ソリューションを採用しており、この分野の急速な拡大にさらに貢献しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 俊敏性と自動化への需要の高まり

- クラウドネイティブテクノロジーの採用拡大

- 進化するセキュリティ環境

- 政府の取り組みと規制

- クラウドサービスの成熟度と費用対効果

- 業界の潜在的リスク&課題

- 計画と戦略の欠如

- 隠れたコストとベンダーの囲い込み

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:プラットフォーム別、2021年~2034年

- 主要動向

- ソリューション

- インフラ移行

- プラットフォーム移行

- データベース移行

- アプリケーションの移行

- ストレージの移行

- サービス

- プロフェッショナルサービス

- マネージドサービス

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- パブリッククラウド

- プライベートクラウド

- ハイブリッド

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 大企業

- 中小企業(SME)

第8章 市場推計・予測:用途別、2021-2034年

- 主要動向

- プロジェクト管理

- インフラ管理

- セキュリティ・コンプライアンス管理

- サプライチェーン管理(SCM)

- コンテンツ管理

- その他

第9章 市場推計・予測:業界別、2021年~2034年

- 主要動向

- IT・通信

- BFSI

- ヘルスケア

- 政府・公共機関

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ

第11章 企業プロファイル

- Accenture

- Amazon Web Services, Inc.

- Capgemini

- Cognizant Technology Solutions Corp

- DXC Technology

- Evolve IP LLC

- Google LLC

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Kyndryl Inc.

- Microsoft

- NTT DATA Americas, Inc.

- Oracle Corporation

- Rackspace Hosting Inc.

- SAP SE

- Sunrise Technologies

- Tata Communications

- Veritis Group Inc.

- VMware, Inc.

- Wipro

- WSM International LLC

The Global Cloud Migration Services Market was valued at USD 11.2 billion in 2024 and is anticipated to experience an impressive growth rate of 26% CAGR from 2025 to 2034. As organizations increasingly demand scalable, flexible, and efficient IT infrastructure, the adoption of cloud migration services is rapidly gaining momentum. These services are crucial for modernizing IT strategies, enabling businesses to cut costs, improve operational efficiency, and speed up the deployment of digital solutions. Businesses today face mounting pressure to stay competitive, and cloud migration services offer a way to enhance agility, improve security, and meet evolving customer needs while optimizing their infrastructure.

The transition to the cloud, however, is not without its challenges. A lack of proper planning and strategy often results in delays, unexpected costs, and operational inefficiencies. Migrating without a structured approach can lead to compatibility issues, data security vulnerabilities, and disruptions during the process. Therefore, organizations must prioritize meticulous planning and execution to ensure smooth, efficient cloud migration, which reduces the risk of these setbacks and guarantees long-term success. Achieving a seamless cloud transition requires leveraging specialized knowledge and tools to manage the complexities of migrating infrastructure, applications, and data.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.2 Billion |

| Forecast Value | $109.7 Billion |

| CAGR | 26% |

The market is split into solutions and services, with solutions accounting for a dominant share of 70.6% in 2024. This includes infrastructure, platform, database, application, and storage migration. These solutions are essential for managing complex IT environments and provide businesses with the tools and expertise necessary to assess, plan, and execute their cloud migrations smoothly and effectively. As more organizations adopt cloud migration services to streamline their processes and enhance productivity, the demand for comprehensive cloud solutions continues to surge.

By vertical, the cloud migration services market is segmented into IT & telecommunications, BFSI, healthcare, government & public sector, and others. The IT & telecommunications sector, in particular, is expected to see substantial growth, reaching USD 31.1 billion by 2034. The need for scalable infrastructure to handle the growing volumes of data and support cutting-edge technologies is fueling the demand for cloud migration services in this vertical. These services allow organizations to optimize workloads, boost efficiency, and reduce operational costs, which is vital in an industry marked by rapid technological advancements.

In the U.S., the cloud migration services market is poised to grow at a CAGR of 24.9% through 2034. The presence of advanced IT infrastructure, coupled with a high concentration of cloud service providers, positions the U.S. as a key player in the global market. Organizations across the country are increasingly relying on cloud migration services to move away from traditional on-premises systems and to accelerate their digital transformation initiatives. Additionally, favorable regulations and government-backed programs have created an environment conducive to greater cloud adoption, particularly in public services. While large enterprises lead the market, mid-sized businesses are also embracing cost-effective cloud solutions that cater to their unique requirements, further contributing to the sector's rapid expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.7 Growth drivers

- 3.7.1 Increasing demand for agility and automation

- 3.7.2 Growing adoption of cloud-native technologies

- 3.7.3 Evolving security landscape

- 3.7.4 Government initiatives and regulations

- 3.7.5 Maturity and cost-effectiveness of cloud services

- 3.8 Industry pitfalls & challenges

- 3.8.1 Lack of planning and strategy

- 3.8.2 Hidden costs and vendor lock-in

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Infrastructure migration

- 5.2.2 Platform migration

- 5.2.3 Database migration

- 5.2.4 Application migration

- 5.2.5 Storage migration

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Public cloud

- 6.3 Private cloud

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 Small & medium-sized enterprises(SME)

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Project management

- 8.3 Infrastructure management

- 8.4 Security & compliance management

- 8.5 Supply chain management(SCM)

- 8.6 Content management

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Vertical, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 IT & telecommunications

- 9.3 BFSI

- 9.4 Healthcare

- 9.5 Government & public sector

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Accenture

- 11.2 Amazon Web Services, Inc.

- 11.3 Capgemini

- 11.4 Cognizant Technology Solutions Corp

- 11.5 DXC Technology

- 11.6 Evolve IP LLC

- 11.7 Google LLC

- 11.8 Hewlett Packard Enterprise Development LP

- 11.9 IBM Corporation

- 11.10 Kyndryl Inc.

- 11.11 Microsoft

- 11.12 NTT DATA Americas, Inc.

- 11.13 Oracle Corporation

- 11.14 Rackspace Hosting Inc.

- 11.15 SAP SE

- 11.16 Sunrise Technologies

- 11.17 Tata Communications

- 11.18 Veritis Group Inc.

- 11.19 VMware, Inc.

- 11.20 Wipro

- 11.21 WSM International LLC