|

市場調査レポート

商品コード

1928904

自動車用エネルギー回収システム市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Energy Recovery System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用エネルギー回収システム市場における機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月08日

発行: Global Market Insights Inc.

ページ情報: 英文 255 Pages

納期: 2~3営業日

|

概要

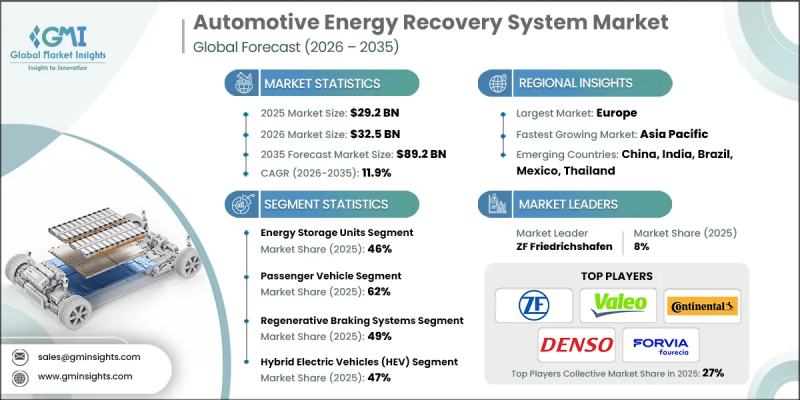

世界の自動車用エネルギー回生システム市場は、2025年に292億米ドルと評価され、2035年までにCAGR 11.9%で成長し、892億米ドルに達すると予測されています。

この成長は、車両のエネルギー利用効率向上、燃料消費量の削減、そしてますます厳格化する環境基準への対応が必要であることから推進されています。自動車メーカーは、車両の運転中に失われるエネルギーを回収・再利用するシステムを優先的に導入しており、これによりコスト効率と排出量削減の両方の目標を支援しています。電気式およびハイブリッド式パワートレインへの移行が加速していることも需要をさらに後押ししており、エネルギー回収ソリューションはオプションの追加機能ではなく、車両構造に不可欠な要素となりつつあります。これらのシステムは、航続距離の延長、エネルギー管理の最適化、および車両全体の性能向上を支援します。世界市場における規制圧力により、自動車メーカーは包括的なエネルギー最適化戦略を推進し続けています。その結果、市場は、複数の回収・管理技術が先進的なパワートレインプラットフォーム内で連携して動作する、完全に統合されたシステムレベルのソリューションへと進化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 292億米ドル |

| 予測金額 | 892億米ドル |

| CAGR | 11.9% |

エネルギー貯蔵ユニットセグメントは2025年に46%のシェアを占め、2026年から2035年にかけてCAGR12.2%で成長すると予測されています。このセグメントが主導的な地位にあるのは、回収されたエネルギーを効率的に貯蔵し再利用することで、測定可能な性能と効率の向上を実現する必要があるためです。エネルギー貯蔵ソリューションは、電動化およびハイブリッド車両プラットフォーム全体において、推進要件、補助システム、および総合的な電力管理をサポートします。回収システムとの統合は、エネルギー再利用の最大化と運用効率の向上に不可欠です。

乗用車カテゴリーは2025年に62%のシェアを占め、2035年までCAGR12%で成長すると予測されています。この成長は、燃費効率と低排出ガス車両への消費者関心の高まり、支援的な政策枠組み、価格帯を問わず電動モデルの普及拡大によって支えられています。先進的な回収ソリューションは、高級車セグメントと量産車セグメントの両方でますます採用が進んでいます。

ドイツの自動車用エネルギー回収システム市場は、2026年から2035年にかけてCAGR10%で成長すると予測されています。同国の強力な自動車製造基盤と排出量削減への規制的焦点が、複数の車両カテゴリーにおける先進的な回収技術の統合を加速させています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 電気自動車およびハイブリッド車の普及拡大

- 厳格な排出ガス規制および燃費基準

- エネルギー回収技術の進展

- 環境に優しくコスト効率の高い車両に対する消費者需要の高まり

- 交通渋滞と都市化の圧力

- 業界の潜在的リスク&課題

- エネルギー回収システムの初期コストの高さ

- 消費者の間におけるエネルギー回収技術に関する認知度と理解度の不足

- 市場機会

- 電気自動車およびハイブリッド車の普及拡大

- より厳格な排出ガス規制および燃費効率規制

- フリートおよび商用車の効率性に対する関心の高まり

- エネルギー貯蔵技術とパワーエレクトロニクスの進歩

- 新興自動車市場における新たな機会

- 成長可能性分析

- 規制情勢

- 北米

- 米国-環境保護庁(EPA)MY2027+基準

- カナダ- カナダZEVプログラム

- 欧州

- ドイツ-EU二酸化炭素排出基準(2030年までに37.5%削減)

- 英国- 英国ZEV義務(2035年までに新車販売の100%をゼロエミッション車とする)

- フランス- ボーナス・マルス制度

- イタリア- 国家復興・レジリエンス計画(PNRR)

- アジア太平洋地域

- 中国- 新エネルギー車(NEV)導入義務

- インド-FAME-IIプログラム

- 日本- ハイブリッド車・電気自動車に対する経済産業省の補助金

- オーストラリア- 国家電気自動車戦略

- LATAM

- メキシコ-NOM-163-SCFI-2013 排出ガス基準

- アルゼンチン- 燃費規制

- 中東・アフリカ

- 南アフリカ共和国- 道路交通排出ガス基準

- サウジアラビア- 国家産業開発・物流プログラム

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許分析

- 使用事例と成功事例

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントに関する考慮事項

- 将来展望と機会

- OEM統合と車両アーキテクチャ適合性

- パッケージング制約(スペース、重量、熱)

- 既存のパワートレインおよびブレーキシステムとの統合

- プラットフォームレベルでの準備状況(内燃機関vsハイブリッドvs BEVスケートボード)

- キャリブレーション及び検証における課題

- 費用便益及び回収期間分析

- 車両あたりのコストプレミアム

- 燃費・航続距離の向上と追加コストの比較

- 車種別回収期間

- フリートと乗用車の経済性比較

- ERS性能ベンチマーク

- ソフトウェア、制御システム及びエネルギー管理インテリジェンス

- 熱管理及び放熱制約

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2022-2035

- エネルギー貯蔵ユニット

- 電池

- スーパーキャパシタ

- フライホイール

- エネルギー変換ユニット

- 電動機/発電機

- 油圧式または空圧式コンバーター

- 制御ユニット

- 電子制御モジュール(ECM)

- 電力管理システム

第6章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- SUV

- セダン

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

- 電気自動車およびハイブリッド車

第7章 市場推計・予測:システム別、2022-2035

- 運動エネルギー回生システム(KERS)

- 回生ブレーキシステム

- 排気エネルギー回収システム(EERS)

- サスペンションベースのエネルギー回収システム

第8章 市場推計・予測:推進力別、2022-2035

- 内燃機関車

- ハイブリッド電気自動車(HEV)

- プラグインハイブリッド電気自動車(PHEV)

- バッテリー式電気自動車(BEV)

第9章 市場推計・予測:用途別、2022-2035

- 制動エネルギー回生

- 排熱回収

- 熱管理および廃熱利用

- パワートレイン効率の向上

- 燃費向上

- 性能向上

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界プレイヤー

- Aisin Seiki

- BorgWarner

- Continental

- Cummins

- Denso

- Forvia

- Hitachi Automotive Systems

- Hyundai Mobis

- Mahle

- Mitsubishi Electric

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- 地域別企業

- Kongsberg Automotive

- Mando

- Nabtesco

- Tenneco

- TRW Automotive

- Emerging Technology イノベーター

- BYD Auto

- Leoni

- Nidec

- Rimac Automobili