|

市場調査レポート

商品コード

1665352

自動車用運動エネルギー回生システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Kinetic Energy Recovery System (KERS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用運動エネルギー回生システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

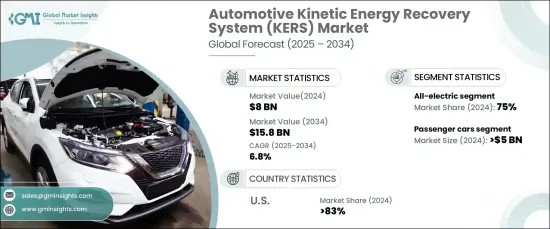

自動車用運動エネルギー回生システム(KERS)の世界市場は、2024年に80億米ドルと評価され、2025~2034年にかけてCAGR 6.8%で成長すると予測されています。

KERSと回生ブレーキシステムの統合は、ブレーキエネルギーを再利用可能な電力に変換することで、自動車のエネルギー効率に革命をもたらしています。この革新的な技術は、従来の燃料への依存を最小限に抑え、世界の持続可能性の目標にシームレスに合致します。自動車メーカー各社は、ハイブリッド車や電気自動車にKERSを搭載し、省エネルギーを高め、性能を向上させ、厳しい排ガス規制への適合を確保する動きが加速しています。

都市化の急速な進展とスマートシティ構想の台頭は、エコフレンドリー輸送ソリューションへの需要を煽っています。KERSは、大都市圏でよく見られるストップ・アンド・ゴーの交通におけるエネルギー使用を最適化し、都市モビリティの要として台頭してきています。電動モビリティインフラへの投資の拡大と公共交通システムの電化が、KERS技術の採用をさらに後押ししています。これにより、KERSはサステイナブル都市交通システムの不可欠なコンポーネントとして位置づけられ、世界市場の成長を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 80億米ドル |

| 予測金額 | 158億米ドル |

| CAGR | 6.8% |

車種別では、商用車と乗用車に区分されます。2024年には乗用車が市場を席巻し、50億米ドルの売上を計上します。このリーダーシップは、乗用車にハイブリッドと電気技術が広く採用され、KERSが燃費を大幅に向上させ、排出ガスを削減することに起因しています。環境的に持続可能でエネルギー効率の高い輸送ソリューションに対する消費者の嗜好の高まりが、KERS搭載車への需要を拡大し続け、市場の拡大を牽引しています。

市場はさらに推進力別に全電気自動車、PHEV、HEV、FCEVに分類されます。全電気式セグメントは、エネルギー回生システムとのシームレスな統合による恩恵を受け、2024年には75%のシェアを占めます。KERSは、制動エネルギーを回収・再利用することでエネルギー効率を向上させ、電気自動車の走行距離を延ばすという極めて重要な役割を果たしています。EV導入に対する政府の支援策と厳しい排ガス規制が、KERS技術の採用を強化しています。軽量コンポーネントの進歩も、全電気推進システムの優位性拡大に寄与しています。

米国の自動車用運動エネルギー回生システム市場は、ハイブリッド車と電気自動車の採用への強いコミットメントが原動力となり、2024年には83%という驚異的なシェアを占めました。より厳しい排出基準や燃費規制が、自動車メーカーにKERSのようなエネルギー効率の高い技術の導入を促しています。連邦政府による優遇措置とサステイナブルイノベーションへの多額の投資が、市場の成長をさらに加速させています。強固な研究開発インフラと大手自動車メーカーの集中により、米国はKERS技術の進歩をリードし続け、世界市場のリーダーとしての地位を固めています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- 原料サプライヤー

- 部品サプライヤー

- メーカー

- サービスプロバイダー

- 販売業者

- 最終用途

- 利益率分析

- 価格分析

- コスト内訳分析

- 技術とイノベーションの展望

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 厳しい排ガス規制による採用

- ハイブリッド車と電気自動車への統合の増加

- 効率向上のための軽量材料の進歩

- 燃費効率と持続可能性への注目の高まり

- 産業の潜在的リスク・課題

- 先進KERS技術に伴う高コスト

- 低価格車セグメントでの採用が限定的

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:2021~2034年自動車別

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- その他

- 商用車

- 小型車

- 中型車

- 大型車

第6章 市場推定・予測:システム別、2021~2034年

- 主要動向

- フライホイール

- バッテリー

- スーパーキャパシタ

第7章 市場推定・予測:推進力別、2021~2034年

- 主要動向

- 全電気自動車

- PHEV

- HEV

- FCEV

第8章 市場推定・予測:KERS別、2021~2034年

- 主要動向

- 機械式

- 電気機械式

- 油圧式

- 電子式

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Advics

- Aisin

- Bosch

- Brembo

- Continental

- Denso

- Haldex

- Hitachi Astemo

- Hyundai Mobis

- Magna International

- Mando

- Nidec

- PHINIA

- Schaeffler

- Skeleton Technologies

- Tenneco

- Torotrak

- TRW Automotive

- Valeo

- ZF Friedrichshafen

The Global Automotive Kinetic Energy Recovery System Market was valued at USD 8 billion in 2024 and is projected to grow at a CAGR of 6.8% from 2025 to 2034. The integration of KERS with regenerative braking systems is revolutionizing energy efficiency in vehicles by converting braking energy into reusable power. This innovative technology minimizes reliance on conventional fuels, aligning seamlessly with global sustainability goals. Automakers are increasingly incorporating KERS into hybrid and electric vehicles, enhancing energy savings, boosting performance, and ensuring compliance with stringent emission standards.

The surge in urbanization and the rise of smart city initiatives are fueling demand for eco-friendly transportation solutions. KERS is emerging as a cornerstone of urban mobility, optimizing energy use in stop-and-go traffic common in metropolitan areas. The growing investments in electric mobility infrastructure and the electrification of public transit systems are further propelling the adoption of KERS technology. This positions KERS as an indispensable component of sustainable urban transportation systems, catalyzing global market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8 Billion |

| Forecast Value | $15.8 Billion |

| CAGR | 6.8% |

By vehicle type, the market is segmented into commercial vehicles and passenger cars. Passenger cars dominated the market in 2024, generating USD 5 billion in revenue. This leadership is attributed to the widespread adoption of hybrid and electric technologies in passenger vehicles, where KERS significantly enhances fuel efficiency and reduces emissions. The growing consumer preference for environmentally sustainable and energy-efficient transportation solutions continues to amplify demand for KERS-equipped vehicles, driving the market's expansion.

The market is further categorized by propulsion into all-electric, PHEV, HEV, and FCEV. The all-electric segment held a commanding 75% share in 2024, benefiting from seamless integration with energy recovery systems. KERS plays a pivotal role in improving energy efficiency by capturing and reusing braking energy, which extends the driving range of electric vehicles. Supportive government incentives for EV adoption, coupled with stringent emission regulations, are reinforcing the adoption of KERS technology. Advancements in lightweight components are also contributing to the growing dominance of all-electric propulsion systems.

The U.S. automotive kinetic energy recovery system (KERS) market accounted for an impressive 83% share in 2024, driven by a strong commitment to hybrid and electric vehicle adoption. Stricter emission standards and fuel economy regulations are encouraging automakers to implement energy-efficient technologies like KERS. Federal incentives and substantial investments in sustainable innovations are further accelerating market growth. With a robust research and development infrastructure and a high concentration of leading automakers, the U.S. continues to lead advancements in KERS technology, solidifying its position as a global market leader.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Manufacturer

- 3.2.4 Service provider

- 3.2.5 Distributor

- 3.2.6 End-use

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Cost breakdown analysis

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Adoption driven by stringent emission regulations

- 3.9.1.2 Rising integration in hybrid and electric vehicles

- 3.9.1.3 Advancements in lightweight materials for better efficiency

- 3.9.1.4 Increasing focus on fuel efficiency and sustainability

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High costs associated with advanced KERS technologies

- 3.9.2.2 Limited adoption in low-cost vehicle segments

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.2.4 Others

- 5.3 Commercial vehicle

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By System, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Flywheel

- 6.3 Battery

- 6.4 Super capacitor

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 All-electric

- 7.3 PHEV

- 7.4 HEV

- 7.5 FCEV

Chapter 8 Market Estimates & Forecast, By KERS, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mechanical

- 8.3 Electro-mechanical

- 8.4 Hydraulic

- 8.5 Electronic

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Advics

- 10.2 Aisin

- 10.3 Bosch

- 10.4 Brembo

- 10.5 Continental

- 10.6 Denso

- 10.7 Haldex

- 10.8 Hitachi Astemo

- 10.9 Hyundai Mobis

- 10.10 Magna International

- 10.11 Mando

- 10.12 Nidec

- 10.13 PHINIA

- 10.14 Schaeffler

- 10.15 Skeleton Technologies

- 10.16 Tenneco

- 10.17 Torotrak

- 10.18 TRW Automotive

- 10.19 Valeo

- 10.20 ZF Friedrichshafen