|

市場調査レポート

商品コード

1684839

船舶推進システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Marine Propulsion Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 船舶推進システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月11日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

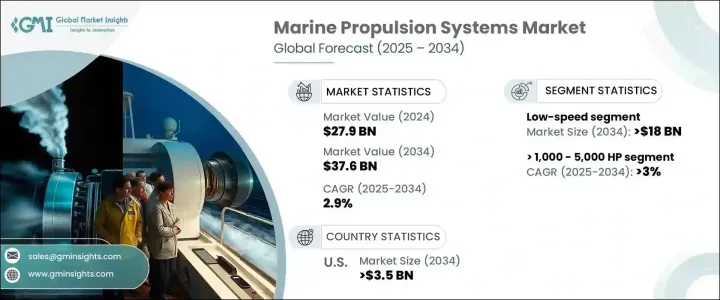

世界の船舶推進システム市場は、2024年に279億米ドルと評価され、2025年から2034年にかけてCAGR 2.9%で成長すると予測されています。

同市場の主な原動力は、世界の海上貿易の拡大と船隊規模の継続的な拡大であり、高度な推進技術に対する安定した需要に拍車をかけています。国際貿易が引き続き盛んになるにつれて、より大型の船舶とより重い貨物積載量を管理できる効率的で高性能の推進システムへのニーズが急増しています。

経済の世界化は、商品貿易を後押しするだけでなく、燃料効率を最大化し、運航コストを削減し、環境への影響を最小限に抑えるよう設計された最先端の推進システムの開発を加速させています。メーカー各社は、望ましい運航効率を維持しながら、進化する規制要件や持続可能性基準に合致するソリューションを生み出すことに重点を置いています。グリーンテクノロジーへの注目の高まりと業界内の脱炭素化の推進が、このダイナミックな市場情勢を形成する主要促進要因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 279億米ドル |

| 予測金額 | 376億米ドル |

| CAGR | 2.9% |

低速推進技術の採用は、市場の将来を形成する上で重要な役割を果たすと予想され、2034年までに180億米ドルの価値が見込まれます。この成長の原動力となっているのは、費用対効果の高い燃料に対する需要の高まりであり、これは長距離貿易航路や、燃料効率の高い船舶オプションに対する世界の依存度の高まりに直結しています。国際的な海事規制もこのシフトに重要な役割を果たしており、船主やオペレーターはより厳しい排出基準に適合するソリューションを求めています。排出規制区域(ECA)の拡大に伴い、よりクリーンで効率的な推進技術への投資は増加の一途をたどっています。加えて、造船部門は著しい進歩を遂げており、設計の革新性と持続可能性の両方を提供する船舶推進システムに対するニーズの高まりがさらに確実なものとなっています。

1,000~5,000馬力(HP)以上の船舶推進システムは、2034年までCAGR 3%で成長すると予測されます。これらのシステムは、その実証済みの効率性、耐久性、厳しい条件に耐える能力により、海事産業、特に貨物船、タンカー、ばら積み貨物船、コンテナ船で高く支持されています。環境の持続可能性への注目の高まりと海上貿易への依存の高まりは、このカテゴリーの成長に寄与する重要な要因です。技術の進歩により、性能が継続的に向上し、メンテナンス・コストが削減され、エネルギー効率が向上しているため、これらの推進システムは現在、環境フットプリントを最小限に抑えながら運航出力を最大化するために不可欠なものと見なされています。

米国の船舶推進システム市場は、2034年までに35億米ドルに達すると予測されています。高出力舶用エンジンへの投資の増加が、同国の厳しい環境基準を満たすように設計された、効率的で信頼性の高い推進ソリューションへの需要を促進しています。排ガス規制技術の継続的な採用は、これらのソリューションを支える重要な要因であり、メーカーは強力なエンジン出力を提供しながら規制を満たすことができます。これらのシステムは、重油を利用しながら回転速度を下げて大きな出力を提供できるため、その魅力が増しています。熱効率が向上するにつれて、これらの高性能推進システムは引き続き市場を牽引し、業界の持続的成長のための強力な基盤を築くことになります。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- ディーゼル

- 風力・ソーラー

- ガスタービン

- 燃料電池

- 蒸気タービン

- 天然ガス

- ハイブリッド

- その他

第6章 市場規模・予測:電力別、2021年~2034年

- 主要動向

- 1,000馬力以下

- 1,000~5,000馬力

- 5,000~10,000馬力

- 10,000~20,000馬力

- 20,000馬力以上

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 低速

- 中速

- 高速

第8章 市場規模・予測:推進別、2021年~2034年

- 主要動向

- 2ストローク

- 4ストローク

第9章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 商船

- コンテナ船

- タンカー

- バルクキャリア

- RO-RO船

- その他

- オフショア

- 掘削リグ&船舶

- アンカーハンドリング船

- オフショア支援船

- 浮体式生産ユニット

- プラットフォーム供給船

- クルーズ&フェリー

- クルーズ船

- 旅客船

- 客船・貨物船

- その他

- 海軍

- その他

第10章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- イタリア

- ノルウェー

- フランス

- ロシア

- デンマーク

- オランダ

- ベルギー

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ベトナム

- シンガポール

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- イラン

- アンゴラ

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

第11章 企業プロファイル

- AB Volvo Penta

- ABB

- Anglo Belgian Corporation

- Caterpillar

- Cummins

- DAIHATSU DIESEL

- Deere &Company

- DEUTZ

- Hyundai Heavy Industries

- IHI Power Systems

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Rolls-Royce

- Scania

- STX ENGINE

- Wärtsilä

- Weichai

- Yamaha Motor

- YANMAR HOLDINGS

The Global Marine Propulsion Systems Market was valued at USD 27.9 billion in 2024 and is set to grow at a CAGR of 2.9% from 2025 to 2034. The market is primarily driven by the expansion of global maritime trade and the continuous increase in fleet sizes, fueling a steady demand for advanced propulsion technologies. As international trade continues to flourish, the need for efficient, high-performance propulsion systems capable of managing larger vessels and heavier cargo loads has surged.

Economic globalization is not only boosting merchandise trade but also accelerating the development of cutting-edge propulsion systems designed to maximize fuel efficiency, reduce operational costs, and minimize environmental impact. Manufacturers are placing a strong focus on creating solutions that align with evolving regulatory requirements and sustainability standards while maintaining the desired operational efficiency. The growing focus on green technology and the push for decarbonization within the industry are key drivers shaping this dynamic market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.9 Billion |

| Forecast Value | $37.6 Billion |

| CAGR | 2.9% |

The adoption of low-speed propulsion technology is expected to play a significant role in shaping the future of the market, with an estimated value of USD 18 billion by 2034. This growth is fueled by the rising demand for cost-effective fuels, which is directly linked to long-distance trade routes and the increasing global reliance on fuel-efficient shipping options. International maritime regulations also play a critical role in this shift, as shipowners and operators seek solutions that comply with stricter emissions standards. As Emission Control Areas (ECAs) expand, investments in cleaner and more efficient propulsion technologies continue to rise. In addition, the shipbuilding sector is seeing significant advancements, further solidifying the growing need for marine propulsion systems that offer both innovation and sustainability in their design.

Marine propulsion systems in the >1,000 to 5,000 horsepower (HP) power range are projected to grow at a CAGR of 3% through 2034. These systems are highly favored in the maritime industry, particularly in cargo vessels, tankers, bulk carriers, and container ships, due to their proven efficiency, durability, and ability to withstand demanding conditions. The increased focus on environmental sustainability and the growing reliance on seaborne trade are significant factors contributing to the growth in this category. With technological advancements continuously improving performance, reducing maintenance costs, and enhancing energy efficiency, these propulsion systems are now seen as essential for maximizing operational output while minimizing the environmental footprint.

In the U.S. marine propulsion systems market, projections indicate a value of USD 3.5 billion by 2034. Rising investments in high-powered marine engines are driving the demand for efficient and reliable propulsion solutions designed to meet the country's stringent environmental standards. The continued adoption of emission control technologies is a key factor in supporting these solutions, allowing manufacturers to meet regulations while still providing powerful engine output. The ability of these systems to deliver substantial power at reduced rotational speeds while utilizing heavy fuel oil is increasing their appeal. As thermal efficiency improves, these high-performance propulsion systems continue to gain market traction, laying a strong foundation for sustained industry growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Wind & solar

- 5.4 Gas turbine

- 5.5 Fuel cell

- 5.6 Steam turbine

- 5.7 Natural gas

- 5.8 Hybrid

- 5.9 Others

Chapter 6 Market Size and Forecast, By Power, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 ≤ 1,000 HP

- 6.3 > 1,000 - 5,000 HP

- 6.4 > 5,000 - 10,000 HP

- 6.5 > 10,000 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 Medium speed

- 7.4 High speed

Chapter 8 Market Size and Forecast, By Propulsion, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 2- stroke

- 8.3 4- stroke

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (USD Million)

- 9.1 Key trends

- 9.2 Merchant

- 9.2.1 Container vessels

- 9.2.2 Tankers

- 9.2.3 Bulk carriers

- 9.2.4 RO-RO

- 9.2.5 Others

- 9.3 Offshore

- 9.3.1 Drilling RIGS & ships

- 9.3.2 Anchor handling vessels

- 9.3.3 Offshore support vessels

- 9.3.4 Floating production units

- 9.3.5 Platform supply vessels

- 9.4 Cruise & Ferry

- 9.4.1 Cruise vessels

- 9.4.2 Passenger vessels

- 9.4.3 Passenger/cargo vessels

- 9.4.4 Others

- 9.5 Navy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 Norway

- 10.3.5 France

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.3.8 Netherlands

- 10.3.9 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.4.7 Singapore

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Angola

- 10.5.5 Egypt

- 10.5.6 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 AB Volvo Penta

- 11.2 ABB

- 11.3 Anglo Belgian Corporation

- 11.4 Caterpillar

- 11.5 Cummins

- 11.6 DAIHATSU DIESEL

- 11.7 Deere & Company

- 11.8 DEUTZ

- 11.9 Hyundai Heavy Industries

- 11.10 IHI Power Systems

- 11.11 Kawasaki Heavy Industries

- 11.12 MAN Energy Solutions

- 11.13 Mitsubishi Heavy Industries

- 11.14 Rolls-Royce

- 11.15 Scania

- 11.16 STX ENGINE

- 11.17 Wärtsilä

- 11.18 Weichai

- 11.19 Yamaha Motor

- 11.20 YANMAR HOLDINGS