|

市場調査レポート

商品コード

2027492

糖蜜の市場機会、成長要因、業界動向分析、および2026年~2035年の予測Molasses Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 糖蜜の市場機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月10日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

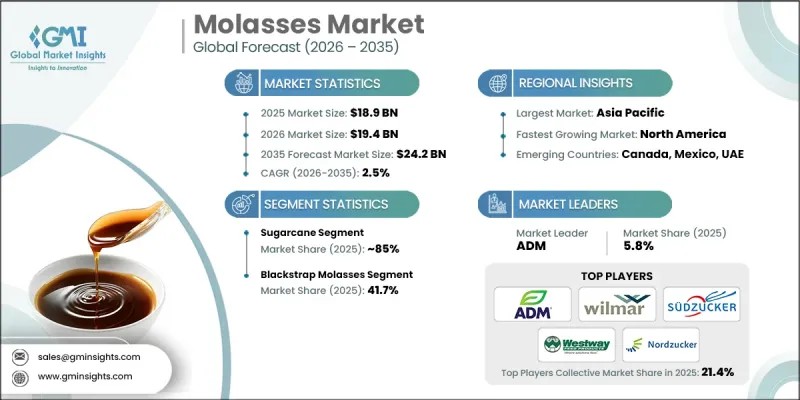

世界の糖蜜市場は2025年に189億米ドルと評価され、2035年までにCAGR 2.5%で成長し、242億米ドルに達すると推定されています。

飲食品・動物飼料、バイオ燃料産業における利用拡大により、市場は拡大を続けています。飲食品分野では、糖蜜は焼き菓子、菓子類、飲料の配合において天然の甘味料や風味増強剤として広く使用されており、加工食品製造における安定した需要を支えています。植物由来の食事に対する消費者の嗜好の高まりは、精製糖ベースの原料の代替品としての糖蜜の役割をさらに強化しています。飼料産業においては、糖蜜はその高エネルギー含有量と嗜好性が高く評価されており、飼料効率と家畜の生産性向上に寄与しています。バイオ燃料部門も重要な成長分野であり、ここでは糖蜜がエタノール生産のための費用対効果の高い原料として使用されています。持続可能性の動向が市場をますます形作っており、メーカーは環境に配慮した生産手法に注力しています。砂糖価格の変動やサトウキビ栽培における天候関連の混乱が供給面の課題を生み出しているもの、産業用途の拡大により需要は堅調に推移しています。技術の進歩と加工効率の向上により、生産量はさらに増加し、コストが削減され、各最終用途産業において一貫した製品品質が確保されています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時点の市場規模 | 189億米ドル |

| 予測額 | 242億米ドル |

| CAGR | 2.5% |

サトウキビセグメントは2025年に85%のシェアを占め、2035年までCAGR2.5%で着実な成長を維持すると予想されています。その優位性は、主に熱帯および亜熱帯地域における大規模な栽培に起因しており、これらの地域では好ましい気候条件が高収量生産を支えています。サトウキビは入手が容易で費用対効果が高いため、世界の産業において糖蜜の最も重要な原料源となっています。その安定した供給基盤は、食品、飼料、および工業用途における安定した生産を保証し、市場構造における主導的な地位を強固なものにしています。

ブラックストラップ・モラセス部門は、その優れた栄養プロファイルと深い風味特性に支えられ、2025年には41.7%のシェアを占めました。この種類のモラセスは、鉄やカルシウムを含むミネラル含有量が高いため、食品加工や動物栄養用途で広く利用されています。その機能性と栄養上の利点は、日々の食事においてより自然な代替原料を求める健康志向の消費者からの支持が高まっていることにも寄与しています。

北米の糖蜜市場は、2026年から2035年にかけてCAGR2.3%で成長すると予測されています。この地域の成長は、飲食品業界全体における天然甘味料や機能性食品原料への需要増加によって牽引されています。クリーンラベル製品や植物由来製品に対する消費者の意識の高まりも、市場の拡大をさらに後押ししています。さらに、酵素抽出や発酵を基盤とした方法を含む加工技術の進歩により、同地域の製造施設全体で製品の品質が向上し、生産効率も改善されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 飲食品業界における需要の増加

- 飼料生産の成長

- バイオ燃料セクター、特にエタノール生産の拡大

- 業界の潜在的リスク&課題

- 砂糖価格の変動および天候による生産への影響

- 市場機会

- 天然甘味料への需要の高まりと健康上の利点

- 飼料およびバイオ燃料産業における利用拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 今後の市場動向

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:ソース別、2022-2035

- サトウキビ

- テンサイ

- その他

第6章 市場推計・予測:タイプ別、2022-2035

- サトウキビ

- テンサイ

- その他

第7章 市場推計・予測:カテゴリー別、2022-2035

- 有機

- 従来型

第8章 市場推計・予測:形態別、2022-2035

- 液体

- 粉末

第9章 市場推計・予測:用途別、2022-2035

- 飲食品

- ベーカリー・菓子類

- ソース、スープ、マリネ

- 飲料

- 乳製品

- その他(朝食用シリアル、お粥、即席食品)

- 動物用飼料

- 家畜用飼料

- 家禽用飼料

- ペットフード

- 医薬品・パーソナルケア

- 栄養補助食品

- 医薬品

- 化粧品・パーソナルケア

- 産業用途

- バイオ燃料/エタノール生産

- 発酵産業

- 化学工業

- その他(インク、塗料、微生物培養培地)

- その他

第10章 市場推計・予測:包装形態別、2022-2035

- ボトル

- パウチ

- バルク/工業用包装

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第12章 企業プロファイル

- ADM

- Amalgamated Sugar

- American Crystal Sugar Company

- B &G Foods

- Cosun Beet Company

- Crosby Molasses Co., Ltd

- International Molasses Corporation

- Michigan Sugar Company

- Nordzucker

- Sudzucker

- Westway Feed Products

- Wilmar International Limited