|

市場調査レポート

商品コード

1928948

電動二輪車市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Electric Two-wheeler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 電動二輪車市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月13日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

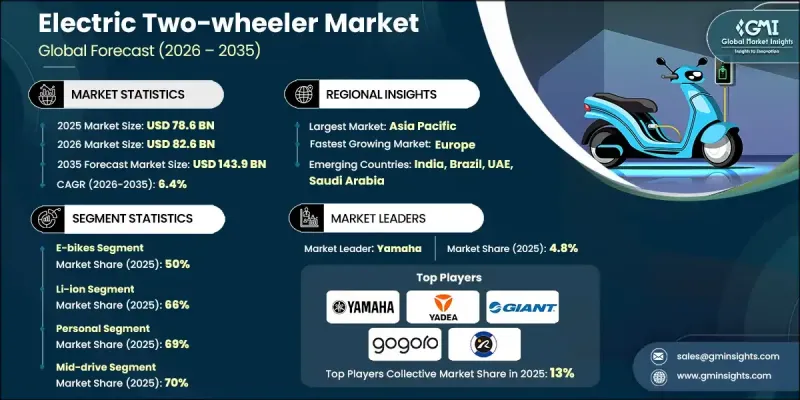

世界の電動二輪車市場は、2025年に786億米ドルと評価され、2035年までにCAGR 6.4%で成長し、1,439億米ドルに達すると予測されています。

大気汚染の悪化や気候変動に関連する課題への認識が高まる中、消費者はよりクリーンな移動手段への移行を促進されています。排気ガスを排出しない電動二輪車は、個人の炭素排出量を削減する現実的な手段としてますます注目され、先進国と新興国双方における持続可能性目標の達成を支援しています。政府が導入する財政的インセンティブにより初期費用が軽減され、手頃な価格が実現されることで、公共政策は普及促進において引き続き重要な役割を果たしております。バッテリーシステムの継続的な革新により、エネルギー密度の向上、充電時間の短縮、耐久性の改善を通じて車両効率が向上しています。インテリジェントな接続機能や先進的なブレーキシステムを含む追加の技術的アップグレードにより、全体的な使いやすさが向上しています。これらの複合的な要因が消費者の信頼を高め、対象顧客層を拡大しており、電動二輪車は従来の燃料駆動型車両に代わる現実的な選択肢として位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 786億米ドル |

| 予測金額 | 1,439億米ドル |

| CAGR | 6.4% |

電動自転車セグメントは2025年に50%のシェアを占め、2035年までCAGR6.5%で成長すると予測されています。この成長は、アシスト付き移動手段、環境に優しい通勤手段、ライフスタイル志向の交通ソリューションに対する消費者の嗜好の高まりによって推進されています。電動自転車は、利便性、自動車に代わる費用対効果の高い選択肢、環境に配慮した移動手段を求める都市部の通勤者に支持されています。さらに、フィットネス志向のサイクリングやレクリエーションとしてのアウトドア活動への関心の高まりが、普及をさらに後押ししています。

リチウムイオン電池セグメントは2025年に66%のシェアを占め、2026年から2035年にかけてCAGR6%で成長すると予想されています。このセグメントの成長は、高いエネルギー密度、延長された稼働距離、高速充電能力、そして生産コストの低下によって推進されています。バッテリー管理システム、熱制御、セル耐久性の改善により安全性と性能が向上し、リチウムイオン技術はほとんどの電動二輪車メーカーにとって最適な選択肢となっております。

中国電動二輪車市場は2025年に40%のシェアを占め、242億米ドルの市場規模を生み出しました。補助金、免税措置、購入リベートなどの強力な政府インセンティブと、大規模な普及促進施策が相まって、所有コストを大幅に引き下げ、消費者の購入意欲を後押ししています。クリーンモビリティを推進する都市政策と充電インフラの急速な拡充が相まって、同国における電動二輪車の成長はさらに加速し、中国は地域をリードする市場としての地位を確立しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 政府の支援と優遇措置

- 技術的進歩

- 環境意識

- 都市部の移動手段と交通渋滞

- 業界の潜在的リスク&課題

- 初期費用が高額

- 充電インフラ

- 市場機会

- アジア太平洋地域における採用拡大

- 電動スクーター及び自転車シェアリング

- OEMパートナーシップとイノベーション

- 新興市場における事業拡大

- 成長可能性分析

- 規制情勢

- 北米

- 米国国家道路交通安全局(NHTSA)規制

- 環境保護庁(EPA)排出基準

- カリフォルニア州大気資源局(CARB)基準

- 欧州

- 欧州連合一般安全規制(EU GSR)

- EU廃車指令(ELV)

- 欧州委員会乗用車安全基準

- 欧州連合(EU)型式承認プロセス

- アジア太平洋地域

- 中国国家車両安全基準

- インド規格局(BIS)エアバッグ規制

- 国土交通省(MLIT)規制

- ASEAN道路安全基準

- ラテンアメリカ

- ブラジル国家交通局(DENATRAN)規格

- アルゼンチン国家道路安全庁(ANSV)規制

- メキシコ通信運輸省(SCT)規制

- メルコスールにおける自動車安全基準の調和

- 中東・アフリカ

- アラブ首長国連邦連邦自動車安全法

- サウジアラビア規格機構(SASO)車両安全規制

- 南アフリカ規格局(SABS)自動車規制

- 北米

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出入

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:車両別、2022-2035

- 電動バイク

- 電動スクーター

- 電動自転車

- 電動キックボード

第6章 市場推計・予測:バッテリー別、2022-2035

- SLA

- リチウムイオン電池

- その他

第7章 市場推計・予測:モーター別、2022-2035

- ミッドドライブ

- ハブ

- その他

第8章 市場推計・予測:モーター出力別、2022-2035

- 3.5kW未満

- 3.5 kW~6.5 kW

- 6.5kW超

第9章 市場推計・予測:電圧別、2022-2035

- 48V

- 60 V

- 72V

- その他

第10章 市場推計・予測:最終用途別、2022-2035

- 個人向け

- 商業用

- シェアードモビリティ

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- デンマーク

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ地域

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第12章 企業プロファイル

- 世界プレイヤー

- Autoliv

- Bosch

- Continental

- Daicel

- Delphi

- Denso

- Hyundai Mobis

- Joyson Safety Systems

- ZF

- Ather

- Giant

- Gogoro

- Hero Electric

- Jiangsu Xinri E-Vehicle

- Niu Technologies

- Ola

- VMOTO SOCO

- Yadea

- Yamaha Motor Company

- 地域プレイヤー

- ARC Automotive

- Ashimori Industry

- ITW Automotive

- Kolon Industries

- Nippon Kayaku

- Seiren

- Toyoda Gosei

- 新興企業

- Jinheng Automotive Safety Technology

- Nihon Plast

- Swicofil

- Tenaris