モバイルブロードバンドインフラ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Mobile Broadband Infrastructure Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684724

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

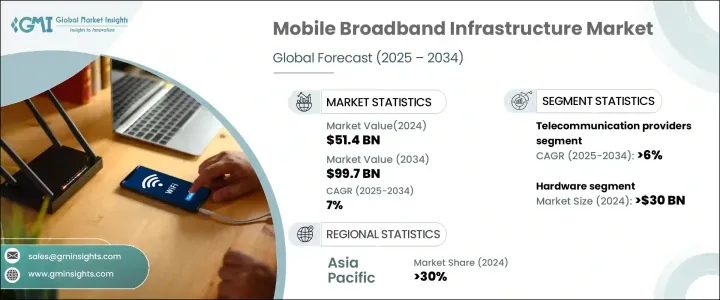

世界のモバイルブロードバンドインフラ市場は、2024年に514億米ドルに達し、2025~2034年にかけてCAGR 7%で力強い成長が見込まれています。

この成長の主要要因は、5Gネットワークの急速な拡大と、特に新興経済圏における4G LTEカバレッジの強化を目的とした多額の投資です。モバイル機器の利用が増え続け、動画ストリーミングやIoTアプリケーションの普及に伴い、通信サービスへの需要が急増しています。こうした動向は、増大するデータトラフィックと接続要件に対応するため、より先進的ネットワークインフラの必要性を高めています。モバイルブロードバンドインフラ市場は、特にモバイルネットワークがまだ開発段階にある地域において、ユーザーや企業が信頼性の高い高速インターネットアクセスを確保する上で重要な役割を果たしています。増大するデータ消費とデバイス接続をサポートする能力が重要であり、インフラのアップグレードと拡大は世界中の通信会社にとって最優先事項となっています。

この市場の成長を牽引する主要なコンポーネントのひとつがハードウェアセグメントで、2024年には300億米ドルを占めます。最新のモバイルネットワークでは、5G以降の高電力、低遅延、スケーラビリティの要求を満たすために、ますます先進的システムが要求されるため、ハードウェアソリューションに対する需要は引き続き高いです。ネットワークインフラは、データ転送とデバイス接続の大幅な増加に対応しなければならないため、信頼性の高い高性能ハードウェアが必要となります。通信事業者が5Gのような先進的技術を展開するにつれて、堅牢なハードウェアソリューションに対するこのようなニーズの高まりはエスカレートすると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 514億米ドル |

| 予測金額 | 997億米ドル |

| CAGR | 7% |

モバイルブロードバンドインフラ市場は、エンドユーザーによって通信プロバイダー、企業、政府機関に分けられます。特に通信事業者は安定した成長が見込まれ、2025~2034年にかけてのCAGRは6%と予測されます。ビデオストリーミング、IoT統合、リアルタイム通信など、データを多用する活動に後押しされ、ネットワーク容量拡大への需要が高まっているため、通信事業者はネットワークのアップグレードに多額の投資を行うようになっています。このような投資は、カバーエリアの拡大と帯域幅能力の向上に不可欠であり、通信サービスが消費者や企業の高まる需要に確実に応えられるようにするものです。

2024年の市場シェアは、中国を筆頭にアジア太平洋が30%を占めます。中国政府は技術インフラ、特に5Gネットワークの展開に積極的な投資を行っており、同国はネットワーク拡大における世界的リーダーとしての地位を確立しています。中国の技術大手は5G基地局の大規模展開の先頭に立っており、この地域のインフラ開発に大きく貢献しています。この急速な進展により、中国は自国市場の主要参入企業としてだけでなく、世界のモバイルブロードバンドインフラソリューションの主要サプライヤーとしても位置づけられています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- 部品メーカー

- メーカー

- 流通業者

- エンドユーザー

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要国のモバイルインターネットユーザー普及率(2024年)

- 携帯電話ネットワーク接続統計(2024年)

- 規制状況

- 影響要因

- 促進要因

- スマートデバイスやIoTの拡大による高速接続への需要の高まり

- インフラ能力を高める5Gネットワークの採用加速

- ネットワークのアップグレードと拡大に対する通信事業者の投資の増加

- 遠隔地やサービスが行き届いていない地域でのモバイル衛星サービスへの依存の高まり

- クラウドコンピューティングとエッジコンピューティングの進歩による強固なネットワーク要件

- 産業の潜在的リスク・課題

- 先進的インフラを導入するための高額な資本コスト

- 技術展開を遅らせる規制とコンプライアンスのハードル

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:コンポーネント別、2021~2034年

- 主要動向

- ハードウェア

- アンテナ&トランシーバー

- リモートラジオユニット(RRU)

- ベースバンドユニット(BBU)

- フィルター&デュプレクサー

- パワーアンプ

- その他

- ソフトウェア

- ネットワーク管理システム

- 運用支援システム(OSS)

- 業務支援システム(BSS)

- ネットワーク機能仮想化(NFV)

- その他

- サービス

- ネットワークコンサルティング

- インテグレーション&展開

- サポート&メンテナンス

第6章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 3G

- 4G

- 5G

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 通信事業者

- 企業

- 政府機関

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Altiostar Networks

- Arista Networks

- Aviat Networks

- Cambium Networks

- Ciena

- Cisco Systems

- CommScope

- Ericsson

- FiberHome

- Fujitsu

- Huawei Technologies

- Juniper Networks

- Mavenir Systems

- NEC

- Nokia

- Parallel Wireless

- Qualcomm

- Radwin

- Samsung Electronics

- ZTE

目次

The Global Mobile Broadband Infrastructure Market reached USD 51.4 billion in 2024 and is expected to experience robust growth at a CAGR of 7% from 2025 to 2034. This growth is largely driven by the rapid expansion of 5G networks and significant investments aimed at enhancing 4G LTE coverage, particularly in emerging economies. As mobile device usage continues to rise, along with video streaming and the proliferation of IoT applications, the demand for telecom services has surged. These trends are intensifying the need for more advanced network infrastructure to handle the increasing volume of data traffic and connectivity requirements. The mobile broadband infrastructure market plays a vital role in ensuring that users and businesses have reliable, high-speed access to the Internet, especially in regions where mobile networks are still in the development phase. The ability to support growing data consumption and device connectivity is key, making infrastructure upgrades and expansion a top priority for telecom companies worldwide.

One of the primary components driving the growth of this market is the hardware segment, which accounted for USD 30 billion in 2024. The demand for hardware solutions remains strong as modern mobile networks require increasingly advanced systems to meet the higher power, lower latency, and scalability demands of 5G and beyond. Network infrastructure must handle substantial increases in data transfer and device connectivity, which requires highly reliable, high-performance hardware. This growing need for robust hardware solutions is expected to escalate as telecom providers roll out more advanced technologies like 5G.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $51.4 Billion |

| Forecast Value | $99.7 Billion |

| CAGR | 7% |

When it comes to end users, the mobile broadband infrastructure market is divided into telecommunications providers, enterprises, and government sectors. Telecom providers, in particular, are expected to experience steady growth, with a projected CAGR of 6% between 2025 and 2034. The demand for greater network capacity, driven by data-heavy activities such as video streaming, IoT integration, and real-time communications, is pushing telecom companies to heavily invest in upgrading their networks. These investments are essential to expanding coverage areas and improving bandwidth capabilities, ensuring that telecom services can meet the rising demands of consumers and businesses alike.

The Asia Pacific region held a dominant 30% market share in 2024, with China playing a leading role. The Chinese government's aggressive investment in advancing its technological infrastructure, particularly in the deployment of 5G networks, has positioned the country as a global leader in network expansion. Chinese technology giants are spearheading the large-scale rollout of 5G base stations, contributing significantly to the region's infrastructure development. This rapid progress has positioned China not only as a key player in its own market but also as a major supplier of mobile broadband infrastructure solutions worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Mobile internet user penetration rate in major countries, 2024

- 3.7 Cellular network connection statistics, 2024

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for high-speed connectivity due to smart devices and IoT expansion

- 3.9.1.2 Accelerated adoption of 5G networks boosting infrastructure capabilities

- 3.9.1.3 Increased telecom investments in network upgrades and expansion

- 3.9.1.4 Growing reliance on mobile satellite services for remote and underserved regions

- 3.9.1.5 Advances in cloud and edge computing driving robust network requirements

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High capital costs for deploying advanced infrastructure

- 3.9.2.2 Regulatory and compliance hurdles delaying technology rollouts

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Antennas & transceivers

- 5.2.2 Remote Radio Units (RRU)

- 5.2.3 Baseband Units (BBU)

- 5.2.4 Filters & duplexers

- 5.2.5 Power amplifiers

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Network management systems

- 5.3.2 Operation Support Systems (OSS)

- 5.3.3 Business Support Systems (BSS)

- 5.3.4 Network Function Virtualization (NFV)

- 5.3.5 Others

- 5.4 Services

- 5.4.1 Network consulting

- 5.4.2 Integration & deployment

- 5.4.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 3G

- 6.3 4G

- 6.4 5G

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Telecommunications providers

- 7.3 Enterprises

- 7.4 Government

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Altiostar Networks

- 9.2 Arista Networks

- 9.3 Aviat Networks

- 9.4 Cambium Networks

- 9.5 Ciena

- 9.6 Cisco Systems

- 9.7 CommScope

- 9.8 Ericsson

- 9.9 FiberHome

- 9.10 Fujitsu

- 9.11 Huawei Technologies

- 9.12 Juniper Networks

- 9.13 Mavenir Systems

- 9.14 NEC

- 9.15 Nokia

- 9.16 Parallel Wireless

- 9.17 Qualcomm

- 9.18 Radwin

- 9.19 Samsung Electronics

- 9.20 ZTE

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日