|

市場調査レポート

商品コード

1698296

エピジェネティクス診断市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Epigenetics Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エピジェネティクス診断市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月26日

発行: Global Market Insights Inc.

ページ情報: 英文 133 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

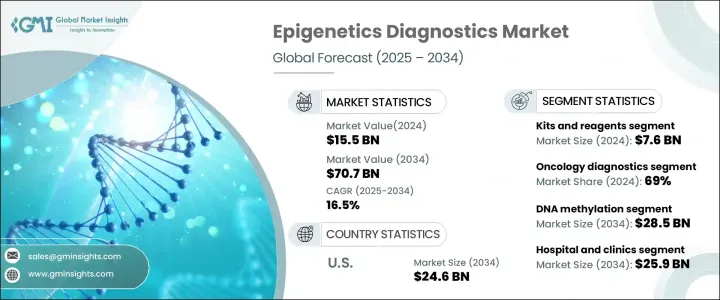

世界のエピジェネティクス診断市場は、2024年に155億米ドルと評価され、2025年から2034年にかけて16.5%のCAGRを記録する見通しです。

この急速な拡大は、エピジェネティックな修飾が疾患の開発と進行の主要な要因であるとの認識が高まっていることが大きな要因となっています。様々な健康状態におけるDNAメチル化、ヒストン修飾、ノンコーディングRNAの役割に関する調査が深まるにつれ、高度な診断ツールに対する需要が急激に高まっています。

近年、精密医療の普及と分子診断の技術進歩が相まって、市場の拡大が著しく加速しています。エピジェネティック解析における人工知能と機械学習の統合は、診断ソリューションの精度と効率をさらに高めています。さらに、大手製薬企業やバイオテクノロジー企業は、新規エピジェネティックバイオマーカーを開発するための研究開発に多額の投資を行っており、業界をさらに前進させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 155億米ドル |

| 予測金額 | 707億米ドル |

| CAGR | 16.5% |

科学的発見を実際の臨床応用につなげる上で、研究機関とヘルスケアプロバイダーとの協力関係の拡大も極めて重要な役割を果たしています。疾病の早期発見と個別化医療の改善を目的とした資金提供や政府のイニシアチブの増加は、この分野での技術革新を促進しています。がんや神経変性疾患などの慢性疾患の増加に伴い、エピジェネティック診断の関連性は高まり続けており、今後10年間は市場が持続的に拡大する可能性があります。

市場は、キット・試薬、機器、ソフトウェア、サービスなどの主要製品カテゴリーに区分されます。2024年には、これらの製品の世界市場は134億米ドルに達し、キットと試薬のセグメントが76億米ドルで圧倒的なシェアを占めています。これらの診断ツールは、臨床応用、学術研究、医薬品開発において不可欠なものとなっています。その人気の高まりは、ユーザーフレンドリーな設計、アッセイ感度の向上、自動化機能、次世代シーケンシング(NGS)やポリメラーゼ連鎖反応(PCR)のような最先端プラットフォームとの互換性に起因しています。業界がよりハイスループットでコスト効率に優れたソリューションに移行するにつれ、信頼性が高く効率的なキットへの需要は高まり続けています。

エピジェネティクス診断のアプリケーションは腫瘍学と非腫瘍学に分類され、腫瘍学が2024年に69%のシェアを占める。このセグメントの優位性は、がんの早期発見に対するニーズの高まりと、様々な悪性腫瘍の診断および治療におけるエピジェネティクスバイオマーカーの重要性の高まりに大きく起因しています。DNAメチル化パターン、ヒストン修飾、クロマチンリモデリングの変化は、がん発症の極めて重要な指標として浮上しており、より正確で個別化された治療アプローチを可能にしています。がんの世界の負担の増加とバイオマーカー研究の継続的な進歩により、腫瘍学セグメントは市場成長の主要な促進要因であり続けています。

米国のエピジェネティクス診断市場は、2034年までCAGR 16.5%で成長し、予測期間終了時には246億米ドルに達すると予測されています。同国は、その強固なヘルスケアインフラ、広範な研究開発イニシアティブ、精密医療の早期導入により、この業界におけるフロントランナーであり続けています。米国国立衛生研究所(NIH)を含む政府機関は、エピジェネティクスの画期的な研究に資金を提供し続けており、イノベーションと商業化をさらに加速させています。慢性疾患の有病率の上昇、バイオテクノロジー企業からの投資の増加、および有利な規制状況は、米国を世界のエピジェネティクス診断ランドスケープにおける支配的なプレーヤーとしてさらに強固なものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- がんと慢性疾患の有病率の増加

- エピゲノム研究と技術の進歩

- 非侵襲的診断への需要の高まり

- 業界の潜在的リスク&課題

- エピジェネティック診断技術の高コスト

- 検査方法の標準化が限定的

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- キットおよび試薬

- 器具

- ソフトウェアとサービス

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- オンコロジー診断

- 非オンコロジー診断

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- DNAメチル化

- ヒストンメチル化

- マイクロRNA修飾

- クロマチン構造

- その他の技術

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院・クリニック

- 製薬・バイオテクノロジー企業

- 診断研究所

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abcam

- Agilent Technologies

- Diagenode

- Dovetail Genomics

- Element Biosciences

- Illumina

- Merck

- New England Biolabs

- PacBio

- Promega

- QIAGEN

- Roche Diagnostics

- Thermo Fisher Scientific

- Zymo Research

The Global Epigenetics Diagnostics Market was valued at USD 15.5 billion in 2024 and is poised to register a CAGR of 16.5% from 2025 to 2034. This rapid expansion is largely fueled by the increasing recognition of epigenetic modifications as key contributors to disease development and progression. As research deepens into the role of DNA methylation, histone modifications, and non-coding RNAs in various health conditions, the demand for advanced diagnostic tools is rising exponentially.

In recent years, the widespread adoption of precision medicine, coupled with technological advancements in molecular diagnostics, has significantly accelerated market expansion. The integration of artificial intelligence and machine learning in epigenetic analysis has further enhanced the accuracy and efficiency of diagnostic solutions. Additionally, major pharmaceutical and biotechnology companies are investing heavily in R&D to develop novel epigenetic biomarkers, further propelling the industry forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $70.7 Billion |

| CAGR | 16.5% |

Growing collaborations between research institutions and healthcare providers are also playing a pivotal role in translating scientific discoveries into real-world clinical applications. The increased availability of funding and government initiatives aimed at improving early disease detection and personalized medicine is driving innovation in the field. With the rise in chronic diseases, including cancer and neurodegenerative disorders, the relevance of epigenetic diagnostics continues to grow, positioning the market for sustained expansion over the next decade.

The market is segmented into key product categories, including kits and reagents, instruments, software, and services. In 2024, the global market for these products reached USD 13.4 billion, with the kits and reagents segment dominating at USD 7.6 billion. These diagnostic tools have become indispensable in clinical applications, academic research, and pharmaceutical development. Their growing popularity stems from their user-friendly designs, enhanced assay sensitivity, automation capabilities, and compatibility with cutting-edge platforms like next-generation sequencing (NGS) and polymerase chain reaction (PCR). As the industry moves toward more high-throughput and cost-effective solutions, the demand for reliable and efficient kits continues to escalate.

The application landscape of epigenetics diagnostics is categorized into oncology and non-oncology segments, with oncology commanding a substantial 69% share in 2024. The dominance of this segment is largely attributed to the growing need for early cancer detection and the rising importance of epigenetic biomarkers in diagnosing and treating various malignancies. Changes in DNA methylation patterns, histone modifications, and chromatin remodeling have emerged as crucial indicators of cancer development, enabling more precise and personalized treatment approaches. With the increasing global burden of cancer and continued advancements in biomarker research, the oncology segment remains a major driver of market growth.

The U.S. Epigenetics Diagnostics Market is projected to grow at a CAGR of 16.5% through 2034, reaching USD 24.6 billion by the end of the forecast period. The country remains a frontrunner in this industry, thanks to its robust healthcare infrastructure, extensive research and development initiatives, and early adoption of precision medicine. Government agencies, including the National Institutes of Health (NIH), continue to fund breakthrough research in epigenetics, further accelerating innovation and commercialization. The rising prevalence of chronic diseases, increasing investments from biotech firms, and favorable regulatory policies are further cementing the U.S. as a dominant player in the global epigenetics diagnostics landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cancer and chronic diseases

- 3.2.1.2 Advancements in epigenomics research and technology

- 3.2.1.3 Growing demand for non-invasive diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of epigenetic diagnostics technologies

- 3.2.2.2 Limited standardization of testing methods

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Kits and reagents

- 5.3 Instruments

- 5.4 Software and services

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology diagnostics

- 6.3 Non-oncology diagnostics

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 DNA methylation

- 7.3 Histone methylation

- 7.4 MicroRNA modification

- 7.5 Chromatin structures

- 7.6 Other technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital and clinics

- 8.3 Pharmaceutical and biotechnology companies

- 8.4 Diagnostic laboratories

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abcam

- 10.2 Agilent Technologies

- 10.3 Diagenode

- 10.4 Dovetail Genomics

- 10.5 Element Biosciences

- 10.6 Illumina

- 10.7 Merck

- 10.8 New England Biolabs

- 10.9 PacBio

- 10.10 Promega

- 10.11 QIAGEN

- 10.12 Roche Diagnostics

- 10.13 Thermo Fisher Scientific

- 10.14 Zymo Research