|

市場調査レポート

商品コード

1684720

自転車用メカニカルディスクブレーキ市場の機会、成長促進要因、産業動向分析、2025~2034年予測Bicycle Mechanical Disc Brake Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自転車用メカニカルディスクブレーキ市場の機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年01月17日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

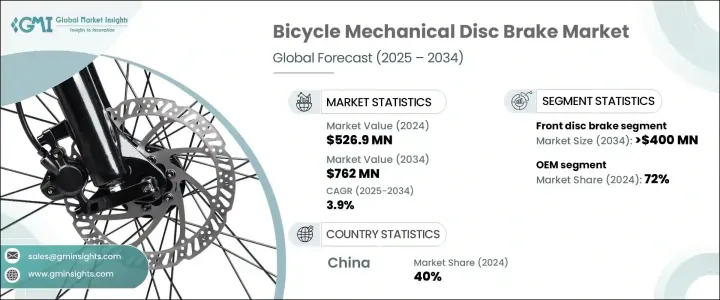

自転車用メカニカルディスクブレーキの世界市場は、2024年に5億2,690万米ドルに達し、2025年から2034年にかけてCAGR 3.9%で成長すると予測されています。

持続可能な交通手段へのシフトが進んでいることが、この市場を前進させる主な要因です。世界各国の政府はサイクリング・インフラに投資し、自動車に代わる有効な手段として自転車を推進しています。自転車専用レーン、サイクリストへの税制優遇措置、電動自転車への補助金などがサイクリングをより身近なものにし、最終的にメカニカルディスクブレーキの需要を押し上げています。都市化が加速し、環境への関心が高まるなか、自転車は日常的な移動手段として好まれるようになりました。サイクリングを楽しむ人が増えるにつれて、信頼性の高いブレーキシステムへのニーズは高まり続けています。

消費者は、その効率性、耐久性、費用対効果から、機械式ディスクブレーキを装備した自転車を選ぶようになっています。油圧式ブレーキとは異なり、機械式ディスクブレーキはメンテナンスの手間が少なく、さまざまな地形や気象条件でも安定した性能を発揮します。この信頼性により、レクリエーションと通勤の両方のサイクリストにとって理想的な選択肢となっています。また、フィットネスやレジャーを目的としたサイクリングの人気が高まっており、ライダーが安全性と制御性を確保できるブレーキシステムを求めていることも、市場拡大に寄与しています。さらに、軽量素材や改良されたパッド化合物などのブレーキ技術の進歩が性能を向上させ、普及をさらに後押ししています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5億2,690万米ドル |

| 予測金額 | 7億6,200万米ドル |

| CAGR | 3.9% |

電動自転車は、自転車用メカニカルディスクブレーキ市場を牽引する重要な役割を果たしています。メカニカルディスクブレーキは、さまざまな速度や負荷の下でも信頼できる制動力を発揮するため、e-bikeに好んで使用されています。多くの政府、特に欧州では、グリーン交通イニシアチブの一環としてe-bike採用にインセンティブを与えています。こうした奨励策と電動モビリティへの嗜好の高まりが相まって、メカニカルディスクブレーキの需要に拍車をかけています。e-bikeが主流の交通機関に移行するにつれて、メーカーは先進的なブレーキシステムを統合し続け、ライダーの安全性と性能を確保しています。

市場はブレーキタイプ別にフロント・ディスクブレーキとリア・ディスクブレーキに区分されます。フロント・ディスク・ブレーキは2024年に市場シェアの60%を占め、2034年までに4億米ドルを生み出すと予測されています。高性能自転車に対する消費者の需要がこの成長を後押ししています。フロントディスクブレーキは優れた制動力を発揮し、厳しい条件下でもコントロールしやすいからです。険しい地形を進むにせよ、雨天のサイクリングにせよ、これらのブレーキはライダーの安定性と安全性を高めています。マウンテンバイクやオフロード・サイクリングの増加は、耐久性と制御性を確保する高精度ブレーキ技術への需要をさらに高めています。

自転車用メカニカルディスクブレーキの流通経路はOEMとアフターマーケットに分けられ、2024年にはOEMが72%の圧倒的シェアを占めています。自転車メーカーはOEMブレーキ・サプライヤーとの提携を増やし、工場から直接最新のブレーキ技術をモデルに装備するようになっています。こうした提携により、ブランドは高性能の機械式ディスクブレーキを生産ラインに組み込むことができ、新しい自転車が最新の安全基準と効率基準を満たすことを保証できます。プレミアム自転車に対する消費者の期待が高まるなか、OEM販売は力強い勢いを維持し、市場の成長を確固たるものにすると予想されます。

中国は、世界の自転車用メカニカルディスクブレーキ市場において支配的な地位を維持しており、2024年にはシェアの40%を占めています。同国は持続可能なモビリティと自動車排出量の削減に重点を置いているため、特に都市部で自転車の普及が進んでいます。中国では、通勤とレクリエーションの両面でサイクリング文化が根付いているため、高品質のブレーキシステムに対する需要が一貫して高まっています。環境に優しい輸送ソリューションを推進する政府の政策がこの市場をさらに後押しし、中国はメカニカルディスクブレーキの生産と技術革新の重要な拠点となっています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料プロバイダー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 最終顧客

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 価格分析

- 影響要因

- 促進要因

- 世界の自転車普及率の上昇

- 環境意識が環境に優しい交通手段への移行を促す

- ブレーキ部品の技術進歩

- サイクリング・インフラを支援する政府の取り組み

- 業界の潜在的リスク&課題

- 高い競合と価格敏感性

- 油圧ディスクブレーキへのシフト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ブレーキ別、2021年~2034年

- 主要動向

- フロントディスクブレーキ

- リアディスクブレーキ

第6章 市場推計・予測:オファリング別、2021年~2034年

- 主要動向

- シングルピストン

- デュアルピストン

- 4ピストン

- マルチピストン

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ロードバイク

- マウンテンバイク

- レーシングバイク

- グラベルバイク

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Box Components

- Campagnolo

- Cane Creek

- Clarks Cycle Systems

- Formula

- Funn Components

- Hayes

- Hope Technology

- Jagwire

- KMC

- Magura

- Nutt

- Promax

- RockShox

- Shimano

- SRAM

- SunRace

- Tektro

- XLC

- Zoom

The Global Bicycle Mechanical Disc Brake Market reached USD 526.9 million in 2024 and is set to grow at a CAGR of 3.9% between 2025 and 2034. The increasing shift toward sustainable transportation is a major factor driving this market forward. Governments worldwide are investing in cycling infrastructure, promoting bicycles as a viable alternative to cars. Dedicated bike lanes, tax incentives for cyclists, and subsidies for electric bicycles are making cycling more accessible, ultimately boosting demand for mechanical disc brakes. With urbanization accelerating and environmental concerns on the rise, bicycles have become a preferred mode of daily travel. As more people turn to cycling, the need for reliable braking systems continues to grow.

Consumers are increasingly opting for bicycles equipped with mechanical disc brakes due to their efficiency, durability, and cost-effectiveness. Unlike hydraulic brakes, mechanical disc brakes require less maintenance and offer consistent performance across various terrains and weather conditions. This reliability makes them an ideal choice for both recreational and commuter cyclists. The growing popularity of cycling for fitness and leisure also contributes to market expansion, as riders seek braking systems that ensure safety and control. Additionally, advancements in brake technology, such as lightweight materials and improved pad compounds, enhance performance, further driving adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $526.9 Million |

| Forecast Value | $762 Million |

| CAGR | 3.9% |

Electric bicycles are playing a significant role in propelling the bicycle mechanical disc brake market. Mechanical disc brakes are the preferred choice for e-bikes because they deliver dependable stopping power under varying speeds and loads. Many governments, particularly in Europe, are incentivizing e-bike adoption as part of their green transportation initiatives. These incentives, coupled with an increasing preference for electric mobility, are fueling demand for mechanical disc brakes. As e-bikes transition into mainstream transportation, manufacturers continue to integrate advanced braking systems, ensuring safety and performance for riders.

The market is segmented by brake type into front and rear disc brakes. Front disc brakes accounted for 60% of the market share in 2024 and are projected to generate USD 400 million by 2034. Consumer demand for high-performance bicycles is driving this growth, as front disc brakes provide superior stopping power and better control in challenging conditions. Whether navigating steep terrain or cycling in wet weather, these brakes enhance rider stability and safety. The rise in mountain biking and off-road cycling further fuels the demand for high-precision braking technology that ensures durability and control.

Distribution channels for bicycle mechanical disc brakes are divided into OEM and aftermarket, with OEMs capturing a dominant 72% share in 2024. Bicycle manufacturers are increasingly collaborating with OEM brake suppliers to equip their models with the latest braking technology straight from the factory. These partnerships allow brands to integrate high-performance mechanical disc brakes into their production lines, ensuring that new bicycles meet modern safety and efficiency standards. With rising consumer expectations for premium bicycles, OEM sales are expected to maintain strong momentum, solidifying market growth.

China remains a dominant player in the global bicycle mechanical disc brake market, accounting for 40% of the share in 2024. The country's emphasis on sustainable mobility and reducing vehicle emissions has led to widespread bicycle adoption, particularly in urban areas. China's strong cycling culture, both for commuting and recreation, drives consistent demand for high-quality braking systems. Government policies promoting eco-friendly transport solutions further support this market, positioning China as a critical hub for mechanical disc brake production and innovation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increase in bicycle adoption across the world

- 3.9.1.2 Environmental awareness encourages the shift to eco-friendly transport

- 3.9.1.3 Technological advancements in brake components

- 3.9.1.4 Government initiatives supporting cycling infrastructure

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High competition and price sensitivity

- 3.9.2.2 Shift toward hydraulic disc brakes

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Brake, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front disc brake

- 5.3 Rear disc brake

Chapter 6 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Single piston

- 6.3 Dual piston

- 6.4 Four piston

- 6.5 Multi-piston

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Road bike

- 7.3 Mountain bike

- 7.4 Racing bike

- 7.5 Gravel bikes

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Box Components

- 10.2 Campagnolo

- 10.3 Cane Creek

- 10.4 Clarks Cycle Systems

- 10.5 Formula

- 10.6 Funn Components

- 10.7 Hayes

- 10.8 Hope Technology

- 10.9 Jagwire

- 10.10 KMC

- 10.11 Magura

- 10.12 Nutt

- 10.13 Promax

- 10.14 RockShox

- 10.15 Shimano

- 10.16 SRAM

- 10.17 SunRace

- 10.18 Tektro

- 10.19 XLC

- 10.20 Zoom