デジタルユーティリティ市場の機会、成長促進要因、産業動向分析、2025~2034年予測

Digital Utility Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684697

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

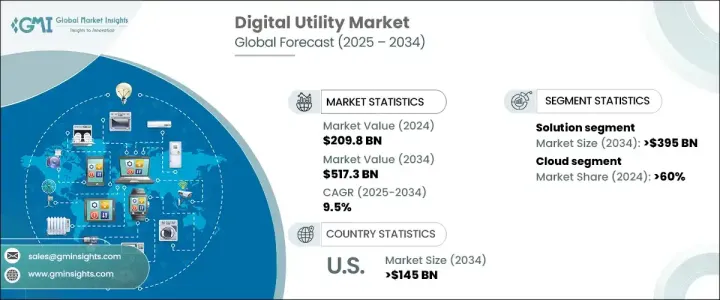

世界のデジタルユーティリティ市場は2024年に2,098億米ドルに達し、2025年から2034年にかけてCAGR 9.5%で成長すると予測されています。

公益事業者がエネルギー効率の向上、運営コストの削減、再生可能エネルギー源の統合を目指す中、スマートグリッド技術の急速な導入がこの拡大を後押ししています。公益事業部門におけるデジタル変革は、リアルタイムのモニタリング、予測分析、自動化を可能にし、最終的にサービスの信頼性を向上させることで、業務を再構築しています。エネルギー需要の増加と気候変動への懸念の高まりにより、高度なデジタル・ソリューションの必要性はかつてないほど高まっています。企業は、老朽化した送電網を近代化し、送電網のセキュリティを強化し、運用を合理化し、進化するエネルギー要件への適応性を確保するために、デジタルインフラに多額の投資を行っています。

世界各国の政府は、近代化を促進する持続可能性イニシアティブと規制枠組みを導入しており、デジタルユーティリティの採用を加速させています。電力会社がエネルギー消費の増加や異常気象による課題に直面しているため、回復力があり安全なグリッド・ソリューションに対する需要が急増しています。高度な計測インフラ、インテリジェントなエネルギー配給システム、自動化ツールは、グリッドの安定性を高める上で基本的なものとなりつつあります。太陽光発電や風力発電を含む分散型エネルギー資源の台頭は、エネルギー配給と需要管理を最適化するデジタル・ソリューションの採用を電力会社にさらに迫っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2,098億米ドル |

| 予測金額 | 5,173億米ドル |

| CAGR | 9.5% |

市場はコンポーネント別にソリューションとサービスに区分されます。2024年にはソリューションが75%のシェアを占め、2034年には3,900億米ドルになると予測されています。スマートメーター、自動エネルギー管理システム、送電網自動化の導入が進み、業界に変革をもたらしています。これらの技術革新は、エネルギー配給を最適化し、リアルタイムの洞察を提供することで、業務効率を向上させています。ユーティリティ企業が複雑なエネルギー変動に対応するため、予知保全と需要対応ソリューションが不可欠になっています。送電網の状況を即座に分析し対応する能力により、デジタル・ソリューションは現代の公益事業運営に不可欠な要素となっています。公益事業者は、AIを活用したアナリティクスを活用して、エネルギー需要の予測、障害の検出、グリッド性能の強化を行い、サービスの中断を最小限に抑えています。

同市場の展開方法は、オンプレミスとクラウドベースのソリューションに分類されます。2024年の市場シェアはクラウド・セグメントが60%を占め、公益事業向けに拡張性とコスト効率の高いインフラ・ソリューションを提供しています。クラウドベースのプラットフォームは、IoTやビッグデータ分析とシームレスに統合され、多額の先行投資を必要とせずにリアルタイムのモニタリングと効率的なグリッド管理を可能にします。デジタルユーティリティが拡大するにつれ、遠隔操作と継続的なデータ駆動型意思決定の必要性が高まっています。クラウドの導入は柔軟性と回復力を確保し、複雑なエネルギー配電網を管理するユーティリティ企業をサポートします。セキュリティは依然として最優先事項であり、プロバイダーはデジタルユーティリティのエコシステムを保護するため、高度な暗号化、自動更新、脅威検知に投資しています。コネクテッド・エネルギー・システムと分散型エネルギー・リソースへの依存の高まりが、クラウド・ソリューションの需要をさらに促進しています。

米国のデジタルユーティリティ市場は、2024年には84%のシェアを占め、2034年には1,400億米ドルを生み出すと予測されています。エネルギー革新を促進する立法措置を含む政府の政策とインセンティブが、国全体のデジタルユーティリティの拡大を促進しています。大手テクノロジー・プロバイダーを中心とした競合情勢が、スマート・ユーティリティ・ソリューションの進歩を促進しています。再生可能エネルギーの統合と送電網の信頼性向上が市場の成長を形成しています。スマートメーターとエネルギー管理システムに対する需要の増加は、業界をさらに強化しています。米国は、自動化、分析、次世代グリッド・インフラに強力な焦点を当て、デジタルユーティリティの変革をリードし続けています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- ソリューションプロバイダー

- サービスプロバイダー

- 販売業者

- エンドユーザー

- 利益率分析

- 特許情勢

- コスト内訳

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- スマートグリッド技術に対する需要の高まり

- IoTとビッグデータ分析の採用増加

- 再生可能エネルギーに対する政府の取り組みと投資

- エネルギー効率と持続可能性への関心の高まり

- 業界の潜在的リスク&課題

- デジタルユーティリティ・ソリューションの初期コストの高さ

- データ・セキュリティとプライバシーに関する懸念

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- 高度計測インフラ(AMI)

- エネルギー管理システム(EMS)

- 顧客情報システム(CIS)

- 地理情報システム(GIS)

- サービス

- コンサルティング・サービス

- システム・インテグレーション

- マネージドサービス

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:ユーティリティ別、2021年~2034年

- 主要動向

- 電力ユーティリティ

- 水道事業者

- ガス事業

第8章 市場推計・予測:最終用途別、2021年~2032年

- 主要動向

- 住宅市場

- 商業

- 産業用

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ABB

- Accenture

- Aclara Technologies

- Capgemini

- Cisco Systems

- Eaton

- Emerson Electric

- General Electric Company

- Hitachi Energy

- Honeywell

- IBM

- Infosys

- Itron

- Landis+Gyr Group

- Microsoft

- Oracle

- SAP SE

- Schneider Electric

- Siemens

- Wipro

目次

The Global Digital Utility Market reached USD 209.8 billion in 2024 and is set to grow at a CAGR of 9.5% between 2025 and 2034. The rapid adoption of smart grid technologies is driving this expansion as utility providers seek to enhance energy efficiency, lower operational costs, and integrate renewable energy sources. Digital transformation in the utility sector is reshaping operations by enabling real-time monitoring, predictive analytics, and automation, ultimately improving service reliability. With increasing energy demands and growing climate concerns, the need for advanced digital solutions is more crucial than ever. Companies are investing heavily in digital infrastructure to modernize aging grids, enhance grid security, and streamline operations, ensuring adaptability to evolving energy requirements.

Governments worldwide are implementing sustainability initiatives and regulatory frameworks that promote modernization, accelerating the adoption of digital utilities. The demand for resilient and secure grid solutions is surging as utilities face challenges posed by rising energy consumption and extreme weather events. Advanced metering infrastructure, intelligent energy distribution systems, and automation tools are becoming fundamental in enhancing grid stability. The rise of decentralized energy resources, including solar and wind power, is further compelling utilities to adopt digital solutions that optimize energy distribution and demand management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $209.8 Billion |

| Forecast Value | $517.3 Billion |

| CAGR | 9.5% |

The market is segmented by components into solutions and services. In 2024, solutions dominated with a 75% share and are projected to generate USD 390 billion by 2034. The increasing deployment of smart meters, automated energy management systems, and grid automation is transforming the industry. These innovations optimize energy distribution and provide real-time insights, improving operational efficiency. Predictive maintenance and demand response solutions are becoming indispensable as utilities navigate complex energy fluctuations. The ability to instantly analyze and respond to grid conditions is making digital solutions a critical element of modern utility operations. Utility providers are leveraging AI-powered analytics to predict energy demand, detect faults, and enhance grid performance, ensuring minimal service disruptions.

Deployment methods in the market are categorized into on-premises and cloud-based solutions. The cloud segment accounted for 60% of the market share in 2024, offering scalable and cost-effective infrastructure solutions for utilities. Cloud-based platforms seamlessly integrate with IoT and big data analytics, enabling real-time monitoring and efficient grid management without requiring significant upfront investments. As digital utilities expand, the need for remote operations and continuous data-driven decision-making is intensifying. Cloud deployment ensures flexibility and resilience, supporting utilities in managing complex energy distribution networks. Security remains a top priority, with providers investing in advanced encryption, automated updates, and threat detection to safeguard digital utility ecosystems. The growing reliance on connected energy systems and distributed energy resources is further fueling the demand for cloud solutions.

The US digital utility market held an 84% share in 2024 and is projected to generate USD 140 billion by 2034. Government policies and incentives, including legislative measures promoting energy innovation, are driving the expansion of digital utilities across the country. A competitive landscape featuring leading technology providers is propelling advancements in smart utility solutions. The integration of renewable energy sources and the emphasis on enhancing grid reliability are shaping the market's growth. Increasing demand for smart metering and energy management systems is further strengthening the industry. The US continues to lead the digital utility transformation, with a strong focus on automation, analytics, and next-generation grid infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Solution Providers

- 3.2.2 Service Providers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Patent Landscape

- 3.5 Cost Breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for smart grid technologies

- 3.9.1.2 Increasing adoption of IoT and big data analytics

- 3.9.1.3 Government initiatives and investments in renewable energy

- 3.9.1.4 Growing focus on energy efficiency and sustainability

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs of digital utility solutions

- 3.9.2.2 Data security and privacy concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Advanced Metering Infrastructure (AMI)

- 5.2.2 Energy Management System (EMS)

- 5.2.3 Customer Information System (CIS)

- 5.2.4 Geographic Information System (GIS)

- 5.3 Services

- 5.3.1 Consulting services

- 5.3.2 System integration

- 5.3.3 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Utility, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Power utilities

- 7.3 Water utilities

- 7.4 Gas utilities

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Accenture

- 10.3 Aclara Technologies

- 10.4 Capgemini

- 10.5 Cisco Systems

- 10.6 Eaton

- 10.7 Emerson Electric

- 10.8 General Electric Company

- 10.9 Hitachi Energy

- 10.10 Honeywell

- 10.11 IBM

- 10.12 Infosys

- 10.13 Itron

- 10.14 Landis+Gyr Group

- 10.15 Microsoft

- 10.16 Oracle

- 10.17 SAP SE

- 10.18 Schneider Electric

- 10.19 Siemens

- 10.20 Wipro

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日