|

市場調査レポート

商品コード

1684685

スマート車両アーキテクチャ市場の機会、成長促進要因、産業動向分析、2025~2034年予測Smart Vehicle Architecture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スマート車両アーキテクチャ市場の機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年01月14日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

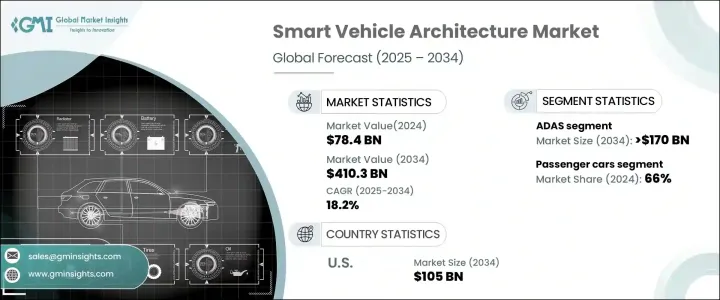

世界のスマート車両アーキテクチャ市場は、2024年に784億米ドルを生み出し、2025年から2034年にかけて18.2%という著しいCAGRで拡大すると予想されています。

自動車技術の進化に伴い、メーカーはシームレスな接続性を優先し、Vehicle-to-Everything(V2X)、インテリジェントなテレマティクス、高度な診断ツールなどの最先端の通信システムを統合しています。5Gネットワークの普及はこのシフトをさらに加速させ、より高速なデータ・トランスミッション、サービスの信頼性向上、待ち時間の短縮を可能にしています。

このような進歩により、自動車の状況は一変し、比類のないコネクティビティとユーザー体験を提供する、インテリジェントでソフトウェア主導の自動車への道が開かれつつあります。電気自動車(EV)が勢いを増す中、自動車メーカーは、従来のパワートレインと電気パワートレインの両方をサポートする柔軟なモジュール設計に対応するため、車両アーキテクチャを再構築しています。このシフトは、生産効率を最適化するだけでなく、安全性、利便性、自動化を強化するコネクテッド、ソフトウェア定義型車両に対する消費者の需要の高まりにも対応しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 784億米ドル |

| 予測金額 | 4,103億米ドル |

| CAGR | 18.2% |

スマート車両アーキテクチャは、V2X通信、ADAS(先進運転支援システム)、インフォテインメントとコネクティビティ、OTA(Over-the-Air)アップデート、サイバーセキュリティ・ソリューション、機械学習(ML)を備えた人工知能(AI)など、一連の変革技術によって推進されています。2024年には、ADASが市場シェアの51%を占め、自動車の安全性と自動化の向上に重要な役割を果たしています。自動車メーカーが先進運転支援機能に注力するなか、アダプティブ・クルーズ・コントロール、自動緊急ブレーキ、交通標識認識などの機能が業界標準になりつつあります。これらの技術の急速な統合は、ユーザー・エクスペリエンスを向上させるだけでなく、規制機関がより厳格な安全コンプライアンスを推進する中で、市場の成長を後押ししています。

市場は、乗用車、商用車、EVなど車両タイプ別に区分されます。2024年には、生産台数の多さ、消費者の需要の高まり、先進的な車載技術の普及が追い風となり、乗用車が66%のシェアを占め、市場を席巻します。都市化が加速し、都市人口が増加するなか、乗用車は依然として好ましい交通手段であり、消費者はシームレスな接続性、電動化、革新的な機能を提供する自動車をますます求めるようになっています。次世代インフォテインメント・システム、自律走行機能、統合AIソリューションへの需要がさらなる技術革新に拍車をかけており、スマート車両アーキテクチャは自動車の将来にとって重要な要素となっています。

米国のスマート車両アーキテクチャ市場は、2024年には85%という圧倒的なシェアを占めており、これは自動車技術革新における米国のリーダーシップの証です。2034年までに、米国市場は1,050億米ドルを生み出すと予測されており、これは先進自動車技術の積極的な採用を反映しています。AI主導の自律走行車開発に重点を置く大手ハイテク企業の存在により、米国はスマート車両アーキテクチャーの世界的リーダーとして位置付けられています。この地域の自動車メーカーは、EVと自律走行車の両方におけるインテリジェント車両システムの統合を先導しており、市場の優位性を強化しています。AI、コネクティビティ、電動化の進展に伴い、スマート車両アーキテクチャの将来は、世界規模でモビリティと輸送を再定義することになると思われます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 技術プロバイダー

- 部品サプライヤー

- OEMメーカー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- コネクテッドカーの需要増加

- 電気自動車の成長

- 自律走行車の採用増加

- ソフトウェア定義の自動車への注目の高まり

- 業界の潜在的リスク&課題

- 高い開発コスト

- データセキュリティとプライバシーに関する懸念

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ADAS

- インフォテインメント&コネクティビティ

- V2x通信

- 無線(OTA)アップデート

- サイバーセキュリティ・ソリューション

- AIとML

第6章 市場推計・予測:アーキテクチャ別、2021年~2034年

- 主要動向

- 集中型アーキテクチャ

- ゾーン型アーキテクチャ

- モジュール型プラットフォーム

- 分散型アーキテクチャ

第7章 市場推計・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- 商用車

- 電気自動車

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自律走行

- インフォテインメントとユーザーエクスペリエンス

- 安全・セキュリティ

- フリート管理

- エネルギー管理

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aptiv

- Mobileye

- Magna International

- RT-RK

- Huawei Intelligent Automotive Solution(Yinwang)

- Infineon Technologies

- Momenta

- Bosch

- Continental AG

- NVIDIA

- Qualcomm

- Texas Instruments

- Renesas Electronics

- Valeo

- Denso Corporation

- ZF Friedrichshafen

- Panasonic Automotive Systems

- Harman International

- Delphi Technologies

- Lear Corporation

The Global Smart Vehicle Architecture Market generated USD 78.4 billion in 2024 and is expected to expand at a remarkable CAGR of 18.2% between 2025 and 2034. As automotive technology evolves, manufacturers are prioritizing seamless connectivity, integrating cutting-edge communication systems such as Vehicle-to-Everything (V2X), intelligent telematics, and advanced diagnostic tools. The widespread rollout of 5G networks is further accelerating this shift, enabling faster data transmission, enhanced service reliability, and reduced latency.

These advancements are transforming the automotive landscape, paving the way for intelligent, software-driven vehicles that offer unparalleled connectivity and user experience. With electric vehicles (EVs) gaining momentum, automakers are reimagining vehicle architectures to accommodate flexible, modular designs that support both traditional and electric powertrains. This shift is not only optimizing production efficiency but also meeting the rising consumer demand for connected, software-defined vehicles that enhance safety, convenience, and automation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $78.4 Billion |

| Forecast Value | $410.3 Billion |

| CAGR | 18.2% |

Smart vehicle architecture is being driven by a suite of transformative technologies, including V2X communication, Advanced Driver Assistance Systems (ADAS), infotainment and connectivity, Over-the-Air (OTA) updates, cybersecurity solutions, and artificial intelligence (AI) with machine learning (ML). In 2024, ADAS accounted for 51% of the market share, playing a critical role in improving vehicle safety and automation. As automakers focus on advanced driver-assistance capabilities, features such as adaptive cruise control, automatic emergency braking, and traffic sign recognition are becoming industry standards. The rapid integration of these technologies is not only enhancing user experience but also propelling market growth as regulatory bodies push for stricter safety compliance.

The market is segmented by vehicle type, including passenger cars, commercial vehicles, and EVs. In 2024, passenger cars dominated the market with a 66% share, driven by high production volumes, growing consumer demand, and widespread adoption of advanced in-car technologies. As urbanization accelerates and city populations grow, passenger vehicles remain the preferred mode of transport, with consumers increasingly seeking vehicles that offer seamless connectivity, electrification, and innovative features. The demand for next-generation infotainment systems, autonomous driving capabilities, and integrated AI solutions is fueling further innovation, making smart vehicle architectures a key component of the automotive future.

U.S. smart vehicle architecture market held a commanding 85% share in 2024, a testament to the country's leadership in automotive innovation. By 2034, the U.S. market is projected to generate USD 105 billion, reflecting its aggressive adoption of advanced automotive technologies. The presence of major tech companies, along with a strong emphasis on AI-driven autonomous vehicle development, is positioning the U.S. as a global leader in smart vehicle architecture. Automakers in the region are spearheading the integration of intelligent vehicle systems in both EVs and autonomous vehicles, reinforcing the market's dominance. With ongoing advancements in AI, connectivity, and electrification, the future of smart vehicle architecture is set to redefine mobility and transportation on a global scale.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 OEMs

- 3.1.4 End user

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for connected vehicles

- 3.7.1.2 Growth of electric vehicles

- 3.7.1.3 Rising adoption of autonomous vehicles

- 3.7.1.4 Increasing focus on software-defined vehicles

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High development costs

- 3.7.2.2 Data security & privacy concerns

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 ADAS

- 5.3 Infotainment & connectivity

- 5.4 V2x communication

- 5.5 Over-the-air (OTA) updates

- 5.6 Cybersecurity solutions

- 5.7 AI & ML

Chapter 6 Market Estimates & Forecast, By Architecture, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Centralized architectures

- 6.3 Zonal architectures

- 6.4 Modular platforms

- 6.5 Distributed architectures

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.3 Commercial vehicles

- 7.4 Electric vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Autonomous driving

- 8.3 Infotainment & user experience

- 8.4 Safety & security

- 8.5 Fleet management

- 8.6 Energy management

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv

- 10.2 Mobileye

- 10.3 Magna International

- 10.4 RT-RK

- 10.5 Huawei Intelligent Automotive Solution (Yinwang)

- 10.6 Infineon Technologies

- 10.7 Momenta

- 10.8 Bosch

- 10.9 Continental AG

- 10.10 NVIDIA

- 10.11 Qualcomm

- 10.12 Texas Instruments

- 10.13 Renesas Electronics

- 10.14 Valeo

- 10.15 Denso Corporation

- 10.16 ZF Friedrichshafen

- 10.17 Panasonic Automotive Systems

- 10.18 Harman International

- 10.19 Delphi Technologies

- 10.20 Lear Corporation