|

市場調査レポート

商品コード

1892913

自転車用コンピュータ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Bike Computer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自転車用コンピュータ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月05日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

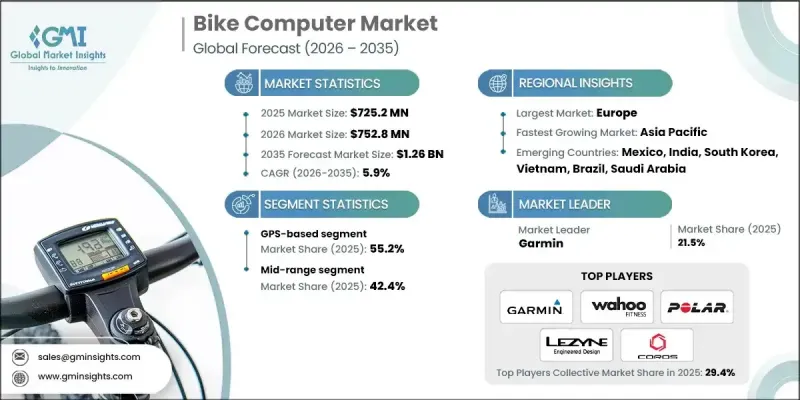

世界の自転車用コンピュータ市場は、2025年に7億2,520万米ドルと評価され、2035年までにCAGR5.9%で成長し、12億6,000万米ドルに達すると予測されています。

個人の健康増進への関心の高まりと、日常生活におけるテクノロジーの統合が進む中、速度、ケイデンス、心拍数、その他のパフォーマンス指標を追跡するデバイスの需要は引き続き増加しています。世界中の健康志向の方々の間で、サイクリングは好まれる活動となっています。特に、糖尿病、心臓疾患、体重管理など生活習慣病に関連する懸念が、より活動的な習慣へと人々を導いているためです。また、複数の地域の政府が二酸化炭素排出量の削減や交通渋滞の緩和を目的としてサイクリングを推進していることから、環境への配慮も大きな役割を果たしています。デジタルシステムの進歩と、モビリティアプリケーションにおけるAIおよび機械学習の役割拡大により、よりスマートで直感的な自転車用コンピュータが市場に登場し、その魅力が高まると予想されます。サイクリングイベントや公共の健康増進プログラムの普及も、トレーニングやパフォーマンスモニタリングを強化するデバイスの利用をさらに後押ししています。フィットネステクノロジーに対する世界の関心が高まり続ける中、接続性と知能性を備えた自転車用コンピュータに対する全体的な需要は加速すると見込まれます。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 7億2,520万米ドル |

| 予測金額 | 12億6,000万米ドル |

| CAGR | 5.9% |

GPS搭載セグメントは2024年に55.2%のシェアを占めました。これらのデバイスは従来のナビゲーションツールをはるかに超え、サイクリストが求める詳細な走行データをリアルタイムで提供します。優れた地図機能により、GPS非搭載製品と比較して優先的に選択されており、レクリエーション・通勤・運動目的での世界のサイクリング普及と一致しています。消費者の期待が高まる中、ライダーは距離・速度・関連指標のより正確な追跡を一貫して求めています。

高価格帯のサイクルコンピュータセグメントは、AI強化型分析機能、高度な健康管理機能、スマートバッテリー最適化機能などの特徴により、2034年までにCAGR7.1%で成長が見込まれます。各ブランドはユーザー嗜好の動向に注力し、製品ラインの洗練と統合機能の拡充を進めています。このセグメントは、機能拡張された高級機種を選択する購入者が増加する中、可処分所得の増加による恩恵を受けています。

米国自転車用コンピュータ市場は、接続型サイクリング技術の急速な成長と自転車利用者の増加に支えられ、2025年に1億8,520万米ドルに達しました。複数の企業が次世代機能の導入や製品革新における基準設定を通じて、同国における動向形成に影響を与え続けています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界のサイクリング参加率の増加と健康意識の動向

- 電動アシスト自転車市場の拡大と統合ディスプレイ需要

- プロサイクリングの影響力とUCIワールドツアーにおける技術採用

- スマートシティインフラ開発と自転車利用の統合

- 業界の潜在的リスク&課題

- スマートフォン代替の脅威と無料アプリの代替案

- 都市部市場における盗難リスクとデバイスセキュリティへの懸念

- 市場機会

- 新興市場への浸透

- 電動アシスト自転車の統合とOEMパートナーシップの拡大

- グラベル&アドベンチャーサイクリングセグメントの拡大

- スマートシティ及び自治体向け自転車データプラットフォーム統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 技術ロードマップと進化

- 技術導入ライフサイクル分析

- 価格動向

- 地域別

- 製品別

- 特許分析

- スマートシティ・インフラ統合

- 交通管理のための自転車検知技術

- 自転車用コンピュータと交通インフラの連携

- 自治体向け自転車データプラットフォーム

- メーカー様向けスマートシティ連携の機会

- センサーエコシステムとアクセサリー市場

- センサー市場概要と収益貢献度

- 速度・ケイデンスセンサー

- 心拍数モニター

- パワーメーター

- 新興センサーカテゴリー

- 消費者行動と購買意思決定分析

- 購入決定要因と機能優先順位付け

- ブランドロイヤルティと乗り換え行動パターン

- プロサイクリング及びアスリート起用広告の影響

- オンライン購入と店舗購入の嗜好比較

- 消費者動向と嗜好の変化

- タッチスクリーンとボタン式インターフェースの移行動向

- ナビゲーション機能の重要性増加

- スマートフォン連携への期待

- 購入の重要な決定要因としてのバッテリー寿命

- 小売チャネルの動向と流通戦略

- 専門自転車小売市場のシェアと動向

- オンライン直接消費者向け販売(DTC)の成長

- 大衆市場小売への浸透

- 自転車購入時のOEMバンドリング

- 製品ライフサイクルと使用パターンの分析

- 製品の平均寿命と耐久性

- ファームウェア更新頻度と長期サポート

- ユーザーセグメント別使用頻度

- 季節による使用状況の変化と天候の影響

- 将来展望と機会

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画と資金調達

- ベンダー選定基準

第5章 市場推計・予測:製品別、2022-2035

- 有線

- ワイヤレス

- GPSベース

- 太陽光発電

- その他

第6章 市場推計・予測:価格帯別、2022-2035

- 基本

- 中価格帯

- プレミアム

第7章 市場推計・予測:センサー別、2022-2035

- リアホイールセンサー

- 速度/ケイデンスセンサー

- 勾配センサー

- 心拍数センサー

第8章 市場推計・予測:接続方式別、2022-2035

- Bluetooth

- Wi-Fi

- ANT+

- その他

第9章 市場推計・予測:自転車別、2022-2035

- マウンテンバイク

- ロードバイク

- 都市型自転車

- 電動自転車

- グラベルバイク

第10章 市場推計・予測:流通チャネル別、2022-2035

- オンライン

- オフライン

第11章 市場推計・予測:用途別、2022-2035

- 陸上競技およびスポーツ

- フィットネス及び通勤

- レクリエーション/レジャー

第12章 市場推計・予測:最終用途別、2022-2035

- 個人消費者

- 自転車レンタル/フリート事業者

- プロフェッショナルチーム/クラブ

第13章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- マレーシア

- インドネシア

- ベトナム

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第14章 企業プロファイル

- 世界企業

- Garmin

- Wahoo Fitness

- Polar Electro Oy

- Hammerhead

- Stages Cycling

- Lezyne

- 地域企業

- SIGMA

- Bryton

- CatEye

- Giant Manufacturing

- Specialized Bicycle Components

- Bosch eBike Systems

- Shimano

- Mio Technology

- 新興企業

- Coospo

- iGPSPORT

- Magene

- Coros

- Suunto

- Omata

- Beeline

- Xplova

- Cycplus

- Trek Bicycle Corporation

- Cannondale