|

市場調査レポート

商品コード

1684623

自転車用チェーンデバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Bicycle Chain Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自転車用チェーンデバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月09日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

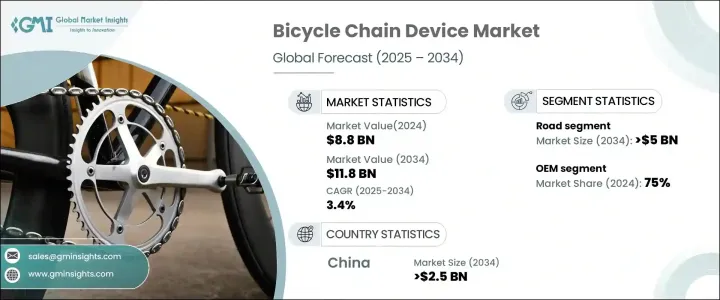

世界の自転車用チェーンデバイス市場は、2024年に88億米ドルと評価され、2025年から2034年にかけてCAGR 3.4%で拡大すると予測されています。

この成長の背景には、伝統的なサイクリングと近代的な電動サポートを融合させ、持続可能で効率的な移動手段を提供する電動自転車(E-bike)の人気の高まりなど、いくつかの重要な要因があります。E-バイクは、特に、自動車に代わる環境に優しい交通手段を求める都市部の通勤者の間で急速に普及しています。都市がより持続可能な社会を目指す中、サイクリングは交通渋滞を緩和し、二酸化炭素排出量を削減する好ましいソリューションとして勢いを増しています。さらに、消費者の間で健康とウェルネスがますます優先されるようになり、サイクリングはレクリエーションとして好まれるようになりました。この需要は、フィットネス目的で自転車を利用する傾向が世界的に高まり続けていることも後押ししています。

自転車用チェーンデバイス市場のもう一つの重要な促進要因は、消費者の嗜好が高級で技術的に先進的な部品へとシフトしていることです。サイクリング愛好家がより優れた性能、耐久性、快適性を求めるようになり、高品質のチェーン・デバイスへの需要が高まっています。メーカーは、サイクリング体験全般を向上させ、よりスムーズな変速、エネルギー伝達の改善、長持ちする耐久性を提供する製品を革新的に開発しています。都市化が進み、実用的な移動手段としての自転車が各地域で採用されるようになったことで、高品質の自転車用部品、特にチェーン・デバイスの需要は今後も増え続けると思われます。さらに、レジャーや競合スポーツのために自転車を利用する傾向が強まっており、サイクリストはカジュアルなサイクリング活動でも高強度のサイクリング活動でもトップクラスの性能を求めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 88億米ドル |

| 予測金額 | 118億米ドル |

| CAGR | 3.4% |

市場は、ロードバイク、マウンテンバイク、電動アシスト自転車など、用途によっていくつかの主要セグメントに分けられます。ロードバイクは2024年に55%を占める最大シェアを占め、2034年までに50億米ドルの市場規模が見込まれます。これらの自転車はフィットネス、レクリエーション、競合サイクリングに人気があり、スムーズな変速と効率的な動力伝達を確保するために高性能のチェーン装置が必要とされます。ロード・サイクリングは依然として世界的に最も人気のあるカテゴリーであるため、このセグメントにおける高度なチェーン・デバイスの需要は今後も市場成長を牽引していくと思われます。

販売チャネルを見ると、市場はOEM(相手先ブランド製造)とアフターマーケットに区分されます。2024年の市場は、OEMセグメントが75%のシェアを占めています。この分野は、生産時にチェーン装置を新しい自転車に組み込むことで、互換性、信頼性、トップクラスの品質を確保することが原動力となっています。自転車、特にe-bikeの需要が世界的に急増し続けているため、OEMは性能と耐久性に対する消費者の期待に応える高品質な統合部品の生産に注力しています。

地域的な優位性という点では、中国は2024年時点で世界の自転車用チェーンデバイス市場の50%という大きなシェアを占めており、2034年までこの地位を維持すると予想されます。自転車生産分野における中国の優位性は、世界最大の自転車製造・輸出国であることに起因しています。同国は、強力でコスト効率の高い生産エコシステムと広範なサプライヤー・ネットワークの恩恵を受けています。さらに、移動、フィットネス、レクリエーションのためのサイクリング人気の高まりに後押しされた中国国内での自転車需要の増加は、同国の市場リーダーシップをさらに強化しています。さらに、e-bike製造分野での中国の役割は、サイクリング・インフラとグリーン・モビリティ・ソリューションの促進を目的とした政府のインセンティブに支えられ、世界市場での地位をさらに強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 自転車用チェーンデバイスメーカー

- OEMディストリビューター

- アフターマーケットプロバイダー

- エンドユーザー

- 利益率分析

- 特許情勢

- コスト内訳

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- フィットネスとレクリエーションを目的としたサイクリングの普及

- 電動自転車(e-bike)の人気上昇

- 軽量で耐久性のある素材など、チェーンデバイスの技術的進歩

- 競合サイクリングやマウンテンバイクへの関心の高まり

- 業界の潜在的リスク&課題

- 新興市場における価格感応度の高さ

- 過酷な条件下での頻繁な交換につながる耐久性への懸念

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 自転車用チェーン

- チェーンリング

- ディレーラー

- チェーンガイド

- チェーンテンショナー

- その他

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ロードバイク

- マウンテンバイク

- 電動アシスト自転車

第7章 市場推計・予測:販売チャネル別、2021年~2032年

- 主要動向

- OEM

- アフターマーケット

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Bafang Electric

- Campagnolo

- Cane Creek Cycling Components

- FSA(Full Speed Ahead)

- Gates Carbon Drive

- Hawley-Lambert

- KMC Chains

- Mavic

- Microshift

- Prologo

- Race Face

- Rotor Bike Components

- Shimano

- SR Suntour

- SRAM

- Sugino

- Trek Bicycle

- TRP Cycling

- Wippermann Chains

- Zee Industry

The Global Bicycle Chain Device Market, valued at USD 8.8 billion in 2024, is projected to expand at a CAGR of 3.4% from 2025 to 2034. This growth can be attributed to several key factors, including the growing popularity of electric bicycles (e-bikes), which blend traditional cycling with modern motorized support, offering a sustainable and efficient mode of transportation. E-bikes are quickly gaining traction, particularly among urban commuters seeking eco-friendly alternatives to cars. As cities work toward becoming more sustainable, cycling is gaining momentum as a preferred solution for reducing traffic congestion and lowering carbon emissions. Furthermore, with health and wellness increasingly prioritized by consumers, cycling has become a favored recreational activity, contributing to rising demand for bicycles and their essential components, including advanced chain devices. This demand is further driven by the trend of using bicycles for fitness purposes, which continues to rise globally.

Another significant driver for the bicycle chain device market is the shift in consumer preferences toward premium and technologically advanced components. As cycling enthusiasts seek better performance, durability, and comfort, demand for high-quality chain devices is on the rise. Manufacturers are innovating and developing products that enhance the overall cycling experience, offering smoother shifting, improved energy transfer, and longer-lasting durability. With urbanization and the adoption of bicycles as a practical mode of transport growing across regions, the demand for quality bicycle components, especially chain devices, will continue to rise. Additionally, the increasing trend of cycling for leisure and competitive sports is propelling the market further, with cyclists demanding top-tier performance for both casual and high-intensity cycling activities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 3.4% |

The market is divided into several key segments based on application, including road bicycles, mountain bicycles, and electric bicycles. Road bicycles hold the largest share of the market, accounting for 55% in 2024, and are expected to generate USD 5 billion by 2034. These bicycles are popular for fitness, recreation, and competitive cycling, which require high-performance chain devices to ensure smooth shifting and efficient power transfer. As road cycling remains the most popular category globally, the demand for advanced chain devices in this segment will continue to drive market growth.

When examining sales channels, the market is segmented into OEM (Original Equipment Manufacturer) and aftermarket sales. The OEM segment dominated the market in 2024 with a 75% share. This segment is driven by the integration of chain devices into new bicycles during production, ensuring compatibility, reliability, and top-tier quality. As the demand for bicycles, especially e-bikes continues to surge globally, OEMs are focused on producing high-quality, integrated components that meet consumer expectations for performance and durability.

In terms of regional dominance, China holds a significant 50% share of the global bicycle chain device market in 2024 and is expected to maintain this position through 2034. China's dominance in the bicycle production sector can be attributed to its position as the world's largest manufacturer and exporter of bicycles. The country benefits from a strong, cost-effective production ecosystem and an extensive supplier network. Additionally, the increasing demand for bicycles within China, spurred by the growing popularity of cycling for transportation, fitness, and recreation, further reinforces the country's market leadership. Moreover, China's role in the e-bike manufacturing sector further strengthens its position in the global market, supported by government incentives aimed at promoting cycling infrastructure and green mobility solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Bicycle chain device manufacturers

- 3.2.2 OEM distributors

- 3.2.3 Aftermarket providers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Patent Landscape

- 3.5 Cost Breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of cycling for fitness and recreation

- 3.9.1.2 Rising popularity of electric bicycles (e-bikes)

- 3.9.1.3 Technological advancements in chain devices, such as lightweight and durable materials

- 3.9.1.4 Growing interest in competitive cycling and mountain biking

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High price sensitivity in emerging markets

- 3.9.2.2 Durability concerns, leading to frequent replacements in harsh conditions

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Bicycle chains

- 5.3 Chainrings

- 5.4 Derailleurs

- 5.5 Chain guides

- 5.6 Chain tensioners

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Road bicycles

- 6.3 Mountain bicycles

- 6.4 Electric bicycles

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Bafang Electric

- 9.2 Campagnolo

- 9.3 Cane Creek Cycling Components

- 9.4 FSA (Full Speed Ahead)

- 9.5 Gates Carbon Drive

- 9.6 Hawley-Lambert

- 9.7 KMC Chains

- 9.8 Mavic

- 9.9 Microshift

- 9.10 Prologo

- 9.11 Race Face

- 9.12 Rotor Bike Components

- 9.13 Shimano

- 9.14 SR Suntour

- 9.15 SRAM

- 9.16 Sugino

- 9.17 Trek Bicycle

- 9.18 TRP Cycling

- 9.19 Wippermann Chains

- 9.20 Zee Industry