自転車用電子ドライブトレインの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Bicycle Electronic Drivetrain Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684594

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

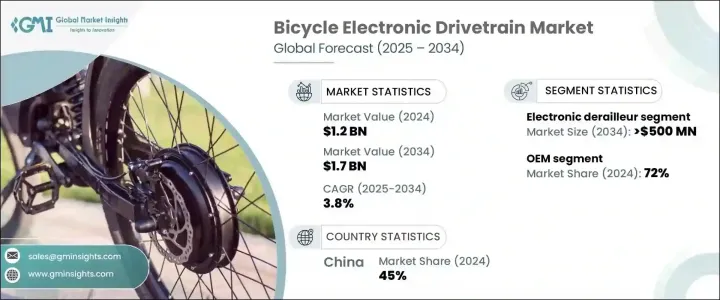

自転車用電子ドライブトレインの世界市場は、2024年に12億米ドルと評価され、2025年から2034年にかけて3.8%の安定したCAGRで拡大すると予測されています。

市場拡大の主な原動力は、E-bikeの普及拡大です。先進的な電子ドライブトレインに大きく依存するE-BIKEは、スムーズで効率的な動力伝達を提供し、ライダーに環境に優しく便利な移動手段、特に都市環境での移動手段を提供します。より多くの消費者が持続可能な移動手段を受け入れ、混雑した都市で従来の乗り物に代わる環境に優しい交通手段を求めているため、この需要の高まりは自転車業界を再構築しています。さらに、e-bikeは日常的な通勤用としてだけでなく、都市部の混雑や環境への影響に対する懸念の高まりに対する解決策としても人気を集めています。

サイクリングスポーツが世界の盛り上がりを見せるなか、高性能の自転車が求められるようになり、自転車用電子ドライブトレイン市場の成長をさらに後押ししています。アスリートやサイクリング愛好家は現在、ギアシステムに高いレベルの精度と信頼性を求めています。電子ドライブトレインは、完璧なギアシフトを実現するように設計されており、最高のパフォーマンスを必要とする競技サイクリストにとって理想的なものとなっています。自動変速、ワイヤレス接続、調整可能な設定などの機能は、トレーニング中や競技レースの両方でサイクリング体験を向上させています。こうした進歩により、サイクリングはレクリエーションからハイテクスポーツへと変貌を遂げ、プロアスリートからカジュアルライダーまで幅広いニーズに対応しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 12億米ドル |

| 予測金額 | 17億米ドル |

| CAGR | 3.8% |

市場は、電子シフター、電子ディレイラー、バッテリーシステム、コントロールユニットなどの主要コンポーネントに分けられます。2034年には、電子ディレイラー分野だけで5億米ドルの売上が見込まれ、2024年の市場シェアの35%以上を占めました。この需要の増加は、サイクリング分野における持続可能性への注目の高まりと密接に結びついています。消費者が環境に優しい交通手段を優先し続ける中、電子ディレーラーのような先進的な電子ドライブトレインを搭載した自転車は、魅力的なソリューションを提供しています。これらのコンポーネントは、持続可能な移動手段としてのe-bikeや自転車の魅力の高まりに貢献しています。

市場はまた、OEM(相手先ブランド製造)とアフターマーケットという流通チャネルによっても区分されます。2024年には、OEMセグメントが市場シェアの72%を占めました。このOEM需要の急増は、最先端のドライブトレインシステムを搭載した高性能自転車を選ぶようになっている競合サイクリストや愛好家によってもたらされています。サイクリングにおける精度、耐久性、スピードへの要求が、電子ドライブトレインコンポーネントの成長に拍車をかけています。特に電子ディレーラーは、優れた変速精度を達成するために不可欠なものとなっており、ライダーがサイクリングを最大限に楽しめるようにしています。

地理的には、中国が自転車用電子ドライブトレイン市場を独占しており、2024年の市場シェアは45%に達しました。アジア太平洋地域の急速な都市化が、この動向を後押しする大きな要因となっています。都市が成長し交通渋滞が激化するにつれ、効率的で環境に優しい交通ソリューションに対する需要が高まっています。高度な電子ドライブトレインを搭載したE-bikeは、この新たなニーズに最適で、混雑した道路を高速で移動する便利な方法を提供します。都市中心部の拡大とサイクリングインフラの充実により、ハイテクE-BIKEへの需要がこの地域の継続的な市場成長を促進すると予想されます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場範囲・定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 原材料プロバイダー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 最終顧客

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース・イニシアチブ

- 規制状況

- 親子市場分析

- 影響要因

- 成長促進要因

- 高性能自転車への需要の高まり

- ドライブトレインシステムの技術進歩

- e-bikeと電動アシスト自転車の成長

- ユーザー体験の向上と変速精度の向上

- 業界の潜在的リスク・課題

- 電子ドライブトレインの初期コストの高さ

- メンテナンスとバッテリー寿命への懸念

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 電子シフター

- 電子ディレイラー

- バッテリーシステム

- コントロールユニット

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ロードバイク

- マウンテンバイク

- レーシングバイク

- グラベルバイク

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- プロサイクリスト

- アマチュアサイクリスト

- コミューター

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Bafang

- Bosch

- Campagnolo

- Cervelo

- Factor Bikes

- Fazua GmbH

- Focus Bikes

- FSA

- Giant

- Look Cycle

- MAGURA

- Ridley Bikes

- Rotor Bike Components

- Scott Sports

- Shimano

- Specialized Bicycle

- SRAM

- TranzX

- Valeo

- Wilier Triestina

目次

The Global Bicycle Electronic Drivetrain Market, valued at USD 1.2 billion in 2024, is projected to expand at a steady CAGR of 3.8% from 2025 to 2034. A major driving force behind market expansion is the increasing adoption of e-bikes. E-bikes, which rely heavily on advanced electronic drivetrains, offer a smooth and efficient power transfer, providing riders with an eco-friendly, convenient mode of transportation-especially in urban environments. This growing demand is reshaping the bicycle industry as more consumers embrace sustainable travel options, seeking greener alternatives to traditional vehicles in congested cities. Additionally, e-bikes are gaining popularity not only for everyday commuting but also as a solution to the rising concerns of urban congestion and environmental impact.

As cycling sports continue to gain traction globally, high-performance bicycles are becoming more sought after, further fueling the growth of the bicycle electronic drivetrain market. Athletes and cycling enthusiasts now expect a higher level of precision and reliability from their gear systems. Electronic drivetrains are designed to deliver flawless gear shifting, making them ideal for competitive cyclists who require peak performance. Features such as automatic gear shifting, wireless connectivity, and adjustable settings are enhancing the cycling experience, both during training and in competitive races. These advancements are transforming cycling from a recreational activity into a high-tech sport, catering to the needs of professional athletes and casual riders alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $1.7 Billion |

| CAGR | 3.8% |

The market is divided into key components, including electronic shifters, electronic derailleurs, battery systems, and control units. By 2034, the electronic derailleur segment alone is expected to generate USD 500 million, holding more than 35% of the market share in 2024. This rise in demand is closely tied to the increasing focus on sustainability within the cycling sector. As consumers continue to prioritize environmentally friendly transportation options, bicycles with advanced electronic drivetrains, such as electronic derailleurs, are offering an attractive solution. These components contribute to the growing appeal of e-bikes and bicycles as a sustainable mode of travel.

The market is also segmented by distribution channels, namely OEM (Original Equipment Manufacturer) and aftermarket. In 2024, the OEM segment accounted for 72% of the market share. This surge in OEM demand is driven by competitive cyclists and enthusiasts who are increasingly opting for high-performance bicycles equipped with cutting-edge drivetrain systems. The demand for precision, durability, and speed in cycling is fueling the growth of electronic drivetrain components. Electronic derailleurs, in particular, have become essential for achieving superior shifting accuracy, ensuring riders get the most out of their cycling experience.

Geographically, China dominates the bicycle electronic drivetrain market, holding a 45% market share in 2024. The rapid urbanization of the Asia-Pacific region is a major factor driving this trend. As cities grow and traffic congestion intensifies, there is a rising demand for efficient and eco-friendly transportation solutions. E-bikes equipped with advanced electronic drivetrains are the perfect fit for this emerging need, offering a fast, convenient way to navigate crowded streets. With expanding urban centers and better cycling infrastructure, the demand for high-tech e-bikes is expected to fuel continued market growth in this region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Parent and child market analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for high-performance bicycles

- 3.9.1.2 Technological advancements in drivetrain systems

- 3.9.1.3 Growth of e-bikes and electric bicycles

- 3.9.1.4 Better user experience and precision in shifting

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs of electronic drivetrains

- 3.9.2.2 Maintenance and battery life concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 electronic shifter

- 5.3 electronic derailleur

- 5.4 battery system

- 5.5 control unit

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Road bike

- 6.3 Mountain bike

- 6.4 Racing bike

- 6.5 Gravel bike

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Professional cyclist

- 7.3 Amateur cyclist

- 7.4 Commuter

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Bafang

- 10.2 Bosch

- 10.3 Campagnolo

- 10.4 Cervelo

- 10.5 Factor Bikes

- 10.6 Fazua GmbH

- 10.7 Focus Bikes

- 10.8 FSA

- 10.9 Giant

- 10.10 Look Cycle

- 10.11 MAGURA

- 10.12 Ridley Bikes

- 10.13 Rotor Bike Components

- 10.14 Scott Sports

- 10.15 Shimano

- 10.16 Specialized Bicycle

- 10.17 SRAM

- 10.18 TranzX

- 10.19 Valeo

- 10.20 Wilier Triestina

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日